Most buyers are aware that homeownership has some extra costs associated with it. You can’t just pay the purchase price and be done. But it seems the vast majority aren’t prepared for just how high those costs can be. A whopping 90% of homebuyers in the past three years underestimated the hidden costs of homeownership, and 73% regretted some aspect of their purchase.

For a third of them, the culprit was property taxes. Even if you have purchased before, buying a new home in a high-priced market will probably drastically change your property tax values. A quarter or slightly over a quarter of respondents didn’t think roof work, renovations, or utilities would be so expensive. Annual expenses among respondents average $17,459 on top of mortgage payments. In hindsight, 57% of buyers know what they would have done differently. Among this subgroup, 42% would have purchased a home that didn’t require quite so much maintenance. It may cost more up front, but the annual costs could be significantly lower. 33% think they just needed to negotiate a lower price, and 29% would have gone for a lower-priced home to begin with. 27% believe it was simply the wrong time to buy, and they would have waited for a better deal.

The California Housing Finance Agency (CalHFA) recently launched the Dream For All Shared Appreciation Loan, a secondary loan to be used in conjunction with CalHFA’s Dream For All Conventional first mortgage. This secondary loan carries its own set of requirements, which may or may not differ from the initial Dream For All Conventional first mortgage. The requirements of the secondary loan are provided here, but you should consult with CalHFA to be sure that you meet all requirements. The requirements are provided for two categories, both for the borrower and for the property.

The borrower must be a first-time homebuyer, which CalHFA defines as not having owned and occupied a home in the past three years. The borrower must also occupy the property as their primary residence and meet income limits for the program. In addition, the borrower, or at least one of the co-borrowers if there is more than one, for any CalHFA first-time homebuyer loan must take a CalHFA approved Homebuyer Education and Counseling course. This course does have a fee, which varies by method and agency, and can be done online or in-person. The Dream For All program also has its own additional course. Fortunately, this course is free, but it is only accessible online.

The property requirements are simple for single-family residences and manufactured homes, which are both allowed, but may be more complex for other types of properties. Condominiums must also meet the guidelines for whichever initial mortgage you choose. Guest houses, granny units, and in-law quarters may be eligible, but would not be eligible in addition to the main residence, since the property must be only one unit.

Wrap-around mortgages are not very common, but it’s still a good concept to know in case you find it difficult to get a more traditional mortgage loan. A sale with a wrap-around mortgage has two important components distinguishing it from a regular sale: First, the seller retains the current mortgage on the property being sold. This differs from standard sales in which the seller normally pays off the remaining mortgage as part of the sale process. Second, the loan is not issued by a lender but rather by the seller. In this way, the seller is most likely planning to pay their mortgage using the money gained from payments the buyer makes to the seller on their new mortgage.

Wrap-around mortgages have both advantages and disadvantages. The primary reason to get a wrap-around mortgage is that they don’t have any standardized qualification requirements. This mostly benefits the buyer, but can also be useful to the seller if they’re having difficulty finding buyers. The primary drawback is that the buyer and seller must write up the contract themselves, since there is no lender involved. That means both parties need to be legally and financially savvy. It’s also impossible to wrap around a mortgage that doesn’t exist, so the seller needs to have a mortgage. There are also cons specific to the seller and buyer. The seller in this instance incurs the same financial risk that a lender would normally. The buyer is very likely paying a higher interest rate, since the arrangement is not worth the risk to the seller unless they are profiting.

A common reason to purchase a new home is needing more space because you are expecting kids. But just having more space isn’t going to prepare your home for all the trouble a baby can get into. By the time your kid is able to crawl, you’ll want to have finished baby-proofing your home.

