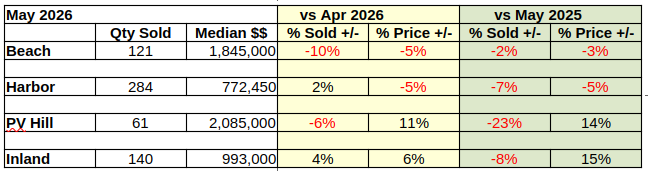

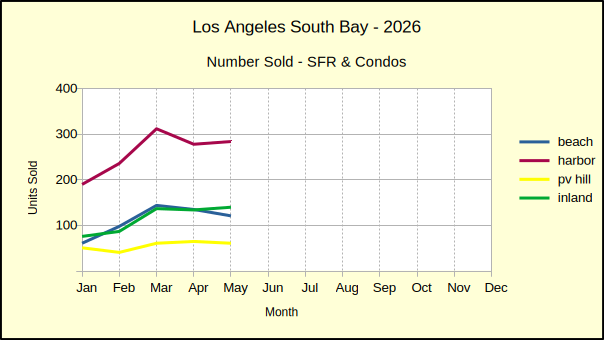

May brought slight improvement to the real estate market in the Los Angeles South Bay. Activity in the number of homes sold compared to April was off 1% across the region, after being down 6% the prior month. After a disappointing 32% drop in January, February and March had rebounded with steep monthly increases in sales. Since then, the war drums sounded in west Asia and sales volume across the South Bay has experienced a significant decline.

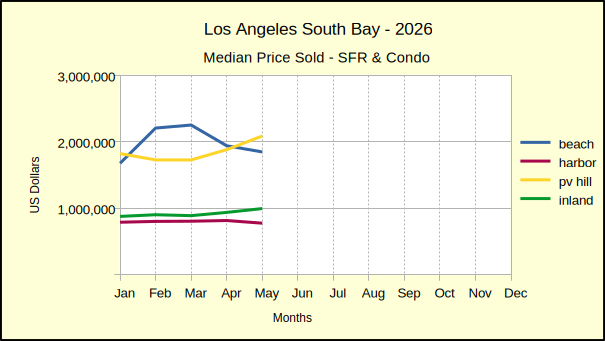

Monthly median prices have continued last month’s negative cast. For example, April and May at the Beach were down 14% and 5% respectively. The Harbor area showed mixed results, ending with a 5% decline in the median price for May. The Inland area is showing solid 5%-6% median price increases in month to month calculations. Prices on the Hill have been positive for the past three months and came in at 11% this month. (As always, one should remember transaction volume on the Hill is low, so a couple of sales can have an out-size impact on the statistics.)

May 2026 vs May 2025

Annually, the number of homes sold dropped in every area of the South Bay. Declines ranged from 2% off at the Beach to 30% off on the Hill. Across the region, year over year sales volume fell 9%. This pattern of decline roughly mirrors the month to month sales activity so far in the second quarter of the year.

Median prices continued to be volatile in May by comparison to the same month last year. The Beach cities once again fell by 3%, just as it did in April. The Harbor area fell 5%, flipping from a 4% gain the prior month. Values in the Inland and Hill areas increased for the second month in succession, this time by 13% and 12%, respectively.

2026 Year to Date vs 2025

Residential sales volume has been on the decline most of this year, in most areas of the South Bay. During the first five months of the year, 2712 homes have sold compared to 2895 for the same period in 2025. As it was last month, this measures out to a 6% decline for the year to date.

The Beach was the only area to show positive growth in May sales with a 4% increase in volume. The largest decline came in the Harbor area with an 11% drop in sales. The Palos Verdes and Inland areas dropped 5% and 7% respectively.

While there have been many instances of decline in median price, the cumulative year to date statistics are still relatively positive. The Beach and Harbor areas both show a 2% increase in the median. At the same time, the median price on the Hill dropped 5%, while the Inland area increased 1%.

The Outlook for June

Home sales for June are projected to continue dropping. Expect month over month declines to be 1% to 2% lower than in May. Annually, sales are anticipated to drop by about 10% compared to last June. Year to date sales are also expected to drop by about 10%.

Continued decline in the number of homes sold will almost certainly impact the median price. Despite historically low inventory, the volatile economic situation has dampened buyers’ enthusiasm. Rather than the “bidding war” environment often seen with low inventory, the current market is watching widespread seller price reductions.

Anecdotal evidence shows some homeowners selling and shifting to a rental in anticipation of recession. These sellers are hoping a market collapse will create an opportunity to profit by buying back into the real estate market after prices collapse. While quite risky, this method started several investment careers during “the great recession.”

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

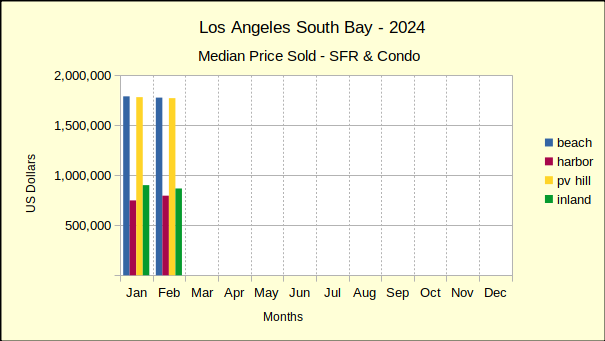

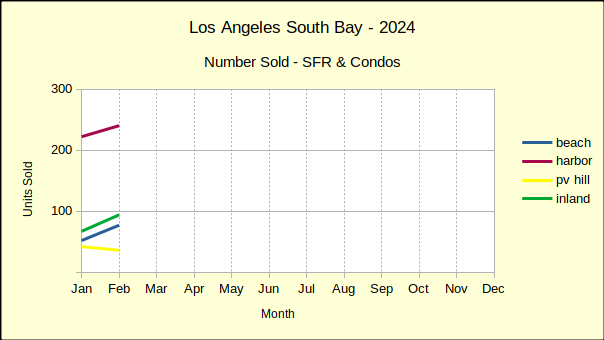

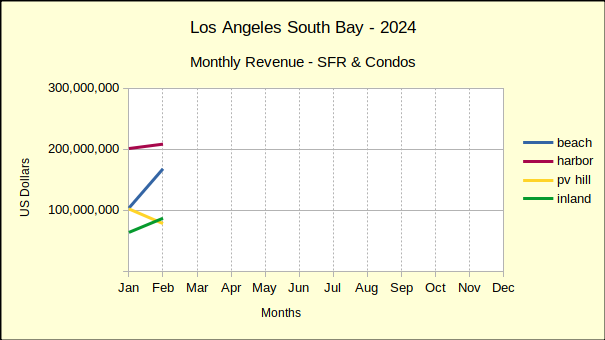

We’re not going to spend a lot of effort talking about month to month real estate activity in this issue. February invariably has more closed sales than January, because the escrows that close in January are for deals that were negotiated in December, when most people were partying instead of buying a home.

The one monthly anomaly screaming for clarity is the 72% increase in monthly sales in the Beach area, while the total increase in sales for the South Bay is only 20%. That’s a real outlier, and we didn’t have an explanation last year when the numbers were nearly the same. In February of 2025 the Beach came in with a 70% increase in the number of sales closed while the total South Bay monthly increase was 24%. The other three areas are normal and the raw totals are normal, except for sales skyrocketing at the Beach for one month. Perhaps there’s a new tax “loophole” happening?

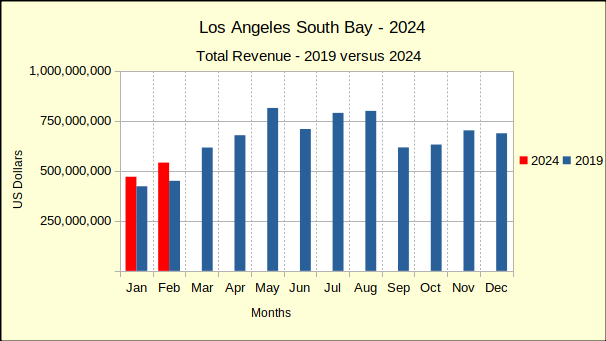

Overall, home sales are still off about 20% from pre-pandemic years. Activity has been gradually catching up, but the projection is for several years of improvement before sales volume is back to what used to be normal. The big surprise in sales volume comes in comparing last month to February of 2025, Last year had shown a solid growth of 19% over February of 2024, with positive numbers in all four areas. This year shows plummetting sales in all four areas, with a drop of 19% across the South Bay.

With that thought in mind, and looking at the year to date, for just January and February, 2024 showed 2% sales growth, and 2025 4% growth. In what appears a total reversal, 2026 is dropping by 18%. It’s still early in the year, so the direction may change. At this point it looks as though economic and war worries may be slowing the number of transactions closing. There was evidence of increased buyer risistance over the last half of 2025. The first quarter figures next month will give a more thorough picture of what to anticipate for the year.

Median Price:

Shifting gear and looking at the median price, shows a similar theme. Once again, the Beach area is showing a super-charged increase in comparison to the balance of the South Bay. The Harbor area was up 1%, the Inland area up 5%, PV down 5%, and the Beach was up 31%!

On one hand, it could be said “Money is migrating to the Beach at an increasing rate.” Or perhaps, “Owners are dumping the Beach for huge profits.” It’s conceivable both are correct. In any event it’s an interesting phenomenon.

Year over year, where the chance to look ahead comes alive, things look much more restrained. The Beach is up 1% in median price, which is significant change from being down 29% in January. At the same time, the Harbor is up 5% and the Inland area is up 2% — all very tame.

Median prices on the Hill dropped by 16%. One needs to remember there is a comparatively small number of homes selling in the PV area on a monthly basis, so one or two unique transactions show up as huge blips in the charts.

Year to date, median prices are more constrained than last year. The Harbor area, the largest of the markets in the South Bay, is up 5% over the same period for 2025. The Inland area is flat, while the Hill is down 10% and the Beach is up 15%.

