Prospective buyers tend to cancel viewings on days of unexpected rain. This makes sense, as most people don’t want to be out in the rain. However, a sudden downpour may actually be an opportunity. If you’re able to tolerate the weather, rainy days are actually the best day to evaluate a home.

Water damage can be extremely expensive to repair. But how are you going to know whether or not a home is prone to water damage? Well, by looking at it in the rain, of course. After rainfall, the water is naturally going to run downhill. If you see water running towards the house, that’s a potential problem. You can also watch for signs of pooling or flooding, especially with waterfront properties, and try to spot leaks before water damage occurs. Sight isn’t the only sense you can use; mildew has a more pronounced smell in the rain. There’s also a bonus advantage — the fact that many people don’t know all this, meaning you’re going to have less competition.

When you’re trying to buy and inventory is low, it may seem inevitable that sometimes there simply isn’t anything available that suits your needs. If this happens to you, it may be that you need to expand the scope of your search. This doesn’t necessarily even mean broadening the range of acceptable homes, but rather looking for them in a different way. There are a couple different options for doing this.

The first option is looking at different media. Many homes are listed on a Multiple Listing Service (MLS) and can be easily found by your agent or on an aggregator site such as Zillow. Off-MLS sales aren’t common, but they do happen. And they’re becoming more frequent with the increasing popularity of social media sites. You can potentially find listings on sites such as Facebook or Twitter. The other is to look at old listings or listings slightly outside your price range. Often these will actually be one and the same. Overpriced homes tend to sit on the market longer because no one wants them at the current price. But that also means there will be less competition, so you may be able to offer below asking price, even in a generally competitive market. Even if the listing isn’t old yet, you can keep tabs on potentially overpriced listings and see if the price drops or it hangs around for a while.

Moving to a new area and not knowing anyone there can be an awkward situation. Some people are social butterflies and will be eager to get to know their neighbors. Others may need a little help. Here are a few suggestions to break the ice.

The most forward approach is to simply go up and knock on their door. Not everyone is going to answer the door to strangers, but you may be able to entice them. Consider bringing a gift of homemade cookies or any other dish you know and love. If you don’t want to take the situation to them, you can instead invite them over. Throwing a housewarming party is a great opportunity to invite all your new neighbors, or you can suggest a block party. For the less socially inclined, there’s an option that doesn’t require contact, but can build up familiarity over time. That is taking walks around the neighborhood and simply greeting people you happen across. If you have a dog, there’s a good chance you’ll do this anyway, but it could just be part of your exercise routine.

When buying a new home, you should not always expect that you’ll stay there forever. This is especially true for first time buyers, who often need to buy a starter home first before they can build up enough equity to buy a forever home. But sometimes it’s the right call. Keep in mind that you don’t actually have to live in your forever home forever; it just means that you could see yourself doing so. And a starter home doesn’t have to be your first home; it can be a middle stage on the way to your forever home. Neither is a binding commitment.

So when should you buy your forever home, and when should you buy a starter home? Starter homes are generally less expensive, and are something you plan to sell later. If you immediately purchase a new home after selling, you may be able to avoid capital gains tax. It’s an investment for the future. The downside is that they’re generally smaller. If you are planning to have kids soon, a smaller home may not be big enough, and moving frequently can be hard on kids. But that isn’t the only factor in determining if you should buy a forever home. Even if you could see yourself living there forever, that doesn’t mean it’s financially sound. More expensive homes will also have higher mortgage payments, taxes, and insurance fees. You may want to consider it, though, if you are able to secure a low interest rate.

Finding the right neighborhood can be difficult. You probably don’t know everything about a neighborhood you’re about to move to. Your agent may know more, but won’t know as well as you quite exactly what you’re looking for. But there are certain factors that are important for most everyone, and many of them can be researched objectively.

Everyone wants to feel safe in their community. No area is entirely without crime, but crime rates can give you a good idea of how safe you will be. The websites Neighborhood Scout and Crime Report can give some in-depth details. You should also look at transportation options and commute time. This includes not just your job, but also shopping, amenities, and schools. Not everyone is going to have the same needs in this respect, but everyone will want their specific needs met. Another important factor is the people in the community. It’s near impossible to judge them without going there, but you don’t have to be living there. You can visit community centers or even just knock on doors. Some people aren’t going to answer the door to strangers, but if that’s an important factor in providing a sense of community, that can also inform your decision.