Some things are probably pretty obvious, like using baby gates, locking drawers, keeping hazardous substances away, and covering up sharp edges. But some safety precautions are things you may not think about. While it’s true that babies often like soft and fluffy blankets, leaving them around loose can be a suffocation risk. When you’re in the kitchen, you’re probably used to having pot and pan handles turned towards you for ease of access. But once your kid can walk, there’s a good chance they can reach up there. Make sure to turn the handles inward. You should also acquire a latch for the oven. Bathrooms can be dangerous for both kids and adults, so you may already have taken precautions such as non-slip mats for your bathroom. But if not, make sure to get some. You may also want to get soft covers for the knobs and spouts.

Some of the questions on a mortgage application may seem unnecessary, but they’re all there for a reason. Certain omissions can lower your interest rate and make your offer seem more appealing. But even if you haven’t done anything wrong — especially if you haven’t done anything wrong — you should always disclose all relevant information.

Money changes hands all the time, and the transfer doesn’t always leave a paper trail. But lenders will still find it odd for you to suddenly have additional money or fewer debts. It’s perfectly legal to ask a friend or family member for some cash to help you buy a home or pay off a debt. That money came from somewhere, though, and if you don’t list it, your lender could assume you are hiding something and deny your application.

A common lie that seems more innocuous but can actually have even more drastic consequences is stating that you plan to live in the home when you actually don’t. People do this because interest rate is lower on loans for primary residences, and they figure it’s fine because of course they can always change their mind. However, this is actually a crime. It’s considered a form of mortgage fraud.

Project Barley serves excellent Food (Gourmet Pizza, gluten free/vegan options, wings, sandwiches, salads), wine, and award winning beer. Food served till 8:30pm. No reservations so arrive early to get a table. 2308 E Pacific Coast Hwy, Lomita, CA 90717 https://projectbarley.com/

FRIDAY, MAR. 24TH AT OUR LIVESTREAM SHOW THIS FRIDAY!!!!

DYLANFEST SUPER EARLY BIRD TICKETS ON SALE NOW-TIL APRIL 1st!

Hello everyone!

Hope all is well!

Lots of other Great gigs coming up….Hope to see you!

Celebrate Andy’s Birthday at our Livestream, Friday, March 24th. Just RSVP to this email to reserve your spot!

We will also be up in Auburn, CA the last weekend of March and Dallas, TX in April…Go to www.andyandrenee.com for more info.

Exciting news….Super Early Bird Dylanfest 33 tickets are ON SALE NOW! Save $10 off the price at the door til April 1st! Go to https://andyandrenee.com/tickets-tips-merch to get yours now!

Every WED @ 8:30PM — 11:30PM Fairmont Century Plaza, 2025 Avenue of the Stars, Los Angeles, CA

Andy & Renee-Livestream #206

Celebrate Andy’s Birthday a day early!!

Friday, Mar. 24th 6pm PST

Home of Andy Hill 17411 Delia Ave., Torrance, CA 90277

Watch live, or anytime at https://youtube.com/live/BpWWfg1d_Hc?feature=share. Come watch the show in person! LIMITED SEATING, so RSVP to reneesafier@hotmail.com ASAP. The Livestream shows are free to watch, but the option to contribute is there for those who are in a position to do so. You can see our song list to make requests and contribute at https://andyandrenee.com/tickets-tips-merch, PayPal (paypal.me/andyandrenee) or Venmo, (www.venmo.com/Renee-Safier). A portion of the proceeds will go to the Los Angeles Midnight Mission. We are sustained by the generosity and support of the fans who love the music, and who donate as they are able. If you use funds from your bank vs. your credit card, we aren’t charged a service fee, but either way, we appreciate your support!