Continuing on the vein we started at the beginning, the sales being reported now were negotiated in January, before the crisis in West Asia bloomed. This shows a tempered market with pullback in both the number of homes sold and in the median price of those homes. The day to day feel of the South Bay real estate market seems to be continuing on a roughly similar pace, but it will be another month before we can really see the statistical impact. Let’s look again next month.

Beach:

M-m, vol: 91, 72%, med: 2,200,000, 31%

y-y, vol: -17%, med: 1%

ytd, vol: -17%, -13% from 2019, med: -15%, up 63% from 2019

Harbor:

M-m, vol: 220, 21%, med: 800,000, 1%

y-y, vol: -19%, med: 5%

ytd, vol: -22%, -27% from 2019, med: 5%, up 49% from 2019

Hill:

M-m, vol: 36, -27%, med: 1,722,500, -5%

y-y, vol: -22%, med: -16%

ytd, vol: 9%, 10% from 2019, med: -10%, up 36% from 2019

Inland:

M-m, vol: 84, 14%, med: 920,000, 5%

y-y, vol: -18%, med: 2%

ytd, vol: -17, -21% from 2019, med: -0%, up 40% from 2019

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

First glance at the month to month December numbers: A 12% increase in December sales brought smiles to a lot of faces, until they realized this only corrected half of the 23% drop in November sales volume. This past year saw a lot of one-step-forward-two-steps-back. The annual numbers make it look like that will continue to be the pattern into 2026. Median prices found gains for the Beach and the Hill, while prices slid in the Harbor and Inland areas.

Year over year, December sales were mixed, with sales volume dropping at the Beach and on the Hill. At the same time, the Harbor and Inland areas experienced solid increases in sales. Median prices for December showed a reverse pattern, with the median increasing at the Beach and on the Hill, while it dropped in the Harbor and Inland areas. This has all the earmarks of being a market peak.

Without getting into details about the monthly statistics, those are covered below, let’s move on to what the year over year data reveals. In the end, 2025 showed a solid 4% growth in sales over 2024. This broke down as: Beach 10%, Harbor 3%, Hill 6% and Inland 1%. It’s important to note the sales volume over the final four months of 2025 were nearly all lower than the same month in the preceding year, showing a persistent drop in sales. Where the early months of the year were overall positive, despite choppy performance, across the board, there has been a slow decline in comparison to last year.

The year began with double digit increases in sales volume across the South Bay, registering 11% in January and 19% in February. The number of homes sold bounced around a lot during the year and ended with a mere 4% increase in sales volume over 2024, with three months out of 2025 being negative.

A slowing in the sales volume doesn’t necessarily dictate a slowing in the median price, although this year it did. The 2025 median for each area showed a 1-2% increase in price everywhere except the Beach were the median trebled to an astounding 6%. One might suspect a bit of investment fever in pricier neighborhoods. Several decades after being a disreputable neighborhood of the displaced and homeless, the Beach areas have become the place to invest extravagantly.

Interestingly, this aligns neatly with a statement in the Federal Reserve’s Beige Report of 1/14/26. “Several Districts also noted that spending was stronger among higher-income consumers with increased spending on luxury goods, travel, tourism, and experiential activities. Meanwhile, low to moderate income consumers were seen to be increasingly price sensitive and hesitant to spend on nonessential goods and services.”

Note, this is not yet a reversal in price increases, like that seen in 2023, but is a distinct slowing of the increase. The rate of increase has fallen from the double digits of 2021 and 2022 to barely remaining positive at about half the rate of 2024. One could easily envision median prices going negative again in 2026.

Such an event might be readily termed “a correction” given that current median pricing is showing roughly 40% above the median from 2019, the last year prior to the Covid pandemic and associated market disruption. That 40% calculates out to about a 6% annual increase, three times greater inflation than the 2% sought by the Federal Reserve.

It has been said the only reason median prices are still climbing at all is the shortage of homes available on the market. Inventory figures appear to be off about 15% from the peak in 2019, just before the pandemic. When the Fed responded to the frozen market and interest rates plummeted, inventory levels fell equally rapidly. By 2022 inventory had dropped to 50% of the 2019 levels. Those home sales, and the huge refinance boom that accompanied them put roughly 40% of the homes in California on a 3%+/- mortgage interest rate. Those homeowners are only selling if absolutely necessary, which is keeping the inventory artificially low and simultaneously keeping median sales prices artificially high.

Beach:

In December, home sales at the Beach increased to 90 units, or 11% greater than November. As noted above, that did not erase the 23% decrease in sales from October to November. At the same time, the median price increased by 4% to $1,825,500.

Compared to December of 2024, the number of residential sales has declined by 16% while the median price increased 1%.

For the year 2025, the number of homes sold at the Beach increased by 10% over 2024. Versus sales for 2019, the market remains depressed by 19%. Sales volume is increasing slightly, but it feels depressingly slow.

For the same period, the median price increased by 6%, which has inflated 45% since 2019.

Harbor:

By virtue of mathematical probability, the Harbor area is the most stable of the four demographic areas in the South Bay. December home sales at the Harbor rose 14% to 298 units, very much in line with the total South Bay increase of 12% over November numbers. At the same time, the median price fell by $779,275, for 4% drop.

On a year over year basis, home sales this December exceeded sales in December of 2024 by 19%. Opposing the volume gain, the median price declined by 3% for the same period.

Looking at the full year, 2025 saw more homes sold by 3%, with the median price increasing by 1%. The bump up in sales volume can be viewed as positive recovery from over-exuberant financing of the Covid years. The median price increase is simply an aggressive response to the low inventory.

Sales for last year fall 22% the volume in 2019, and median prices are currently 40% above those of 2019.

Hill:

November versus December sales on the Hill brought in a zero change for the 45 units sold. The median price showed an increase of 1% to $2 million even for the final month of the year.

Year over year, December ended at a 10% decline in the number of homes sold in 2025, while jumping up for a 14% rise in the median values of those homes. As always, the small sample size of PV sales may lead to extreme results, so feel free to call if you have a specific question.

For the year as a whole, compared to 2024, 6% more homes were sold on the Peninsula in 2025 and the median price was 2% greater. Compared to 2019, sales volume was down by 17% while the median price was up 46%.

Inland:

The number of homes sold in the Inland area for December jumped 14%, to 116, from November, while the median price fell by 3% to $838,500.

Annually, December 2025 gained 9% in sales volume over the same month in 2024. Median price for that period fell by 6%.

Inland sales enjoyed a 1% increase year over year in 2025, while also seeing a 1% increase in median price. Compared to 2019, sales volume remained suppressed by 19%, while median price ended 2025 with a 33% increase.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

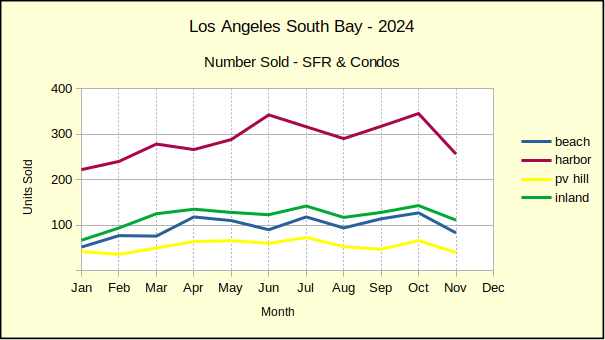

In real estate, sales volume is always a good indicator of market direction, of what buyers are focused on. Looking across this year in the Los Angeles South Bay, with September in the mirror, the number of homes sold each month in comparison to last year, tells a story. The tale starts in January with a healthy 11% increase over January of 2024. In February that number nearly doubled to a 19% increase.

In March the comparison dropped into single digits and through May increases were 2%. 9% and 7%. Buyers were not responding to the homes on the market. Sales were slowing. Then June hit with a zero change and July followed with a -1%—even more slowing. August showed a 10% rebound in sales, frequently attributed to the ‘back to school’ rush of sales closures. For September homes sales dropped back to 0% versus September of 2024.

Essentially much of the annualized increase in the first quarter of the year has evaporated. What was a 30% annual growth is now a 6% growth rate. Delving a little deeper into where in the South Bay changes are occurring shows sales declining in the Beach area (detail below) as well as in the Harbor and Inland areas. Last month sales on the Hill were the only positive influence on the broader South Bay sales statistics (detail below).

The impact of the slowing homes sales across the South Bay can be seen in the falling prices across the region. September is the first month since January where median prices rose in all four areas. The year started with increases across the board and immediately started losing ground in February with a price decline in the Harbor area. For the next six months median prices slid in more than half the sales recorded, see-sawing back and forth across the four areas.

As of now, with the third quarter of the year complete, median prices are up appreciably only at the Beach. Year to date, compared to the same period in 2024, prices of Beach area homes were 9% higher than last year. However, keep in mind, the other three areas are essentially at zero growth versus 2024. Price appreciation at the Beach has remained stronger than the rest of the South Bay, but appears to be faltering as the year goes on.

So, what should one expect for the balance of the year? Sales are 15%-20% below pre-pandemic levels, while median prices are 30%-50% above. Based on the supposed ideal of 2% inflation, those prices should be around 12.5%, or roughly one third of the increase we’re seeing. At least a few financial CEOs are referring to the current environment as an “asset bubble” in the nature of the 2008 collapse.

A good deal of the price appreciation is a result of lower inventory levels which are not expected to recover until the end of the decade. It remains as a reminder of when interest rates were hovering around 3% and home prices were easily inflated. While many are still riding the wave of inflationary increases, many buyers are balking.

At the same time the economy in general is squeezing the typical home buyer with stubborn mortgage interest rates, an increasing cost of living and shrinking paychecks. It seems apparent something is going to give. Jamie Dimon, of JP Morgan Chase, is reported to have said the market could implode within six months, or could last another two years.

Confining the discussion to local real estate, the market appears to be on course to a point where price resistance causes inventory levels to drop enough to compel sellers to lower prices. Extending the spreadsheet out to the end of the year, while continuing the current trend shows homes sales continuing to decline, slipping to about 4% over 2024 levels for the South Bay as a whole. Median prices at the end of 2025 should be slightly lower than they were in 2024. Probably not by a statistically significant margin, but lower.