Accessory Dwelling Units (ADUs) have been contentious for a while, but SB 9 has passed recently, ostensibly making them easier to construct in California. Unfortunately, this hasn’t panned out as well as expected, as local governments aren’t entirely on board. They’re trying to sidestep the requirements by introducing zoning ordinances that effectively, but not explicitly, ban ADUs. Zoning restrictions have always been the largest obstacle to ADUs.

What clearly isn’t much of an obstacle is popular support. Particularly in California, major cities are seeing support of over 70%, even up to 80% in San Jose. But California isn’t the only state. Nationwide support is at 69%, with the remaining 31% split between opposing and indifferent. It’s no surprise that more renters than homeowners support it, since they’re more likely to be searching for housing. But both groups show strong support — 76% of renters and 66% of homeowners.

While we can all agree that high prices and low inventory is not a recipe for a healthy real estate market, reversing the trend too quickly can cause issues as well. Prices are predicted to start declining towards the end of 2022 and throughout 2023 and 2024. This may be good for prospective homebuyers, but it’s not good for sellers who purchased relatively recently.

A sharp decline in prices could result in negative equity for some people looking to sell, meaning that they won’t be able to sell normally and may have to go into foreclosure. This is not the same type of recession that we’ve just experienced, but it’s a recession nonetheless. Fortunately, it’s not likely to result in a crash, since the continued low inventory is a positive for sellers. The market is expected to begin to stabilize in 2025, but not without steep economic losses.

In a normal year one would expect April to be the turning point for the LA real estate market. March is still cold and the children are still in school for another 10 weeks. April’s the month when the weather turns warm, the flower buds poke up, and the buyers come out to start the spring buying season. It hasn’t happened that way this year.

Prices had gone through the ceiling by the end of 2021, much of the activity stimulated by fear of escalating mortgage interest rates. Usher in 2022–January and February were typically slow and in March home sales bounced up like an indicator of business as usual. But, interest rates continued to climb and April ended with the total number of home sales down instead of up. Likewise, total sales dollars were down across the South Bay.

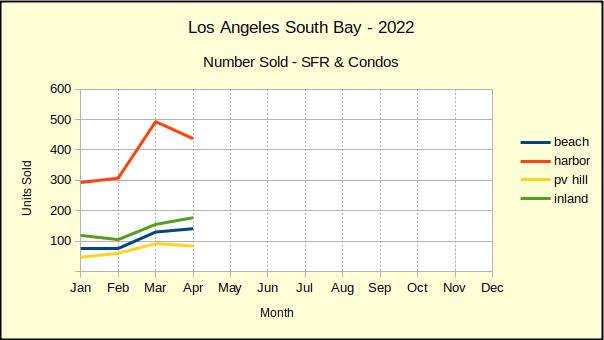

Number of Homes Sold

Judging from the charts, entry level homes in the Harbor area were clearly the center of activity for South Bay real estate. As interest rates pushed against the 5% mark, panic set in among first time buyers who had been outbid multiple times. Prices went up as high as buyers could afford, a number that shrinks amazingly fast with each tenth of a percent increase in the interest rate.

Across the South Bay, the number of homes sold in April dropped by -4% from March, which had been an increase of 59% over the prior month. As we see from the chart below, sales were uneven between the various areas.

On the entry level front, at the same time Harbor area home sales were dropping off, Inland homes gained sales. On the high end, sales on the Palos Verdes peninsula were also facing declining numbers, while Beach area sales increased.

So far declining sales counts have been modest, but a decline overall, coupled with a decline in half of the individual areas covered indicates that buyers are pulling back. Part of the resistance is a matter of simply being priced out of the market. Another important piece is the anticipation of price corrections in the near future. We have heard multiple buyers say they are watching and waiting for lower prices later this year.

At this point we’re well into the second quarter of the year and it looks as though those folks may be on track for some savings. even some of our most gung-ho pundits are beginning to see a market downturn on the horizon.