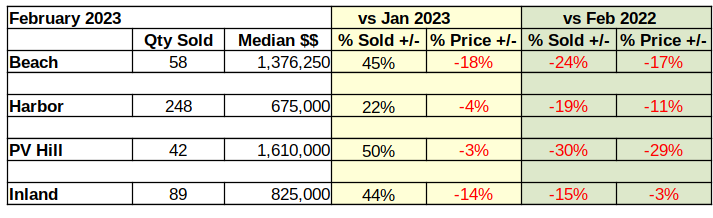

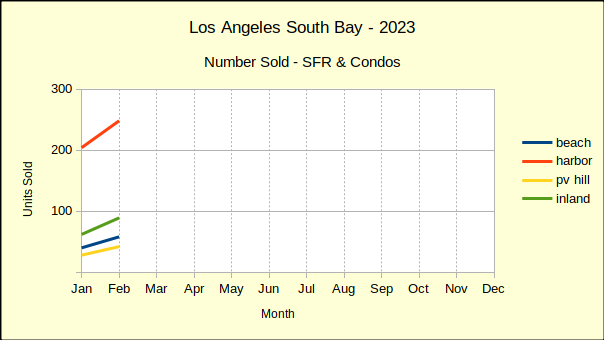

Last year ended with sales volume off, median prices coming down and revenue dropping fast. January showed little change. February of this year shows sales volume up from January by as much as 50%. The reason why is obvious–the median price is simultaneously dropping by percentages as high as 18%.

Comparing February activity to February a year ago shows significant declines in both sales volume and in median price. At that point in 2022 the market was just beginning to dip a toe in the recessionary waters. Now we’re wading into it.

The first week of March Fed Chairman Jerome Powell told Congress, “…the ultimate level of interest rates is likely to be higher than previously anticipated.” Powell’s pointed remark clearly tells us the most recent pause in interest rate hikes is momentary. The lowest local mortgage rates we could find at the time was 6.75%. As such, we anticipate rates in excess of 7% by summer.

February Sales Volume Climbs

About the second week of January mortgage lenders began loosening the interest rates in anticipation of a relaxation by the Federal Reserve. For the most part, local rates stayed below 6% until late in February when the Fed began dropping hints that inflation was still raging.

After a “soft” January, sellers in the market were dropping prices and buyers responding positively by making offers. Now that mortgage rates have resumed climbing, sellers will have to drop prices some more to remain attractive to buyers.

With only two months behind us this year, there are indications lenders will “see-saw” the rates throughout the year. Already this year we have seen retail mortgage rates moving up and moving down without influence from the Fed. It seems to be an effort to induce buyers to accept high interest rates based on the theory they were higher last week so this temporary reduction is a good deal.

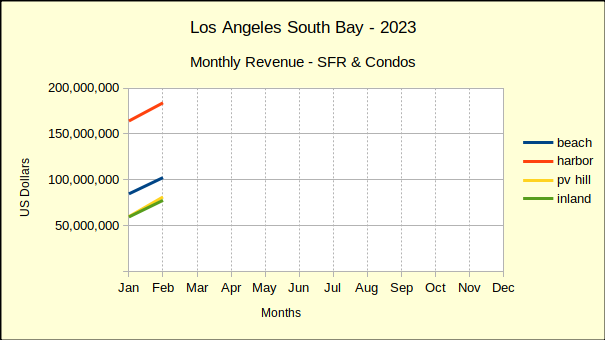

RevenueClimbs From January Depth

On a month-to-month basis, revenue across the South Bay is up 21% from January of this year. Don’t get excited—it’s only one month. January was one of the lowest performing months we’ve seen recently.

On a year-over-year basis, revenue is down 34% from last February! January was 38% lower than January of 2022. Year to date through February, revenue in the South Bay is down 36% and is expected to continue falling.

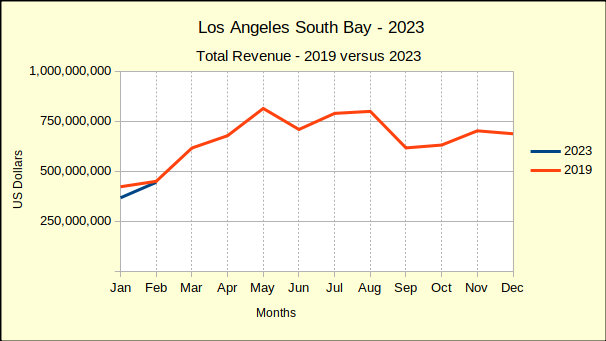

One of the more important statistics to note is how 2023 activity compares to 2019, which was the most recent “normal” year of real estate business. Across the South Bay real estate revenue for the first two months of 2023 is 7% below the same period in 2019. Restated, the South Bay has already lost over four years of gain in real estate revenue.