Beach:

Monthly home sales at the Beach took a 9% hit in September, dropping to 98 units sold. Month to month sales volume has been up and down throughout the first three quarters. While there have been some dramatic swings—like a 40% drop in January, followed by a 70% increase in February—most of the ups and downs have been confined to a much narrower range.

Looking at monthly median prices, September was $1,962,915, up from last month by 5%, the highest gain since it rose 30% in January. Six of the seven intervening months were negative with August being the only other positive month, and that with only a 1% increase.

On an annual basis, September is the first time in 2025 the number of homes sold in the Beach Cities has dropped below same month sales for 2024. Sales volume has dropped several times in month to prior month sales, but this is the first annual decline.

The Beach had been having an unbelievable year, with sales volume increases in the double digits most months. Then, September plummeted from a 15% increase in August to a 14% decline in annual sales. At the same time, median prices repeated the 10% increase experienced in August.

Year to date, through the third quarter, the number of sales stands dramatically higher than the rest of the South Bay. The 17% increase in volume is nearly three times the 6% found across the region. Similarly, the median price at the Beach came in with a 9% increase, while the median across rest of South Bay was 0%. Will the Beach cities continue the out-size performance seen to date? Probably not, but we have three more months to find out.

Harbor:

Monthly sales in the Harbor area dropped 1% in September, falling to 308 homes sold. This follows a 1% increase the prior month. These small monthly swings indicate a stable market, as opposed to the broad double digit sweeps during the early months of the year.

The median price last month was $795,000 up 2% from August. Since the beginning of the year the month to month price changes have all been in single digits and mostly positive. This contrasts sharply with the Beach area, where monthly prices have fallen nearly every month this year.

Year over year, September home sales in the Harbor area dropped 3%. This is effectively a return to the pattern started in June when sales volume began to slide. August was the outlier, up by 7%, similar to the rest of the South Bay in the month before school starts.

Median prices for this September were 5% above last September. It was also the first increase in the median price since June. The median is beginning to look rather flat at the Harbor.

With three fourths of the year gone, the Harbor area appears to be setting the pace for the South Bay. Sales volume has been shifting down since before the summer buying season and currently rests at a 3% increase in the number of homes sold compared to the same period in 2024. Median prices have been moderating, with a year to date increase of 1% over last year at the third quarter.

As an interesting side note, compared to the same period in 2019, sales volume is down 21% (that ten year Covid deficit), and median prices are up 41% (the Covid bubble?).

Hill:

Any conversation about statistics and the Palos Verdes Peninsula needs to start with an understanding that this is a statistically tiny sample and one or two unusual sales can dramatically skew the results. September of this year is a classic example.

Contravening the direction of the rest of the region, September sales on the Hill skyrocketed 36% over August for a total of 80 homes sold. The median price likewise showed a significant increase, jumping 19% to hit $2,143,000.

Comparing this year to last September shows a phenomenal sales volume increase of 70%. This is nearly three times any similar percentage recorded this year. That same upward leap carried across to the median price which came in at a 26% increase; nearly three times any other increase in the region.

Looking at the detail of this anomaly one finds that in a typical September there are somewhere around 60 units sold on the PV Peninsula. Last year there were only 47 homes sold—this year there were 80. Nothing special, just two successive years going opposite directions in a tiny sample.

Despite the scorching monthly numbers, for the first nine months of the the year, Palos Verdes shows a 10% increase over 2024 sales volume. Still a healthy increase, but much more in line with reality. Median price for the year to date is actually a 1% decrease even though the September statistics show increases in the median. Out of nine months, four have been increases while five have been decreases.

Looking back at 2019, the last ‘normal’ year before the pandemic, reveals sales volume is currently 11% above that of 2019 and the median price is up 45%.

Inland:

The Inland cities experienced an 11% sales decline in September, falling to 188 homes sold, after an anemic August increase of only 2%. Yet another indication the residential real estate market is on a downward trajectory. That fall was accompanied by a surprisingly strong 14% increase in the median price, jumping up to $1,006,000. Month to month sales data for the Inland has been relatively consistent so far this year, with ranges often in the double digits.

Looking back to the same month last year shows an 8% drop in the number of Inland area homes sold. This is consistent with the rest of the South Bay, excepting the fluctuating numbers on the hill (see above). The median price, like the South Bay overall, was strongly positive with a 14% increase.

Looking at the Inland area longer term, comparing the first three quarters of 2024 to the first three of 2025 shows a modest increase of 1% in the number of home sales. This is the lowest increase of the four areas in LA’s South Bay. Year to date across the region is a 6% increase in volume. Sjifting focus to the median price, the record shows 0% change, or at best a rounding error in the 2024 versus 2025 median prices.

Once again, looking back to the 2019 baseline, Inland area home sales volume in down 18% from 2019 and the median price is up 33% from 2019.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

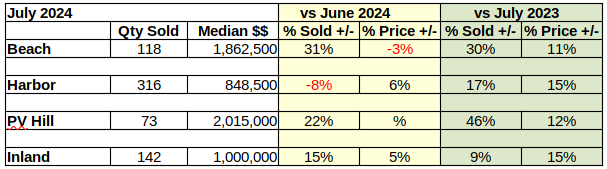

In July the South Bay real estate market made a valiant attempt to maintain a positive stance. It failed. Compared to June of this year, things looked better on the sales volume side, but June was already in the tank, so even the summer bump was only modest help. Looking back to July of last year gave a depressing picture. Overall sales for the south Bay were off by 1%. In itself that’s not a huge number, but considering the market started this year at well over 10%, it’s a big drop in sales.

Median price was an even greater disappointment. In January every area of the South Bay was in positive numbers. By July, every area except PV (which has been negative four out of seven months), was shrinking.

Year to date numbers have overall pointed in an equally negative direction. For the first seven months of the year the South Bay is looking at a 6% increase in homes sold. Compared to the 11% that started the year, one has to conclude the local real estate economy is trending down. The median price tells an even more down-trodden perspective with nearly all areas showing prices falling by 1% to 3% from the same period in 2024.

Beach: A One Month Jump?

The number of homes sold in the Beach cities during July jumped to 130 units, up 11% from June sales. Keep in mind, the increase follows a 4% drop in June, which followed a 2% drop in May. Month to month sales have been erratic at the Beach, while annual sales volume has been steeply up compared to 2024. July sales continued the trend with a 10% increase over the same month last year.

Median price is another matter. At the Beach the median came in at $1,844,000, down 3% from June. July was the sixth successive decline in month to month median prices for the Beach area. Annually the median has shown mixed results compared to 2024, ranging from a 32% increase in January to a 1% decline in July. This drop in July followed another 1% decline in June, continuing what looks like a year long slide in median price and in sales volume. While still higher than in 2024, July was the second lowest month this year in terms of homes sold.

Cumulative sales for 2025 were 23% higher than 2024, though still down 15% from 2019, the last normal year of business preceding the pandemic. For the same period, the median price is up 9% over last year, while coming in at 49% above the median in 2019.

Harbor: Volume and Median Down

July was not a positive month for the Harbor area. Compared to June, sales volume and median price both fell by 8%. The number of homes sold for the month fell to 307 units, while the median price dropped to $775,000. This was the steepest monthly drop seen at the Harbor in 2025.

Annual statistics weren’t any better. Looking back to July of 2024, shows sales volume declined by 3%, and the median price fell 9%, the largest annual drop this year. If the current trend continues for the balance of the year, Harbor area real estate may take a serious hit.

Year to date sales through July came in at 3%. While still positive, it’s important to note the Harbor started the year with sales volume at 10% and has been dropping all year. Similarly, the median price has gone from 1% up in January to 9% down in July, ending the first seven months falling by 1%.

A quick comparison to 2019, shows year to date sales volume still down 20% from pre-pandemic business. Median price is still 43% above the 2019 median.

Hill: Strikingly Good

The Palos Verdes Peninsula saw a strikingly good real estate market in July. Month over month sales climbed an astonishing 53%. Of course, it’s not so impressive when one notes that sales dropped 34% last month. Even at that, 75 homes were sold in July, well above the average sold in any month for 2024 and the highest number in yet this year. At $2,185,000, a 13% increase over June, the median price was likewise the highest month for 2025.

Though not as dramatic, the year over year statistics were also impressive with a 3% increase in the number of homes sold compared to July of 2024. Increasing at 8% over July of last year, made PV the only area with a positive median price this month.

Viewing 2025 versus 2024 year to date sales brought another increase of 2%, roughly on par with the rest of the South Bay. Then came the only negative on the Hill for July—a drop of 1% in the median price.

Year to date sales compared to 2019 are still down by 11% , while the median price remains up by 44% from 2019.

Inland: Long Term Slowdown

July versus June numbers showed surprising strength for the Inland area. Those cities kicked the sales volume by 15%, with the number of homes sold climbing to 131 units. While boosting the median price 1%, to $979,000, the Inland area topped the market except for the highly volatile PV peninsula.

The monthly trend reversed with the annual statistics. July 2025 compared to July 2024 showed a 8% drop in the number of sales, accompanied by a 2% drop in the median sales price.

Year to date for the first seven months came with mixed results. Sales volume showed a 1% increase. For the same period, the median price dropped 3%, ending very much like all areas except the Beach, which continued to show positive results.

Once again looking back to 2019, before the real estate market was irremediably shaken by the Covid pandemic, current sales are down 15% and median prices are up 36%. With five months left in the year and economic forecasts leaning toward stagflation, this could well be a tipping point.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

As 2025 rolls by the real estate market in the Los Angeles South Bay continues to slide downward. January started the year with 11% more homes sold than in 2024. Now, with June in the books, the difference is 0% growth in sales across the South Bay. From month to month the numbers are up and down, but the end result is down.

With the exception of the Beach cities, the same thing is true for the median price. The four areas of the South Bay are distinguished from each other by the basic appeal of each area to potential home owners. Comparing real estate from 2024 to 2025 shows a distinct difference between the Beach cities and the other three areas.

Consider the sales volume, for example. Across the South Bay the cumulative change in the number of homes sold for the first half of each year, shows a 7% increase. However, the Beach area measured in at a 26% increase. The Harbor area was 4%, Palos Verdes peninsula was 2%, and the Inland cities were 3%. Different South Bay buyers are definitely viewing things differently.