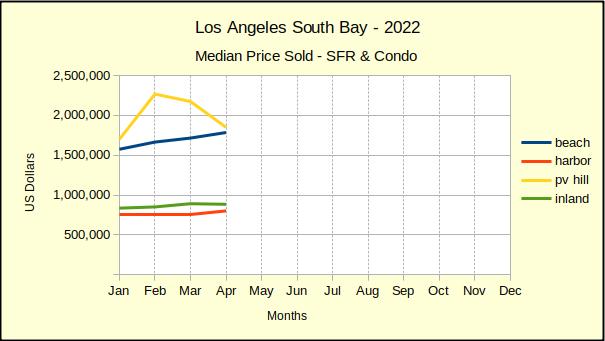

Median Price Sold

Interestingly, Harbor area prices went up at the same time the number of sales went down.The March to April price increase was a modest +6% compared to a +21% increase over April of last year. Similarly, the Beach cities had a month over month increase of +4%, while showing +19% year over year. While sales prices are still rising in those areas, the increase is a fraction of what it was last year.

Sold prices on the Hill continued to slide downwards. Because the February increase in the median price was created by the sale of new construction, and that building phase is now sold out, a downward turn in median price is expected. We anticipate that leveling off soon.

In the Inland area the median price for homes sold during April of 2022, was +12% greater than sales in April of 2021. By comparison, the median price of those sold in March of 2022 versus April of 2022 decreased by -1%. It’s a modest decrease that points to the direction of the South Bay real estate market for the balance of the year.

Area Sales Dollars

The total dollar value of home sales in the South Bay usually tracks right along with the number of units sold. The few times it differs are important times like these when the number of homes sold is dropping, and/or the sales prices are dropping. Today, of the four areas we track, PV Hill has a declining number of sales, both in comparison to last year and in comparison to last month. As we noted above, the area also is declining in total dollars compared to last year and last month.

As we discussed in last month’s issue, some of the reason for the drop is found in new construction homes that sold at a much higher price than the typical Palos Verdes resale home. The rest of it can be found in longer days on market waiting for a buyer, and in price reductions.

At the opposite end of the spectrum, the Beach cities showed gains last month for both number of units sold and for the total sales value of those homes. The only decline this month for the Beach was in number sold compared to April of last year. Sales this April were off by -21%.

The Harbor area still trended upward in dollar value, both month over month and year over year. But, the number of units sold was down for both time measurements. The price competition was very stiff in what is generally an entry level market. During the past couple years, bidding wars and over-asking sales prices have kept the dollars high. The April numbers show that changing rapidly.

Total dollar sales for the Inland community increased 15% month over month. That was the highest growth of all four areas. Scanning those individual transactions showed an odd pattern. Sales in the price range from about $325K up to about $750K were a familiar mix of some under asking price, some at asking and some above asking. The degree of variance was about what one would expect. Unexpectedly, for sales over $750K, nearly every property sold above asking price, and in many cases well above asking.

We found no clear explanation for why this phenomena occurred. There is a suspicion that buyers who were priced out of Beach properties may have shifted their bidding wars into the increasingly popular parts of west Torrance. This theory is supported by the distribution of sales among the various neighborhoods.

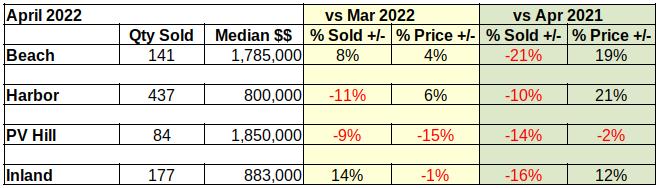

In Summary

In the table below are the core statistics comparing April to March of this year, and comparing April of this year to April of 2021. The prevalence of negative numbers is convincing evidence that high prices and high interest rates are pushing the South Bay real estate market into a recession.

Notable Properties

One of the more interesting properties sold in April is a four bedroom, five bathroom home located in west Torrance. The home was purchased by the seller as their family home in 1990 for just above $360K. The children grew up and the parents remodeled in 2022 and sold the house.

As would be expected in a good neighborhood with a contemporary remodel, the home sold for over the asking price of $2.7M. The final selling price was slightly over $3M. and just happened to be almost exactly $360K over the asking price.

In the 32 years that family owned the home it appreciated at an average rate in excess of $84K per year. It’s the classic “American Dream.”

With home prices on the rise, young adults are experiencing struggles paying for a home with just their own income. As a result, cohabiting is becoming more common, in which unmarried partners –or possibly just friends — choose to pool their money and purchase a home together. Some may be concerned that this can cause some financial headaches. But really, all you need to do is make sure you know your cohabiting partners well.