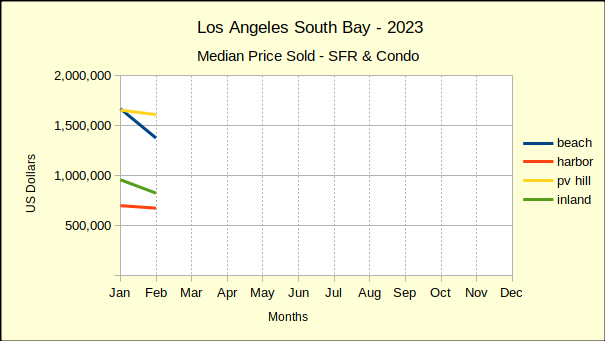

Median Price Slips, Volume Rises

More units of housing were sold in February than January, and the median price was lower in February. The Beach Cities saw a drop of 18% from January while the PV Hill held the decline to 3%. The Harbor area fell 4% and the Inland area dropped 14%.

Comparing February of this year to February of 2022 brought a harsher focus to the picture. All four areas have fallen from last years median price. The Beach is down 17%, the Harbor down 11%, the Hill is off 29% and the Inland cities down just 3%.

2023 Versus 2019 Shows a Sinking Market

The summary numbers comparing the first two months of 2023 to the most recent “normal” year of 2019 are not encouraging. Overall, sales revenue has fallen 7% below revenue figures for the same period in 2019. The Harbor area has fared the best, showing a 9% increase in revenue over January and February activity in 2019. Of course, that was four years ago and classic inflation would give that type of gain. It’s clear the “inflation on steriods” we’ve been experiencing is gone from the real estate industry.

The Beach cities provide an excellent indication of where the real estate economy is going. The first two months of revenue for 2023 is down 32%. Palos Verdes is down 2%, while the Inland area is up be a mere 1%. After four years of pandemic, recession, inflation and Federal Reserve manipulation the real estate market is tanking.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

If you’re looking to earn some extra income over the summer, consider renting out your home as a vacation rental. It’s not too early to start thinking about it, especially if you want to buy a vacation rental house. Spring is the top of the real estate market and there will usually be more options available to buy. Even if you want to rent out your current house, there’s some prep work to be done first.

When marketing a short-term rental, think of it as a hotel. That’s where most people stay while on vacation, so you need to make sure it’s attractive to people who would otherwise simply book a hotel room. Advertise the amenities you have and the benefits of staying there over a hotel room. Price probably isn’t going to be one of them, but it’s still definitely something you need to think about. Pricing vacation rentals is difficult because they probably won’t be earning income all throughout the year, especially if you live there yourself most of the time. This means you may need to charge more to cover your monthly costs and retain a profit, unless you don’t have a mortgage. But you don’t want to charge so much that no one rents from you.

The other thing to consider is protecting yourself and maintaining your property. With the property changing hands between multiple tenants, you never know what could happen unless you keep an eye on it, which may be difficult if you are also on vacation yourself. Talk to property management companies to see what services they offer and for how much. You’ll want your home cleaned in between tenants, which may or may not require hiring cleaners separately from a property manager. Also take a look to see if you want additional liability insurance.

Discrimination — sometimes legal, sometimes not — has kept Black homeownership rates below white homeownership rates for decades. Even now, Black homeownership rates are nearly 20 percentage points lower than the overall homeownership rate in California, at 35.6% versus 55% in 2021. Fortunately, it’s going up, albeit slowly. Between 2016 and 2021, the rate increased 2.5% percentage points.