Looking at the median price shows a similar story. In the same order, Beach was 11%, Harbor was 1%, Palos Verdes was -1% and Inland was -1%.

Clearly, buyers in the Beach cities have a different perspective than those in the rest of the South Bay. It would take some serious research to study the various purchases, what type of buyer was involved, how the property is currently being used, and how big of a premium the buyer was willing to place on the property, etc., in order to understand the motivations. An early guess is speculation. Buyers with sufficient available resources are speculating that the value will continue to go up without interruption. There might also be some number of those buyers who believe short term rentals will help defray the carrying costs. And probably a few who just want to live at the beach.

The key tying them all together though, is speculation. Those Beach area buyers believe the economy is going to hold and their purchases are going to further advance in value. That opinion appears to be changing though. The June median results for the Beach shifted from positive to negative in what may be an indication of the direction of our economy. We’ll be back next month with an update.

Beach: Mostly Down

Compared to May the Beach cities real estate performance was a bust. June is the second “down” month in succession for the Beach. At 117 units sold, monthly sales volume dropped 4%, after dropping 2% in May. Median prices in the Beach area have been negative since February. The median for June was a mere $5000 below last month’s $1.9M, leaving a statistically insignificant 0% drop.

In year over year sales volume, the Beach did much better, with a 30% increase in the number of homes sold over June of 2024. However, median price took a nosedive from June of 2024, falling from positive 9% in May to a negative 1% in June this year.

Contrasting the first six months of 2025 to the first half of 2024 lends the Beach cities a win. While the South Bay as a whole saw an increase of 7% in the number of homes sold over those sold in 2024, the Beach area jumped by 26%. For the same period of time, Beach prices climbed by 11%, far better than any of the other three areas.

As a point of reference, the number of Beach homes sold in the first half of 2025 is 17% below the number of sales in 2019, the last “normal” business year before the pandemic. Over the same time frame, median prices have increased 54%.

Harbor: Mostly Up

Real estate in the Harbor area showed surprising resilience in June. With 335 homes sold, sales volume was up 14%. At the same time, the monthly median price of $838,000 at the Harbor was up 3% from the prior month.

In the only decline for the Harbor in June, the annual sales volume slipped slightly with a 2% decline. This was offset by a 5% increase in the median price over the same month last year.

Year to date statistics brought even more positive news for the Harbor area. Sales volume for the first six months of the year was up 4% over sales in 2024. The median price was also up, with a modest increase of 1%.

Much like the Beach cities, when looking back to pre-pandemic real estate, the sales volume is 18% below that of 2019 while the median price is up 46%.

Hill: More Down

On the Palos Verdes Peninsula, the only positive number for June was the median price, which rose from $1.85M in May to $1.94M in June, for a 5% increase. Heading the opposite direction, monthly home sales dropped by 34%, ending the month with 49 sales.

In comparison to 2024, PV cities lost ground in sales and in prices. The number of homes sold fell by 18%, while the median price lost 4%.

With the first half of 2025 in history, homes on the Hill appear to have settled in with modest sales volume increases accompanied by small decreases in price. As of June, homes sales are up by 2% and the median is down 1%.

Compared to the first six months of 2019, Palos Verdes volume is off by 9%. For the same period, the median is up 44%.

Inland: And More Down

After four months of sales growth this year the Inland area flipped with a 20% drop from last year. Running the opposite direction from the sales decline, the median price jumped by 11%, coming in at $965,000.

Year over year statistics likewise ended with a drop in the number of homes sold and an increase in the median price. Compared to 2024 sales volume was down 7%, while the median climbed 1%.

At mid-point in the year, the Inland area is posting a 3% increase in sales over 2024 business. That number seems quite reasonable, especially when compared to the monthly sales which range from 18% increase to 20% decrease. While the total number of sales is down, the median price for the first half of the year is up 1%.

Continuing the year to date comparison with pre-pandemic activity, the Inland area is showing sales at 14% less than 2019, combined with a median price at 38% higher than then.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

The real estate market in the Los Angeles South Bay kicked off 2025 with an 11% increase in the number of residences sold for January. That increase in sales volume was accompanied by median price bumps that ranged from 0% in the Inland area to 32% in the Beach cities.

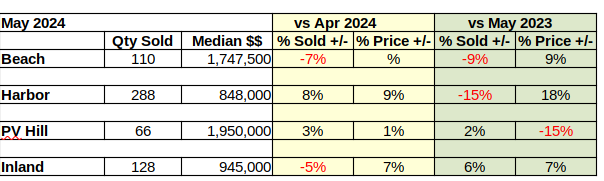

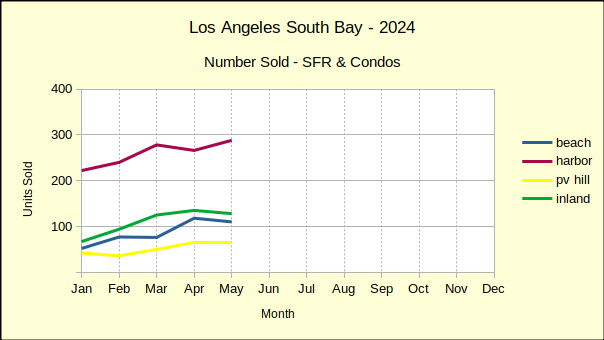

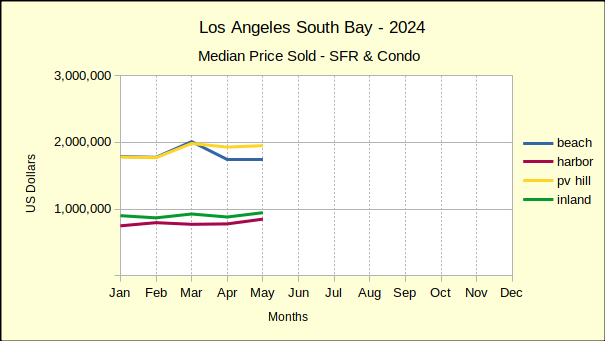

Fast forward to May, almost halfway through the year, and the sales volume has dropped to a 7% increase over May of last year. With the number of homes selling declining, the median prices have likewise moved from the positive side to the negative. Comparing the median prices to May of last year shows prices falling in three of the four South Bay areas. Only the Beach cities managed to stay positive with a 9% increase, albeit compared to 32% in January. The other three areas dropped by as much as 8%. (See below for more detail.)

This South Bay Market Snapshot shows where the market is shifting and by how much. It’s designed to help clients understand the direction of the market. Those who watch the market trend will see increasing larger chunks of real estate market are sliding toward recession either in the number of homes sold for a given period, or correspondingly dropping in median price. The mid-year report next month should provide a more definitive comment on the future of local real estate.

Beach: Still Up, but …?

May was not a good month for real estate in the Beach cities, but it was better than last May. The month over month statistics are red ink, with the number of homes sold dropping by 2% and the median price falling 3% from April. Sales volume came in at 122 units, compared to 125 in April. The median price was $1,900,000 down from $1,955,000 last month.

Annual sales volume was more impressive at 11% increase in the number of homes sold. Similarly, the median price at the Beach escalated by a relatively high 9%, compared to the other areas of the South Bay.

Year to date, 541 homes have sold in the Beach area, 25% greater than the first five months of 2024. At $2,000,000 the median price surprises, since the median month to month is only $1,900,000. How could the median for the year to date, be higher? Well, looking at the past few months shows Beach area prices started the year much higher than they are now. In fact, the median in January was $2,355,000—almost $400,000 higher than May. Beach area median prices have been falling every month this year.

Harbor: Sales Slipping, Prices Down

Month over month, sales volume in the Harbor area dropped by 5%, from 310 homes in April to 293 in May. Surprisingly, the median price climbed from $785,000 to $815,000, for a boost of 4%.

Comparing this May to the same month last year gives similarly mixed results, though in reverse. While monthly home sales found May lower than April, annual sales were up 2% from May of 2024. In the same time frame, median prices fell 4% across the year.

For January through May of 2025 the number of home sold rose 6% from last year, for a total of 1373 properties closing escrow. During the same period of time the median price rose 1%, ending at $785,000.

Hill: Sales Solid, Prices Down

Home sales on the Palos Verdes Peninsula for the month of May delivered an increase of 1%, totaling 74 homes. In May, the median price likewise went up, reaching $1,850,000, or 4% more than those sold in April.

Looking at sales volume year over year shows a more varied picture. Last month compared to May of 2024 offers a 12% increase in the number of homes sold. At the same time, the median price tumbled by 5%. One should always be cautioned that with the small number of transactions in peninsula homes, percentages often seem exaggerated, thus it’s important to look at the year to date statistics, too.

For the first five months of 2025 275 homes were sold on the Hill, boosting sales volume by 7% over that of 2024. While the volume came up, the median price went down. At $1,897,000 the median dropped by 2%. It would seem a correction was in the making, though that’s based on memory of other financial “compressions” in recent years.

Inland: Median Prices Continue Down

Monthly sales statistics brought a 12% jump in homes sold in the Inland area. This increase is easily the steepest in the South Bay for May. The next closest rise in sales was the Palos Verdes area with a 1% bump over April volume. The 143 homes sold at a median price of $870,000, a 1% drop from the April median.

The Inland area joined the Hill in yearly sales increases. Both areas registered a 12% jump in volume, coming in at the top, with the South Bay as a whole rising by only 7%. Continuing a trend started in March, Inland median prices once again fell, this time registering the steepest drop across the South Bay, falling 8% below last year’s May numbers.

As the calendar barrels toward mid-year Inland sales volume for the year to date has climbed 5% over 2024 to 575 homes sold. Median prices for the same period rose a very modest $10, settling at $900,000, effectively a 0% increase.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

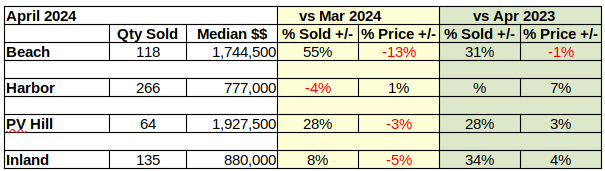

The first two months of 2025 looked generally good. Not necessarily strong, but sales were more or less pluses compared to 2024. By the time March rolled around things were starting to look less positive. Sales were dropping in most neighborhoods and double digit increases were pretty much a thing of the past. With April the number of homes closing escrow actually increased, except for the Inland area.