Marriage certainly confers some legal and financial benefits. As far as purchasing a house, though, the financial side of things doesn’t actually care whether you’re married or not. Relationship status is not a factor in mortgage rates, as every co-purchaser’s financial history is considered separately, whether they are married or not. However, this also means that if you don’t really know a partner’s financial history too well, you may be in for an unwelcome surprise. It’s also important to note that even after successfully purchasing the home, conflicts between co-owners can result in situations not too dissimilar to divorce proceedings, even if you aren’t married.

Fannie Mae was sued back in 2016 under allegations of fair housing violations, and the organization decided to settle in February of this year. The settlement amount was $53 million. Fannie Mae had acquired a large number of properties in the wake of the subprime mortgage crisis, and thus became responsible for their maintenance until they were sold. But fair housing organizations started to notice a trend: only the ones in predominantly white neighborhoods were being adequately maintained.

The settlement agreement was the first to determine that foreclosed properties, like the ones Fannie Mae holds, are also subject to fair housing laws. This was not officially determined prior. Also, it’s possible that they were in worse conditions to begin with, but that doesn’t absolve Fannie Mae of their responsibilities. Their argument was that their intentions were not discriminatory. Perhaps they simply were not able to maintain the homes as well since they were in worse shape. But they were unable to reject the claim that regardless of their intentions, the impact was obvious. This is what led to Fannie Mae needing to settle.

With mortgage rates on the rise, more and more buyers are struggling to obtain loans. Given this, an infrequently-used financing option is starting to make a comeback. Seller financing is an process in which the seller of a property offers to carry the mortgage, and the buyer will then owe the seller rather than a lender. This doesn’t have the same stringent requirements that mortgage loan approval has, so it’s much more accessible to buyers.

Seller financing tends to be attractive to buyers. Not only is it more accessible, but the interest rate is usually lower. It also doesn’t incur any fees such as loan origination fees. But why would a seller want to do this? Well, there are a couple reasons. Firstly, because seller financing is so attractive to buyers, it can improve the property’s marketability. There’s an additional benefit, though. It allows the seller to defer part of the taxes on sale profits. The seller only pays taxes on the principal as it is received. At the time of sale, they pay taxes on only the amount the buyer paid. This can include the down payment and any partial loans the buyer received.

The California Housing Finance Agency (CalHFA) has introduced a new loan program called the Forgivable Equity Builder Loan. It comes with some heavy restrictions — only first-time homebuyers are eligible, and it only covers up to 10% of the purchase price. This is because it’s a supplementary loan that can only be taken out in combination with a CalFHA first mortgage. The good news is that this loan has an interest rate of zero percent, and is also forgivable if you occupy the residence continually for five years. However, standard interest rates apply to the CalFHA first mortgage.

The program also requires borrowers to complete a course on homebuyer education and obtain a certificate of completion. This course does require a one-time fee of $99 if taken online, or a variable-rate fee if taken in person. You must also occupy the new home as your primary residence, as well as meet income requirements. The property must be a single-family residence or manufactured home. This can include condominiums if they meet the requirements for the CalFHA first mortgage, or ADUs in some cases.

You can find advice for prospective home buyers all over the internet — including, of course, in our articles. But who knows better than the buyers themselves what they’re having trouble with? For over half of survey respondents, 56% to be exact, the biggest problem is finding the right property. This is probably partially the current market, with very low inventory, and partially buyers not knowing what or where they can afford to buy.

This isn’t one of the categories buyers mention, though. For nearly a third of respondents, the most difficult part is understanding the process and paperwork involved. 20% cite primarily monetary issues, either with saving for a down payment or getting a loan. Comparatively few, only 7%, believe that COVID-19 was a significant complication. Meanwhile, 18% of respondents don’t think the process of buying a home is difficult at all.

Many homebuyers aren’t sure what to do when a home they want to make an offer on is in pending status. If you really want the home, the best thing to do is to make a backup offer. If you submit an offer normally, the seller is still contractually obligated to honor the original offer if it doesn’t fall through, even if your offer is better. But don’t get your hopes up — most pending sales carry through to completion, since it merely means that the seller has accepted an offer.

What does it mean if the sale does fall through, though? In certain situations, this could be a red flag, but in others, the problem lies elsewhere. Sometimes the home inspection reveals issues that the buyer (and possibly the seller) wasn’t aware of, which could change your mind as well. The bank could decide to cancel an unapproved short sale, which could entail more legal complications than you want to deal with. Other times, the problem was with the buyer, perhaps not being able to acquire a loan. If the issue is with contingencies that have yet to be met, the home may be listed as contingent rather than pending.