Riverside County experienced the largest increase, going from 44% to 53% across the five years. However, the rate stayed the same or even decreased in some counties, including San Francisco where it’s remained just 22% and Santa Clara County which saw a drop from 30% to 25%. Even with the Black population in California only being about 6%, compared to the national value of 13.6%, it still accounts for over 2 million people. It certainly is difficult to find affordable non-rental housing for that many people, but there’s no reason it should be more difficult to house Black people than white people.

Real estate articles will frequently talk about first-time buyers, since they are a significant proportion of buyers overall. Less discussed are first-time sellers. It may be time to change that, since it seems like they could use some advice from experts. In the past two years, 84% of first-time sellers wished they did something differently during the sale process. The four things first-time sellers most regret are their decisions regarding pricing, online presence, timing, and repairs.

The most frequent comment was that they should have priced their home higher. Of course, that depends on the market. That may have been true when they sold, but don’t necessarily take that to heart. It’s also possible to list too high, which may be a more common regret this upcoming spring. Regardless of the list price, though, 90% of first-time sellers believe they could have done something to get a higher price. For 39% of them, this may be better listing photos. Virtual curb appeal is important nowadays when many people are looking online for their purchases. Since listings with virtual tours get 69% more views, this could boost your chances by quite a bit, and 25% of people agree a virtual tour would have helped. According to Zillow, the optimal time to sell is the second half of April. Not everyone has the flexibility to do this, but 25% still wish they listed at different time. 36% also didn’t have a good idea of how long it would take to sell. Even though 66% of first-time sellers completed at least two home improvements before selling, 25% believe a bigger investment in repairs or improvements would have increased the sale price.

California has been experiencing a significant exodus of its residents, many of them moving to arguably quite dissimilar states, such as Florida, Texas, and North Carolina. The most salient difference between California and these states is political leanings; however, that’s not the reason people are leaving. The real reason is that California is simply too expensive. When asked where they would move if money were no object, the greatest percentage of people named California, at 27% of respondents.

This is definitely not where most people did move in 2022, but the responses of those people regarding their reasons for moving corroborate this idea. The two biggest reasons were better quality of life for 24% of respondents and lower cost of living or home prices for 23% of respondents. Note that respondents could pick multiple options, so they do not add up to 100%. Within quality of life, affordability was rated as the second most important factor, only below a safe neighborhood.

Along with California, New York and Illinois were also among the states that the greatest number of people left. The fact that these three states contain the three most populous cities in the country is probably not a coincidence. But this is not because people don’t like big cities. 40% of people would prefer to move to a city if they could, but many can’t afford it.

Spring is the hottest season in the real estate market. If your home is in need of some improvements before selling, now is the right time. Or, even if you aren’t selling, some seasonal DIY projects can bring something new to your own enjoyment of your home.

Something that will always help sell your home is a fresh coat of paint. And if you have the time, it doesn’t require contractors. Painting is relatively easy and only takes a couple hours to learn online even if you’ve never done it before. Or maybe you aren’t selling, and simply want a new look for the spring season. In that case, pastel greens, blues, and creams are good spring colors. If you have a garden, a project that will only take up a weekend of your time is building DIY planters. Many planters are made of wood, but stone planters are more durable. Building a stone planter just requires four slabs of stone such as granite or marble, one to two tubes of stone adhesive, a ruler, and cement tape. All you need to do is make sure the slabs are positioned correctly with the aid of a ruler, apply adhesive to the inside edges, and use cement tape to hold it together while the adhesive dries. Something more on the fun than practical side is bird seed rings, which are a treat for birds, and for yourself if you enjoy feeding them. They are made by combining gelatin, corn syrup, and flour into a paste, mixing that with a bag of bird seed, then using a donut pan to mold them into a ring shape. You can then hang them outside where they will attract birds.