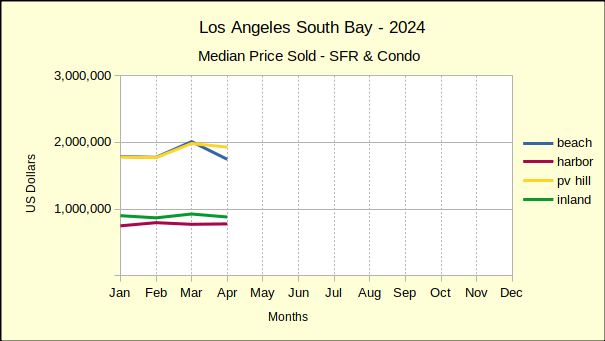

Median price is another story. While prices have continued to escalate at the Beach, they have flattened in the Harbor area and dropped into negative territory everywhere else. The year to date statistics for median price are still ok, but beginning to look like a recession in the making.

Like the rest of the world’s economy, South Bay real estate in 2025 is volatile. From one month to the next there is hardly any continuity. Looking across the year to date activity is seems clear both sales volume and prices are sliding.

Sales volume is expected to remain below prior years for some time. This is a reaction to the extremely low interest rates attached to homes purchased during the pandemic. Those owners are holding on to those properties and rates for as long as possible. Compared to 2019, the last year before pandemic influenced real estate, sales volume has consistently been 5% to 15% lower.

On the other hand, median prices have jumped consistently. South Bay median prices are anywhere from 40% to 70% higher than in 2019. That inflation appears to have begun receding in the Harbor and Inland areas. It has slowed but not reversed at the Beach or on the Peninsula.

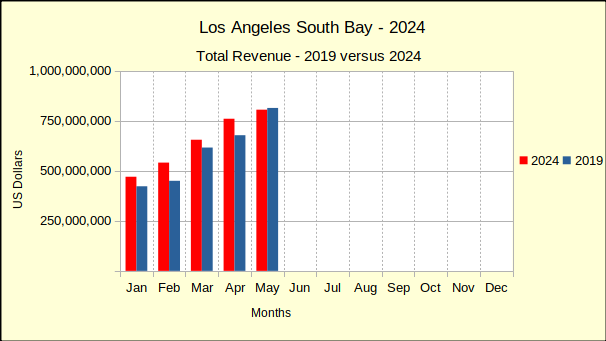

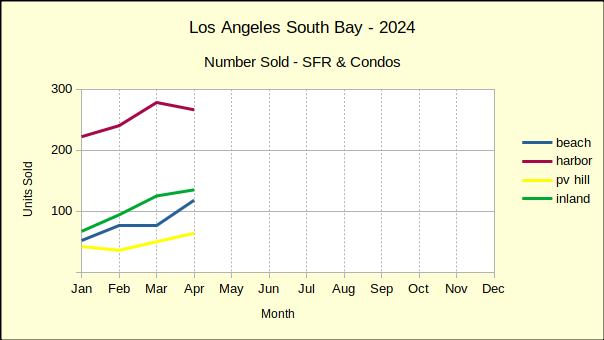

Beach: Starting to Weaken

The number of homes sold in the Beach cities during April increased to 125 units, or 3% over March. Looking at year of year sales volume, 6% more were sold in April of 2025 as were in the same month of 2024.

Median prices were mixed, coming in at $1,955,000, 2% below March of this year. Annually, the April median was 12% above April of last year.

Year to date for the first four months of the year, 419 homes have sold for a 30% increase over sales in 2024. The median price of $2,090,000 represents a 17% lift from last year.

Harbor: Sharply Slower

April sales volume in the Harbor area jumped by 23% above March, ending at 310 homes sold. Annually, that came in at a 17% increase above April of 2024.

Like the Beach, Harbor area median prices dropped 2% from March sales, registering at $785,000. Comparing that to the median in April of 2024 showed an increase of 1%.

Looking at the longer perspective, 1080 homes sold in the Harbor area year to date through April, for a increase of 7%. For the same period of time, the median price was flat at $772,500.

Hill: Prices Negative

On the Palos Verdes peninsula 73 homes were sold in April, an increase of 46% over March. That monthly increase far over-shadowed the year over year increase of 14%. It’s important to remember that activity on the PV Hill is lower than any of the other areas measured here, and is subject to some rather dramatic statistical swings.

While the number of sales increased monthly and annually, the median price dropped in both categories. At $1,783,560, April’s median price was 10% below that of March. April of 2025 came in 7% below the same month in 2024.

The first four months of the year saw 5% sales increase with 201 homes sold. For the same period, the median price rose 4% to $1,935,000.

Inland: Mostly Down

Monthly, sales in the Inland area climbed to 128 homes, for a 12% increase. At the same time the year to year sales volume fell 5% from April of last year.

The median price in April was $877,500, a drop of 4% from March while remaining the same as April of 2024.

Year to date sales of 432 homes was a 3% improvement over the first four months of 2024. For the same period, the median price of $900,000 represented a 1% increase.

Beach=Manhattan Beach, Hermosa772,500 Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

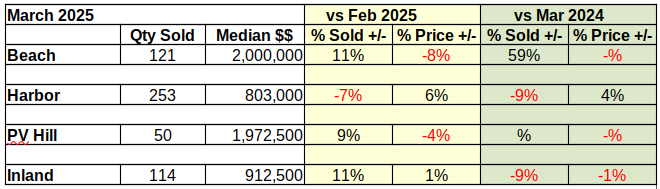

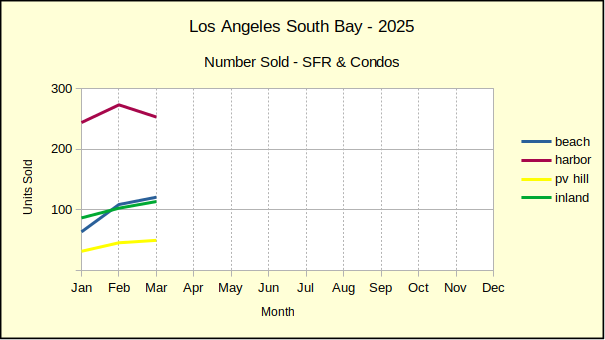

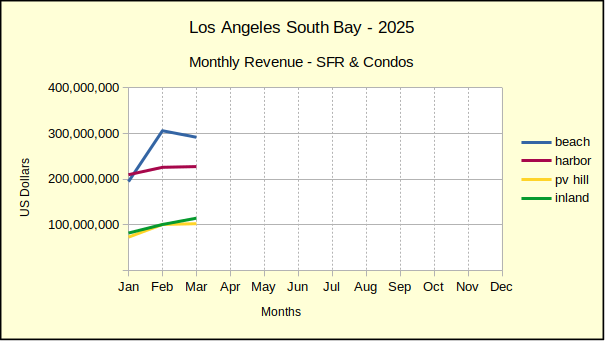

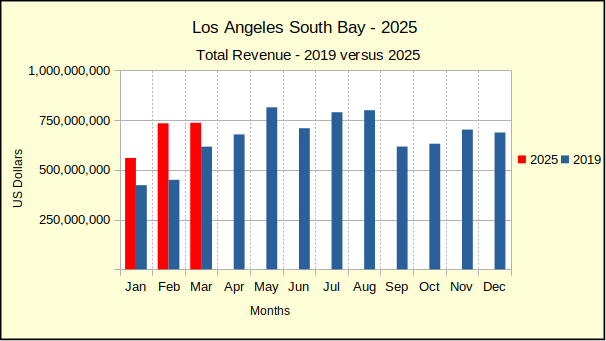

March was not a good month for sellers of South Bay realty. Median prices for residential property collapsed into red territory for nearly all areas. Sales volume was right behind it with falling numbers everywhere except the Beach cities. Even at the Beach, where the number of homes sold rose, the median price went negative.

So to what should this market slow down be attributed? Is it the elevated interest rates? Probably not, since mortgage rates have actually come down, albeit only slightly. Perhaps it’s a lack of inventory? Not likely, as there are more homes on the market in most neighborhoods. Tariffs? There are none on real estate. Has inflation driven off the buyers? Possibly. Median home prices are up in a range from 40% to 74% across the South Bay, though most of that price jump occurred when mortgage interest was toying around the 3% area.

Economic chaos is probably a more accurate answer than any other. Investors like stability, which is not in evidence today. Right now, investors can’t tell from one day to the next, whether to expect recession or inflation. In order to buy low, or to sell high, it’s necessary to know which direction the economy is going. When they can’t tell, investors park their money in the least volatile place they can find.

It’s often called the “investor flight to safety.” So, when the IMF warns of “major negative shock” to the international economy, investments shift to gold and bonds. Right now, both are doing quite well. At some point the investment community will decide real estate has fallen as far as it’s going to, and then we’ll return to—inflation.

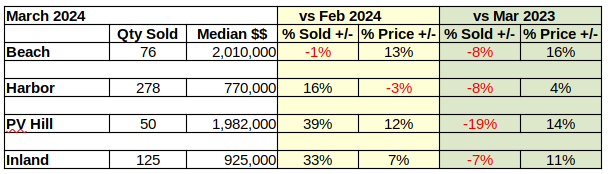

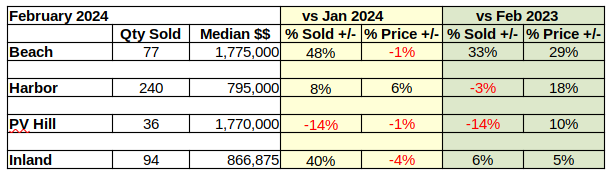

Beach:

Monthly home sales in the Beach cities climbed 11% above February, while the median price plummeted by 8%. The number investor flight to safety.of homes sold increased from 109 in the prior month to 121 units in March. The median price dropped $180,000, ending the month at $2,000,000.

