As 2025 rolls by the real estate market in the Los Angeles South Bay continues to slide downward. January started the year with 11% more homes sold than in 2024. Now, with June in the books, the difference is 0% growth in sales across the South Bay. From month to month the numbers are up and down, but the end result is down.

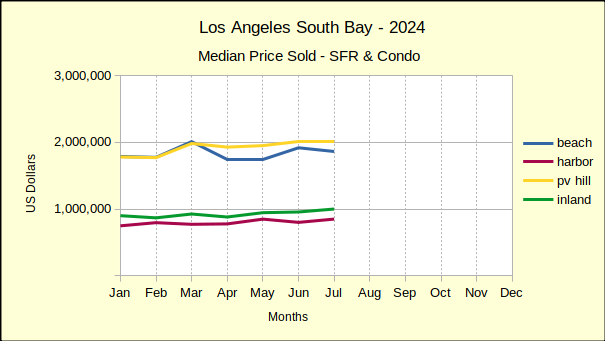

With the exception of the Beach cities, the same thing is true for the median price. The four areas of the South Bay are distinguished from each other by the basic appeal of each area to potential home owners. Comparing real estate from 2024 to 2025 shows a distinct difference between the Beach cities and the other three areas.

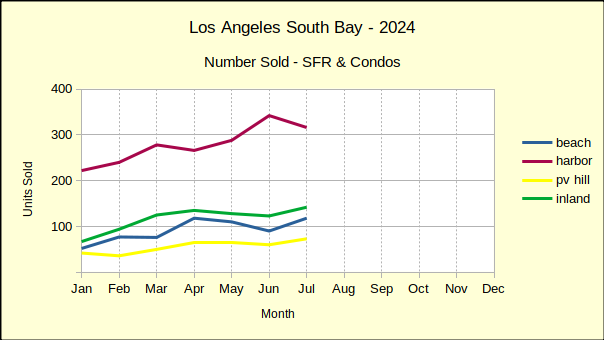

Consider the sales volume, for example. Across the South Bay the cumulative change in the number of homes sold for the first half of each year, shows a 7% increase. However, the Beach area measured in at a 26% increase. The Harbor area was 4%, Palos Verdes peninsula was 2%, and the Inland cities were 3%. Different South Bay buyers are definitely viewing things differently.

Looking at the median price shows a similar story. In the same order, Beach was 11%, Harbor was 1%, Palos Verdes was -1% and Inland was -1%.

Clearly, buyers in the Beach cities have a different perspective than those in the rest of the South Bay. It would take some serious research to study the various purchases, what type of buyer was involved, how the property is currently being used, and how big of a premium the buyer was willing to place on the property, etc., in order to understand the motivations. An early guess is speculation. Buyers with sufficient available resources are speculating that the value will continue to go up without interruption. There might also be some number of those buyers who believe short term rentals will help defray the carrying costs. And probably a few who just want to live at the beach.

The key tying them all together though, is speculation. Those Beach area buyers believe the economy is going to hold and their purchases are going to further advance in value. That opinion appears to be changing though. The June median results for the Beach shifted from positive to negative in what may be an indication of the direction of our economy. We’ll be back next month with an update.

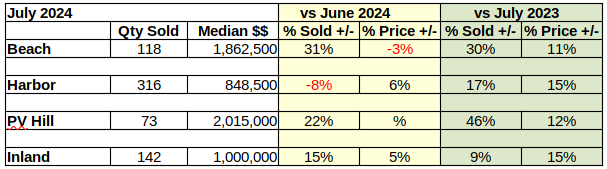

Beach: Mostly Down

Compared to May the Beach cities real estate performance was a bust. June is the second “down” month in succession for the Beach. At 117 units sold, monthly sales volume dropped 4%, after dropping 2% in May. Median prices in the Beach area have been negative since February. The median for June was a mere $5000 below last month’s $1.9M, leaving a statistically insignificant 0% drop.

In year over year sales volume, the Beach did much better, with a 30% increase in the number of homes sold over June of 2024. However, median price took a nosedive from June of 2024, falling from positive 9% in May to a negative 1% in June this year.

Contrasting the first six months of 2025 to the first half of 2024 lends the Beach cities a win. While the South Bay as a whole saw an increase of 7% in the number of homes sold over those sold in 2024, the Beach area jumped by 26%. For the same period of time, Beach prices climbed by 11%, far better than any of the other three areas.

As a point of reference, the number of Beach homes sold in the first half of 2025 is 17% below the number of sales in 2019, the last “normal” business year before the pandemic. Over the same time frame, median prices have increased 54%.

Harbor: Mostly Up

Real estate in the Harbor area showed surprising resilience in June. With 335 homes sold, sales volume was up 14%. At the same time, the monthly median price of $838,000 at the Harbor was up 3% from the prior month.

In the only decline for the Harbor in June, the annual sales volume slipped slightly with a 2% decline. This was offset by a 5% increase in the median price over the same month last year.

Year to date statistics brought even more positive news for the Harbor area. Sales volume for the first six months of the year was up 4% over sales in 2024. The median price was also up, with a modest increase of 1%.

Much like the Beach cities, when looking back to pre-pandemic real estate, the sales volume is 18% below that of 2019 while the median price is up 46%.

Hill: More Down

On the Palos Verdes Peninsula, the only positive number for June was the median price, which rose from $1.85M in May to $1.94M in June, for a 5% increase. Heading the opposite direction, monthly home sales dropped by 34%, ending the month with 49 sales.

In comparison to 2024, PV cities lost ground in sales and in prices. The number of homes sold fell by 18%, while the median price lost 4%.

With the first half of 2025 in history, homes on the Hill appear to have settled in with modest sales volume increases accompanied by small decreases in price. As of June, homes sales are up by 2% and the median is down 1%.

Compared to the first six months of 2019, Palos Verdes volume is off by 9%. For the same period, the median is up 44%.

Inland: And More Down

After four months of sales growth this year the Inland area flipped with a 20% drop from last year. Running the opposite direction from the sales decline, the median price jumped by 11%, coming in at $965,000.

Year over year statistics likewise ended with a drop in the number of homes sold and an increase in the median price. Compared to 2024 sales volume was down 7%, while the median climbed 1%.

At mid-point in the year, the Inland area is posting a 3% increase in sales over 2024 business. That number seems quite reasonable, especially when compared to the monthly sales which range from 18% increase to 20% decrease. While the total number of sales is down, the median price for the first half of the year is up 1%.

Continuing the year to date comparison with pre-pandemic activity, the Inland area is showing sales at 14% less than 2019, combined with a median price at 38% higher than then.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

Inland=Torrance, Lomita, Gardena

Photo by Matthew Davis on Unsplash