Home improvements have gotten more popular recently, as many people have switched to work-from-home and are spending more time there. Usually, these improvements are primarily made for the owner, rather than for a prospective buyer. These features would also be high in demand if you are planning to sell your home, but there are a few things that can actually increase the value of your home by much more than you spend.

You may be able to improve your energy efficiency by upgrading your windows, which is certainly value over time for a homeowner, but it’s also increased value for a home seller. Energy efficiency is a significant draw for buyers, and will improve the value by more than its cost, even if you aren’t reaping the rewards of it yourself. Kitchen remodels almost always pay for themselves. Homeowners spend a lot of time in their kitchen, and they want it to suit their needs. Figure out what people are looking for in a kitchen right now, and make it happen. A rather expensive upgrade is a stone veneer. You won’t recoup the entire cost if you sell immediately, but you’ll get back most of it. This is one that you’ll want to have accrue value over time.

The primary purpose of refinancing is in order to spend less money in the long term. It may seem like this is a good idea whenever rates drop even the slightest amount. However, it’s important to remember that you are technically originating a loan when you refinance, and doing so incurs the same fees. The upfront costs are what deter repeated refinancing.

Most of the fees are a few hundred dollars — unless otherwise specified, you can estimate they will be about that much. Since you are applying for a mortgage loan when you refinance, this requires both a mortgage application fee and a loan origination fee. The numbers vary, but typically, the the loan origination fee is 1% of the loan’s value. You will also need your home to be re-appraised, as lenders want to know the value of your home before approving a loan, which will require an appraisal fee. It’s also possible that your lender will require a title search, and you may need new title insurance, both of which incur fees. Title insurance, if required, could be $1000 or more.

The majority of homebuyers choose fixed-rate mortgages (FRMs) over adjustable-rate-mortgages (ARMs) in order to not have to deal with the uncertainty of changing interest rates. However, there’s very little uncertainty right now — interest rates are going up. This does include both FRMs and ARMs, but ARMs tend to have lower starting rates — a 5-year ARM was at 4.28% in mid-April. Buyers are predicting that even with an adjustable rate, their rate is not likely to surpass the 30-year fixed rate of 5.37% as of the end of April.

ARMs aren’t exactly popular, though. Even with their share doubling in the past three months, that’s still only 9% of mortgages. About as large a share of potential buyers are instead choosing to simply wait for a better time, with mortgage applications dropping by 8% and refinance applications dropping by 9%. Refinance applications are also drastically lower than the same time last year, having dropped a whopping 71%. New mortgage applications also dropped since last year, by a much more modest but still significant 17%.

The usual effect of rising interest rates is a decrease in demand, as buyers would rather wait to lock in a lower rate. Decreased demand should then translate to lower prices, since sellers want to encourage buyers. Not so in the San Francisco Bay Area right now. Prices are still going up, and demand didn’t really go down all that much.

The culprit? A couple of factors. Most significantly, inventory is extremely low in the Bay Area. Buyers are encouraged to take opportunities where they can, since they don’t come up often. That often means paying less-than-ideal prices. Secondly, the Bay Area is generally a high-income area and already has high prices. Even with rising prices, most people able to purchase there aren’t going to be suddenly priced out. Those looking for a median-income or lower household aren’t looking in that area to begin with.

We know that the wildly high post-lockdown demand was in large part driven by fear of missing out, or FOMO. People definitely took notice of the low interest rates and decided to take advantage of them. Interest rates are no longer low, and home purchasing demand has slowed. However, home renovations are still in high demand for just a bit longer. Renovating is not as expensive as buying, so homeowners with FOMO who could not afford to buy instead sought to remodel their current homes to better suit their needs.

In turn, though, home renovation costs have also increased rapidly in response to demand. By the last quarter of 2021, the year-over-year change in home remodeling costs had risen to 9.4%, about 2.5 times the expected 3.8% increase. Current projections have the Q3 2022 increase at an incredible 19.7%. But just like with rising home prices, increasing home remodeling costs will begin to price out even those affected by FOMO. Q3 is predicted to be the peak, with the prices starting to slow again by Q4 2022.