On a year over year basis, the sales volume was even more insane, with 59% growth over March of 2024. The last time the local market saw sales numbers this high was during the pandemic, when interest rates were at rock bottom. The craziest part of the story—is seeing that with all those sales, the median price for March actually dropped $10,000. The decline was small enough to register as a 0% change.

Year to date comparisons to the first three months of last year showed similarly divergent percentages, though not quite as radical. Sales volume for the first quarter of 2025 exceeded 2024 by 43%. For the same period of time, the median price at the Beach rose an astonishing 22%. This compared to low and negative numbers across the rest of the South Bay for both sales volume and median price.

Harbor:

Talk about diverse—the Harbor area did a complete 180º turn on the Beach area. Monthly, the Beach was: volume – up, median – down; the Harbor was volume – down, median – up. The Harbor came in with a 7% drop in number of homes sold, falling to 253 units from 273 last month. The median sale was $803,000, a 6% increase over last month’s $760,000.

The same diversity, or is it perversity, kicked in on the yearly statistics. Compared to March of 2024, this year the Harbor area dropped 9% in the number of homes sold, while the median price of those homes climbed 4%.

First quarter home sales at the Harbor continued to climb, though not as aggressively as the Beach area. The sales volume rose 4%, which is more in line with business on the Hill and for the Inland area. For the same time frame, the median price fell 1%.

Hill:

Month to month sales in Palos Verdes showed a 9% increase, climbing from 46 units in February to 50 in March. While the number of homes sold climbed, March saw a 4% drop in the median price.

Comparing March of 2024 to this March brought 0% change for both the number of homes sold and the median price. Exactly 50 homes sold in both years. The median price actually declined by $10,000, though the change was statistically insignificant.

There was also no change to the sales volume for the first three months of this year. Median price on the Hill rose 11% for the first quarter of 2025.

Inland:

While March brought 11% growth in the number of homes sold compared to February, the Inland area challenged market pressure and registered a 1% increase in the median price. With 114 sales for the month, compared to 103 for last month, the Inland area maintained positive volume. At the same time, the median price improved by $12,500, up from the February median of $900,000.

Annually, March flipped the statistics, with both the sales volume and the median price dropping. Home sales fell by 9%, the same decline the Harbor area experienced. The median price was off 1%, which doesn’t seem like much until compared with the 40% growth since 2019.

Year to date the Inland area showed 6% growth in the number of homes sold compared to the first quarter of 2024. Like the Harbor area, the Inland area delivered a significant drop in the median price, coming in with 0% change.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

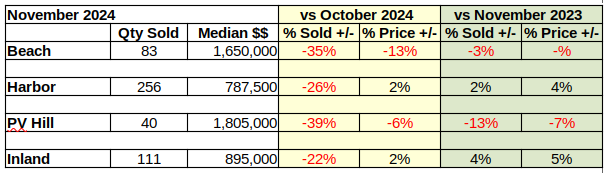

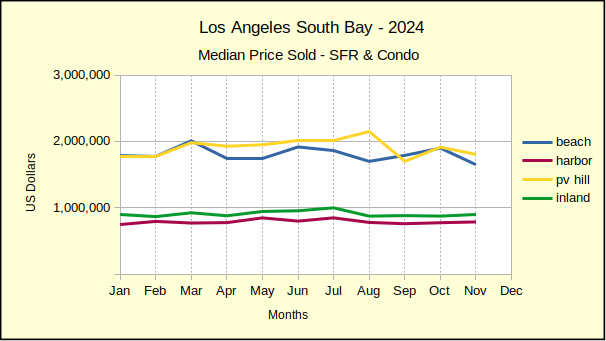

On the heels of an encouraging October real estate market, November saw the South Bay market plummet into the red. Compared to last month the number of homes sold fell by nearly 30%, while the median price collapsed at the Beach and on the Hill. At the same time, the Inland and Harbor areas showed modest growth in median price, posting a 2% gain in both areas.

This was a surprising downturn following across the board sales growth in the October market, accompanied by generally positive price appreciation.

Looking at year over year, same month sales provides a slightly more positive result. Both the Beach and the Hill show the number of homes sold down by 3% and 13% respectively. The Harbor area maintained sales growth of 2% while the Inland area increased by 4%. Both areas were off substantially from the 20-30% increases of October.

Year over year median prices were equally depressed. The Beach and the Hill, the high end of the South Bay market, both lost ground in the single digits. The Harbor and Inland areas, which make up the bulk of sales in the South Bay, grew at 4% and 5% respectively.

It’s too early to attribute this shift to the election results because most of the transactions closing escrow in November would have been negotiated in October. If anything, the decline reflects nervous anticipation leading up to the election. December sales will provide a much more definitive indication of how the public has reacted to the election results.

For right now we know that current sales volumes are running about 10% below December of 2023. And, we know that December last year was lower than December 2019 by 30%. Back at the end of October conditions seemed to be improving, but today it would seem we are still trying to climb out of the Covid trough.

Beach: Sales Off 35% for November

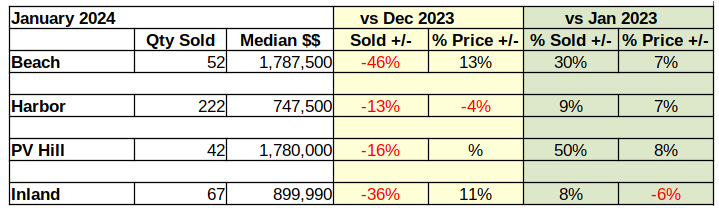

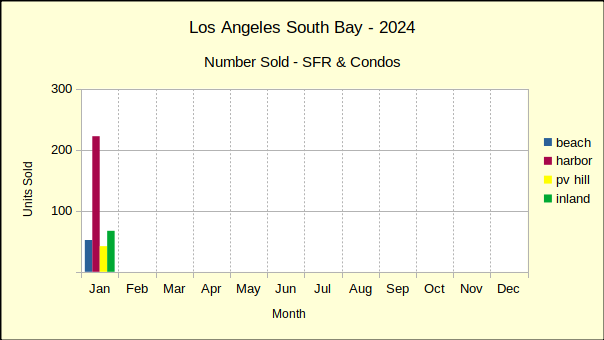

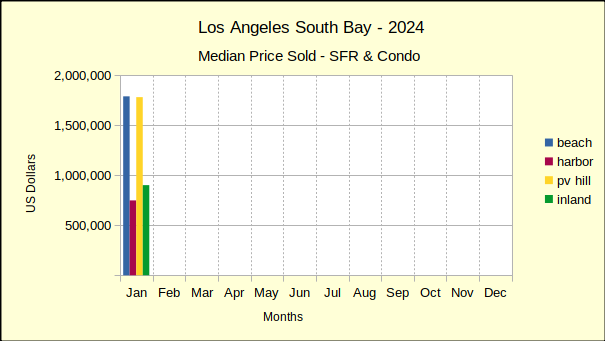

The number of homes sold in the Beach Cities dropped from 127 in October to 83 in November showing a 35% decline for the month. At the same time the median sales price dropped from $1.9M in October to $1.65M in November for a loss of 13%.

On an annual basis sales volume was off by 3% compared to last November, while the median price was flat.

Year to date, 1,059 Beach homes have been sold compared to 1007 during the first 11 months of 2023. This is a 5% increase in the number of homes sold. The median price rose 7% from $1,675,000 last year to $1,787,500 year to date.

Harbor: Sales Fall 26% in November

Harbor area home sales plunged 26% from October, dropping to 256 units from 345 sold last month. At the same time the median price climbed 2%, to $787,500 from $775,000.

On the flip side, same month, last year sales moved the opposite direction, rising 2% this year compared to 252 homes sold in November of 2023. The median price this November was up 4% over the $760,500 recorded in November of last year.

With only one month remaining in the year, the Harbor area displays modest increases in both the number of homes sold so far this year and the median price of those homes. Annual sales have reached 3,160 to date, 3% higher than last year’s 3,076. Median prices for the year have climbed from $740,000 last year to $780,000 this year.

Hill: Market Drops 39% for the Month

Home sales on the Palos Verde Peninsula dove down 39% from October to November, wiping out all but 1% of last month’s gain. As mentioned in the October issue, during the last quarter of 2023 mortgage interest rates were hitting around 8%, which drove the South Bay market to a standstill. The fact 2024 sales volume is falling below 2023 is a concerning matter. Interest rates are once again pushing up against 8%, which has been an impenetrable barrier in recent years. While the number of homes sold dropped precipitously, the median price came in with only a 6% decline, falling from $1,914,500,in October to $1,805,000 in November.

Comparing November of 2023 to November this year turned up a steep fall again. This year brought a sales volume decrease of 13% accompanied by another 7% drop in the median price.

As 2024 heads for closure, the dramatic swings of earlier in the year are mellowing out. Through November, the 597 sales on the Hill have settled in at just 1% above last year. Similarly, the median price, which has ranged from an increase of 26% to a decrease of 15% throughout the year, is coming in at 3%, or $1,927,500.

Inland: Home Sales Collapse by 22%

November sales of 111 homes in the Inland area totaled a 22% drop from the 143 sold in October, rounding out a total decline of 28% for South Bay real estate this month versus last month. Despite the fall in month to month sales volume, the Inland area enjoyed a 2% increase in median price over October.

Same month last year sales increased by 4%, moving up from 107 units in 2023. At $895,000, the median price for November Inland area homes was up by 5% over the $851,000 of last year.

Looking at year to date sales volume of 1,313 shows a mere 1% increase over January-November of 2023 when 1,302 homes sold. Median price fared higher, with a 3% jump from $867,500 to $895,000 this year.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

It looks like the real estate market is finally climbing out of the Covid trough. Each passing month this year has shown red ink, mostly on sales volume, and a lot on median price as well. October brought some relief in that the number of homes sold is up in every area, and median prices are only down in half the South Bay.

The number of South Bay homes changing hands has varied considerably since 2019. Sales staggered briefly after the spring shutdown in 2020, then recovered mid-year as the interest rate continued down. Rock bottom interest rates pulled in buyers and homes flew off the market with bidding wars. In the final quarter of 2022 sales plummeted and the buying spree ended.