WalletHub, a personal finance website, releases its report on the Happiest Cities in America each year. 182 of the largest cities are ranked on 30 different metrics, condensed into three categories — emotional & physical well being, income & employment, and community & environment. Taking the number one spot with a total score of 76.10 out of 100 is Fremont, California, which has now been number one for its third consecutive year. Not only that, Fremont ranks highest in two of the three major categories, both emotional & physical well being and community & environment. Fremont’s rank in income & employment is 34.

California’s San Francisco Bay Area seems to be doing quite well for itself. Fremont itself is in this region, and so are the number 2 and number 5 ranked cities on the list, San Jose and San Francisco. These three cities and Oakland are the four largest cities in the Bay Area. Oakland is also in the top 15, sitting at number 13. The other 2 cities in the top 5 aren’t in California, though. These are Madison, WI at number 3 and Overland Park, KS at number 4. As far as best in category, we already know Fremont takes the top spot in two of them. But the top spot for income & employment belongs to Burlington, VT, which is also number 10 overall. The least happy city overall is Detroit, MI, but at least it’s not the absolute bottom in any category.

There’s plenty of advice out there telling you that negotiating your mortgage is important and that you should get multiple opinions. However, unless you know what you’re looking for, you’re probably not actually getting the best deal. On the surface, it may look like the lowest rate you can find, but it likely isn’t. You’ll often need to dig and ask the right questions.

So what are the right questions? Ultimately, you want to know the exact breakdown of the estimate. As you probably already know, interest rates aren’t based on just one factor. You may not realize that some of these factors are actually negotiable, or you may even have more information about it than the lender and be able to correct the estimate. Ask if the estimate includes any discount points. Discount points are an up-front payment that lenders aren’t going to tell you actually lowers your interest rate, rather than being just a standard fee. Discount points are negotiable, but lenders won’t mention that unless you bring it up. The estimate that a lender provides may or may not also include closing costs. Discount points and lender fees are part of closing costs, but a significant portion of them are not actually under the lender’s control. Lenders frequently underestimate escrow fees, so when it comes time for you to pay the closing costs, your fee may be higher than the estimate even if the rate is locked. Make sure to only compare costs the lender can control.

Most agents are probably familiar with a pocket listing, but if you aren’t an agent, you may not know what that is. Even if you do know what it is, you may not realize why they’re a problem. A pocket listing is a listing that is temporarily exclusive, before a delayed release into the open market. At first glance, this can seem like a win-win-win situation. Sellers don’t need to do as much preparation and their agent can vet the buyers for them. Buyers don’t have to deal with nearly as much competition. The agent gets double the commission by representing both sides.

However, it’s not all upside. There are also plenty of cons to pocket listings, and they may outweigh the benefits. A big problem is that pocket listings simultaneously skew the market while not being governed by the market. Not listing the properties on the market reduces inventory values, which skews both competition and prices upward, significantly hurting buyers overall. You may think this benefits the seller, but it actually doesn’t. Because the pocket listing isn’t governed by this upwardly skewed market, the buyer of a pocket listing is likely to pay significantly less than the distorted high prices. In fact, because of the total lack of competition, they’re likely to pay less than the actual market value. For the agent, being a dual agent is a lot of work and stress, and it’s only increased by attempting to make it a pocket listing. In the event the seller suggests a pocket listing, this isn’t as much of an issue. But an agent truly can’t push for a pocket listing without breaching their fiduciary duties to the seller, which include taking reasonable steps to locate a buyer. Even if it’s on the seller’s suggestion, there will always be a conflict of interest when representing both sides that the agent will need to delicately navigate.

When less fraud is being reported, that tends to mean consumers get complacent and aren’t being vigilant, thinking that fraud is less common. But what it actually entails is that fraudsters are getting smarter. According to the Federal Trade Commission (FTC), the total value of fraud reported by consumers in 2022 was $8.8 billion, with 2.4 million fraud reports. This dollar value is an increase of 30% from 2021, despite fewer reports. In 2021, there were 2.9 million reports totaling $6.1 billion.