Year

Homes Sold

2019

7,100

2020

8,581

2021

10,279

2022

7,616

2023

6,481

2024proj

6,636

If this is indeed the beginning of a normal real estate market again, it’s possible to see reaching the pre-pandemic sales volume in 2025, but more likely in 2026.

The median price is another story. Interest rates were hovering around 3.5% in spring of 2020. The Federal Reserve opened the money spigot to keep the economy flowing while everyone was locked down. For about 15 months mortgage interest rates were below 3%. Historical data sourced from Freddie Mac shows that rates dropped below 4% starting in June of 2019 and lasting until March of 2022. Nearly three years of sub 4% rates makes the current +/-7% a significant deterrent to buying a new home or trading up.

During that period, buyers took advantage of the low rates to boost their offering prices for homes, creating a sellers’ market and bidding wars. The median price sky-rocketed in 2021 and continued through the first of the next year. In summer of 2022, median prices started falling and dropped until late in 2023. Across the board, median prices have been modestly positive since the beginning of 2024.

Certainly it’s all relative, and the market is adjusting, both on the side of higher prices and higher interest rates. But, with today’s median prices roughly 40% above 2019, the number of buyers who can qualify for the necessary loan is way down. A 2024 Q3 estimate from the California Association of Realtors shows only 15% of households in Los Angeles County can afford the median priced home. That compares to 56% in 2012, which leaves a lot of buyers on the sidelines.

The election is over and the incoming administration is clearly pro-corporate. Over the next couple months the dynamics of the shifting markets will become clearer. By the new year we should have a better understanding of the impact to our local real estate. As of October, declines are leveling off and sales are starting to pick up.

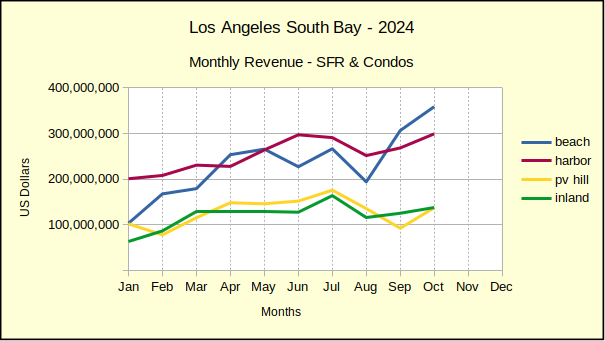

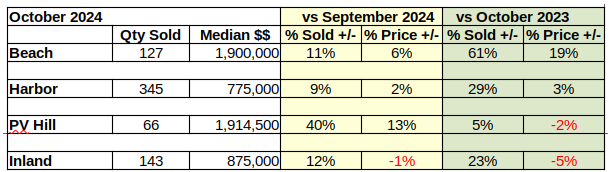

Beach: YTD Sales Up 6%, Prices Up 7%

The number of homes sold in the Beach cities increased by 11% in October, rising from 114 in September to 127. The median price of Beach properties went up from $1,790,000 to $1,900,000, a 6% jump in monthly figures.

Annually, October this year showed a whopping 61% increase in sales over October of 2023, climbing to 127 homes this year versus 79 last year. Over the same one year span, the median price rose 19%.

In view of the huge increase, it’s important to note that October of 2023 is the month mortgage interest rates started toying with 8%, which the buying public simply wasn’t accepting. While lenders and the Fed worked to lower rates, real estate was “in the tank” for last quarter of the year. After the beginning of 2025 the year over year percentages should level out.

January through October, the number of homes sold this year hit 976, 6% more than were sold in the same time period of 2023. Median price at the Beach climbed to $1,788,750 for a 7% increase over last year.

Harbor: YTD Sales Up 3%, Prices Up 4%

October sales in the Harbor area came in at 345 homes for a 9% increase over September. The median price was $775,000, up 2% from the prior month.

Looking at year over year for the same month, this October showed a 29% improvement over the 267 homes sold last year. As noted earlier, home sales took a significant drop in the last quarter of 2023 due to mortgage interest rate hikes. The year over year median price was a much more reasonable 3% increase.

For the first ten months of the year, sales volume has gone up by 3%, to a total of 2,904 homes sold. Over the same period, the median price has jumped up 5% to $778,500.

Hill: YTD Sales Up 2%, Prices Up 5%

On the PV Peninsula, October sales outpaced September by 40%, coming in with 66 homes sold versus 47 the preceding month. It’s important to remember that the Palos Verdes market is the smallest of the South Bay, so a handful of transactions can make a huge difference in either, the sales volume or the median price. The steep increase in sales was accompanied by a more modest increase of 13% in median price, ending the month at $1,914,000.

Comparing October to the same month last year reveals a 5% boost to the number of homes sold. On the other hand, the median price took a fall, dropping by 2%.

Year to date, home sales on the Hill have increased 2%, from 544 in 2023 to 557 this year. For the same ten months, the median price went up 5% to $1,938,750.

Inland: YTD Sales Up 1%, Prices Up 2%

Home sales in the Inland area have been stable, with an increase of 12% in the number of transactions, from 128 properties sold in September to 143 in October. A 1% drop in the median price from last month to this brought the median down from $882,500 to $875,000.

Annual sales in October of this year ended 23% higher than October of 2023. The median price, going the opposite direction, fell 5% from $917,000 last year.

Continuing the relatively modest numbers, the Inland area has risen 1% in the number of homes sold year to date, The 1202 sales reported so far, compare to 1195 sold in 2023. Similarly, the median price is up 2%, having risen from $871,250 last year to $891,245 this year.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

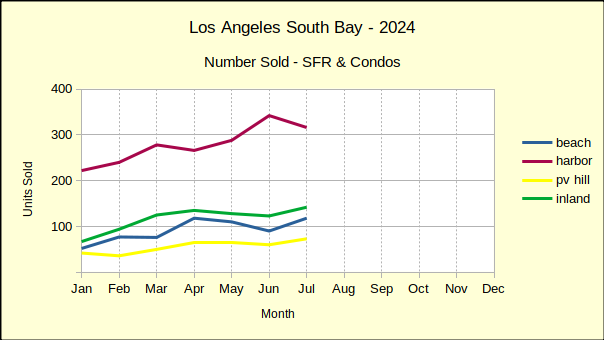

July brought a bonanza—of sorts—to real estate in the Los Angeles South Bay. Sales volume, which had been falling below last year for three of the last four months jumped up 20%. Granted, July was an unusually slow month in 2023, compared to most years including 2024.

Month over month showed a comparable increase. Total sales volume was up 6% from June to July. The only negative for monthly sales was in the Harbor area where activity was off by 8%.

More importantly, year to date through July, sales volume was up 1% across the South Bay compared to the same period in 2023. With over half the year past already, some growth is a positive sign. This close to November on a presidential election year, one would expect the market to be looking better than it has been.

In fact, The number of homes being sold has still not recovered from the pandemic. Sales this July were 22% fewer than they were in July of 2019! As discussed previously, because the mortgage interest rates were temporarily at rock bottom, about 40% of the homeowners in California currently are “trapped in a mortgage they can’t afford to leave.” This promises to maintain downward pressure on home sales for the better part of a decade. Paradoxically, the reduced inventory is contributing to rising prices.

More homes were being sold in July, and they were being sold for greater prices. Annual increases in the median price were up 15% in entry level neighborhoods. At the Beach and on the Hill median prices didn’t reach quite as high, but were still more than 10% above July of 2023.

Monthly pricing showed the contrast between high end and entry level homes more clearly. In the Beach area the median dropped 3% from June, while on the Peninsula, there was no change in the median price. In contrast, the Harbor and Inland areas rose 6% and 5% respectively over June numbers.

Comparing the first seven months of this year to last year shows inflation continues to plague the real estate economy. Median prices rose in a range between 6% and 9% in the South Bay during the period.

Beach: Highest YTD Sales Volume Increase

Sales in the Beach cities jumped from 90 homes in June to 118 in July for a massive 31% monthly increase. This was matched by a 30% annual increase over July of 2023. Month to month statistics, as well as same month last year comparisons have shown tremendous variability this year.

The rapid fire changes precipitated by the pandemic, and subsequently by the Federal Reserve in an effort to keep the economy under control, created wild swings in the number of homes sold. At the same time the shifts in median price were less frequent and considerably less wide-ranging.

Today, looking at the year to date summaries for both, sales volume and median price, the numbers have moderated greatly. Sales volume at the Beach measured against last year has ranged from negative 27% to positive 33%. That huge range smoothed out to 6% growth in the year to date view.

Likewise, the median price, which has been a bouncing ball, declined 3% from June and increased by 11% over July of last year. Comparing the year to date from 2023 to 2024, the median settled in with a 6% increase for the longer term perspective.

Harbor: Highest YTD Median Price Growth

Monthly sales volume in the Harbor area fell 8% to a total of 316 homes sold in July compared to 342 sold in June. Annual sales moved the opposite direction, rising 17% from July of 2023 to July this year. For the first seven months of 2024 sales have fallen 1% compared to the same period last year.

Median prices had fallen 6% in June and have reclaimed that loss with a 6% growth in July. The new median, $848,500, is a 15% improvement over July of 2023. Year to date the median price is up by 9% in the Harbor area over the same seven month period in 2023.

Interestingly, every month this year has been a growth month for the year over year median price at the Harbor. The lowest increase has been 4% in March and again in June. The highest has been 18% in both February and May.

Hill: Highest Median Price In South Bay

Monthly data for the PV Peninsula came in with 73 homes sold for a 22% increase in volume over June. Annually, sales showed a 46% increase over July of 2023, a welcome change from the 24% drop in June vs June numbers. Year to date sales posted a 4% increase in volume over the same seven months in 2023.

PV registered a 12% annual increase in median price to $2,015,000 in July, so far the highest median in the South Bay for 2024. It doesn’t quite reach the $2,300,000 of May, 2023, but is one of the more impressive months in recent years. The monthly increase from June was negligible, but the timing in 2023 coincided with a downward shift in median sales prices. So, the change shows up as a 8% increase in the year to date median.

Inland: Median Price Hits $1,000,000 First Time

Sales volume for the Inland area jumped in July—up 15% month to month for a total of 142 homes sold, and up 9% since July of last year. Being past the halfway point of the year boosts the value of the the year to date statistics which come in at a mere 2% through July.

At the same time, the July median sales price for the Inland cities climbed 15% above July 2023 and hit $1,000,000 for the first time! Last year’s number was pretty run-of-the-mill so lends some import to this year’s improvement. The 2024 year to date median price calculation supports the strength shown by the monthly and annual numbers with a solid 7% increase over 2023.

Why Use Median?

A brief comment on median price and why it’s often used in real estate: Averages are used for a great many things in making comparisons, and for things that change frequently, averages do a great job. Medians, on the other hand, minimize the ‘jerky’ nature of averages and show directional movement better than a lot of up and down action.

A median is exactly the middle of a group of numbers, so that half are higher and half are lower. So the impact of a single outlier number shows less distortion on the longer term trend line of the values. In other words, it’s easier to see what your investment will likely be worth in 10 years.

Most of us don’t buy houses often enough to care about movement over the last 30 days. We’re interested in staying put for 10 years, plus or minus. The median trend will show us the most likely path.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

Photo catalina_from_wayfarers_chapel.jpg by Carl Clark

Median prices for real estate around the Los Angeles South Bay have risen over 40% since 2019, the year before the corona-virus pandemic. Comparing the median prices and sales activity for the first half of 2024 shows increases approaching 50% for the five year period in all areas across the South Bay.

Over the same time period, sales volume has plummeted by 22%, falling from 4,022 in 2019 to 3,149 in 2024. The Beach cities have been particularly hard hit with a 34% drop in the number of homes sold during the first six months of the year.

Looking at 2024 versus 2023 shows a similar pattern with median prices up nearly 10% from the first half of last year. The Beach area showed the lowest increases, coming in at 5% above the 2023 median.

Sales volume was off by 2% across the area with the only positive being the Beach at a mere 1% above 2023 numbers. As the 2024 year has progressed, the number of sales has declined in total. Simultaneously, more and more parts of the South Bay have fallen into negative growth.

As of the end of June, 2024 sales figures for all areas were negative in comparison to June of 2023. While the number of homes sold has consistently declined through the first half of the year, median prices have been equally persistent at increasing over last year. Most experts are attributing the increasing prices and decreasing sales to the shift from an ultra-low mortgage interest rate during the pandemic, to a comparatively high rate currently.

When rates were at the lowest, many homeowners took advantage of the opportunity to refinance at the incredible rates. Those folks are now in a position where they would incur a painful increase in monthly living costs if they were to move. That has resulted in about a 40% reduction in the number of homes typically available on the Multiple Listing Services (MLSs).

At the same time, the increased mortgage interest rates have pushed a significant number of potential sellers out of the market because they no longer qualify for the loan they would need to trade up to a larger or newer home. That reduced the available inventory of resale homes even further and became another contributing factor to the bidding wars among the few buyers still in the market.

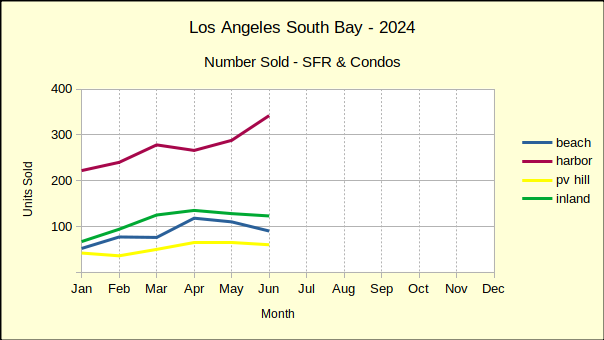

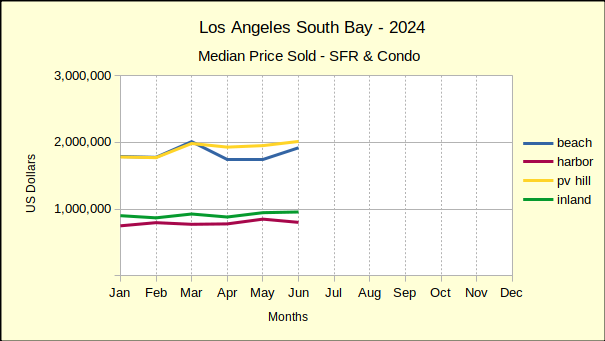

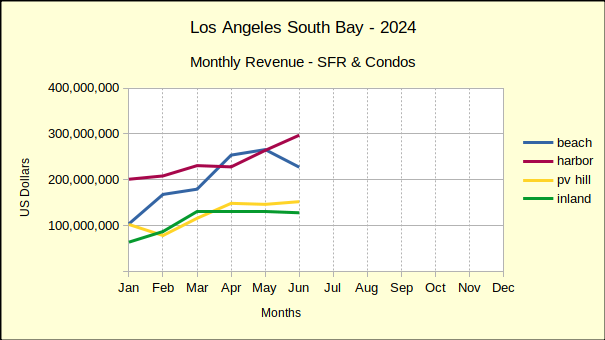

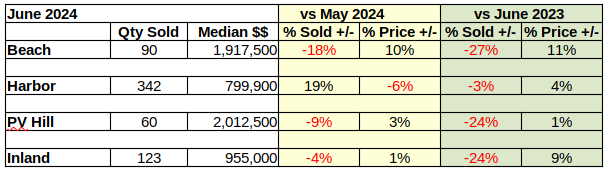

Beach: Down 18% in Sales May to June

Monthly sales volume fell from 110 units in May to 90 homes in June, for an 18% drop. Median price jumped 10% in one month to end at $1,917,500.

Year over year, the number of homes sold declined from 124 in June of last year to 90 this year for a loss of 27%. Median price for the Beach climbed 11% over the year.

Year to date for the first half of 2024 versus the first six months of 2023 shows a modest increase of 1% in sales volume along with a increase of 5% in median price.

Harbor: June Median Price Off by 6%

The Harbor area was the outlier for June. While month over month sales collapsed and pricing jumped for the other three areas, Harbor sales of 342 homes boosted sales by 19%, coming in well above the 288 homes sold in May. Meanwhile, median price went the other direction, dropping from $848K in May to $799,900 in June, for a decline of 6%.

Year over year statistics went the opposite direction, following the rest of the South Bay. Sales volume fell by 3%, dropping from 124 in 2023 to 90 in June of this year. Meanwhile the median price was up 4% for the year, rising from $772,000 last June to nearly $800,000 this year.

The first six months of 2024 brought a year to date sales drop of 4%. The median price in the same period climbed 9%.

Short term changes, as from month to month, have been unpredictable since the pandemic. Looking at the longer term, there is consistency in the declining sales volume and increasing median price. With 2024 a presidential election year, it will be interesting to see how long this direction holds.

Hill: Year Over Year Sales Fell 24%

With a reputation for wildly shifting statistics, the Palos Verdes Peninsula came in with relatively modest decline of 9% from May sales. Similarly, the increase in median price was very tempered at only 3%.

The sales volume for same month last year was anything but mild. June of 2023 reported 79 homes sold versus 60 homes in June of 2024. That’s a 24% drop in volume from last year. While a fourth of the 2023 sales disappeared, the median price eked out a 1% increase, going from $2,000,000 last June to $2,912,500 in June of 2024.

In what is becoming a familiar trend, the year to date sales volume is down 2%, and the median price for the first six months of the year is up 7%.

Inland: June 2024 Sales Drop 24% From 2023

The Inland area showed the smallest month to month change of the South Bay. The 4% drop in sales volume from 128 homes sold in May to 123 in June was minor. Likewise the 1% increase in median price from $945,000 to $955,000.

Like the Hill, the Inland area had a radical drop in sales from June of 2023 to June of 2024. Falling from 161 homes sold last June to 123 sold this June resulted in a 24% drop in transactions. Median price in the same period rose 9%, from $875,000 to $955,000.

Interestingly, there has been no statistically significant change in the sales volume for the first six months of the 2023 and 2024 years. It actually increased by three units from 669 homes sold in 2023 to 672 homes sold in the first half of 2024. For the same time periods, the median price climbed by 6%.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

South Bay median home prices are continuing to climb! May versus April showed increases as high as 9% for the month. Comparing May of this year to last May gave increases as high as 18% for the year. Year to date statistics for the first five months of the year came in with increases as high as 11%. Looking at the same five month period from five years ago shows median prices have climbed by nearly 45%.

Mortgage interest rates have roughly doubled from two years ago. The Federal Reserve Bank kept raising rates, hoping to drive inflation down. Unfortunately, it doesn’t seem to be working in the real estate world.

So far this year the interest rate increases have only modestly slowed purchases in month to month data. The number of homes sold in April was 10% higher than in March. May shows a 2% increase in the number of homes sold compared to April. Year over year sales volume shows a greater impact, with an 8% drop from May of 2023 to May this year. Most of that decline was lost this year as home sales for the year to date are up 1% from last year.

Once again looking back five years shows sales are off by 22% across the board from pre-pandemic sales volume. All while median prices are up 45%! But, there are very few homes on the market, and the shortage of inventory is driving price increases, contrary to the Fed goal of slowing inflation.

So why are there so few homes for sale today compared to 2019? And why are prices climbing in the face of mortgage interest rates that have doubled?

One possible factor: During the pandemic mortgage interest rates were at and below 3%. A significant number of existing mortgages were refinanced during the 18 months of the pandemic. Another 17% of currently existing mortgages were purchases at those rates. In summary, about 50% of the current mortgage market is now holding a note with an interest rate that is a fraction of today’s rates. There is essentially no reason for those folks to ever move.

Since about 80% of California homeowners carry a mortgage, and about half of those have an historically low interest rate, about 40% of homeowners have an incentive to stay where they are now, rather than trade up, as would be normal. Given the financial benefits, those homeowners are not likely to put their home on the market and increase the inventory thereby relieving some of the supply and demand imbalance.