The increasing online presence is definitely contributing to the problem. The greatest amount of losses by method of contact is social media, accounting for $1.2 billion. The second most reported method of scam is an online shopping scam. Older methods of fraudulent activity are still alive and well, though. Imposter scams are the most common method, and phone calls have the highest per-person reported losses at a median of $1400. Investment scams are also getting increasingly popular, with losses more than doubling from $1.8 billion in 2021 to $3.8 billion in 2022.

If you’ve just unexpectedly come into some extra cash, you may be tempted to immediately put it towards a home so you can start accruing equity as soon as possible. Unfortunately, this isn’t always possible. Most, but not all, lenders require at least a portion of your down payment to come from what they call seasoned funds. Typically, seasoned funds are those that have been in your possession at least 60 days. Lenders will require a paper trail to confirm how and when you acquired the funds used for your down payment.

Usually, at least half of your down payment must come from seasoned funds. However, rules vary by lender, both with the percentage of funds that must be seasoned and the length of “seasoning.” Fortunately, this mainly applies to windfall gains, and there are other methods of acquiring money that don’t need them to be seasoned. If the money was acquired via borrowing from your savings or retirement account, this is generally allowed, though you should discuss the tax implications of this with an accountant. Some lenders will allow gifts to be used for a down payment. Some don’t allow it at all, and those that do will probably require a written confirmation from the person gifting the money.

Even with all its ups and downs, real estate has always been one of the safest investments. But as with any type of investment, you need to know your stuff to get the best deal. That means being familiar with some of the terms used in investment. Three important ones are hard money loan, net operating income or NOI, and debt-to-income ratio or DTI.

A hard money loan is any loan backed by real property. While this is the actual definition, there’s another aspect of most hard money loans that is what investors are most interested in. Usually, a hard money loan is an immediate, short term loan used for the purchase of commercial or investment property. However, they are typically offered only by private lenders, and often have a higher interest rate due to the shorter term length.

NOI is the net amount of revenue you gain from your investment, after deducting related expenses. These expenses could include such things as mortgage payments, property taxes, insurance, and property management fees. At first, NOI may appear to be the same as return on investment or ROI. In common parlance, the terms may be synonymous. However, in investment real estate, ROI actually refers to the length of time it takes to get positive NOI.

DTI is a term you need to know if you are getting any loan, not only an investment loan. Fortunately, the name doesn’t hide what it is. It is simply the ratio of your total debt to your monthly gross income. Lenders use DTI to determine the loan’s interest rate. A lower DTI will give you a better rate on mortgage loans.

No matter which region of California you’re looking at, things initially appear pretty dire for home sales. From December 2022 to January 2023, it’s down in every single major area. The decrease is smallest in the Inland Empire at 15.4% and highest in the San Francisco Bay Area, where sales dropped 38.1%. They also dropped significantly in the Central Valley, by 30.8%. Even in the Far North, where prices actually increased by 4.9%, home sales are down 18.4%. Most regions experienced a decrease of approximately 19%.

However, that rate is not seasonally adjusted. Winter is the slowest season in terms of home sales, so it makes sense that sales would be down. One rate that is seasonally adjusted is the statewide single-family residence (SFR) data. With sales being down in every region, you’d expect sales to be down statewide, since those regions do encompass the entire state. But with seasonal adjustment, we discover that the month-to-month SFR sales actually increased ever so slightly, by 0.4%. In fact, this was the second straight month of seasonally adjusted increase in SFR home sales. It’s hard to say just yet whether this is an overall increase in market confidence, or simply preparation for the often-hot spring season, but in either case, expect sales to increase. If spring sees not only an increase — which is expected regardless — but a seasonally adjusted increase, then we’ll know that market confidence has improved.

This coming Tuesday night will feature some of LA’s best songwriters! Ted Russell Kamp, Abby Posner, Mary Scholz and me~

This coming Tuesday night will feature some of LA’s best songwriters! Ted Russell Kamp, Abby Posner, Mary Scholz and me~