Two more bills aimed at increasing multi-family construction go into effect July 1, 2023 after Governor Newsom signed them into law in September. These are AB 2011, called the Affordable Housing and High Road Jobs Act of 2022, and SB 6, the Middle Class Housing Act of 2022. Both laws sunset nine and a half years later, on January 1, 2033.

AB 2011 adds a secondary review pathway for some multi-family construction projects. If the project meets affordability standards and site criteria, the review will not take into account conditional use permits or environmental impact reports. The site must be primarily commercial, and unless it’s a commercial corridor, 100% of the units must be below market rate. Even if it is on a commercial corridor, 15% of the units must be below market rate. AB 2011 also includes provisions for fair pay and additional training for construction workers. SB 6 expands the types of buildings that can be constructed in areas zoned for office, retail or parking. These buildings may be residential if they meet certain other criteria, many of which are similar to the requirements set forth in AB 2011.

The State of California sets housing goals for every city in the state. Many cities, particularly more affluent ones, frequently decide to simply not meet these goals, as it doesn’t really benefit them to do so. Their only incentive to follow through has been what is termed the “builder’s remedy, ” which requires cities with no plan submitted, or that fail to meet their goal, to permit any and all housing as long as at least 20% of it is affordable housing.

This law has actually been in place for about a decade, but it hasn’t been easily enforceable. Recent changes have made it more enforceable, so now cities have to start thinking about it. Not all cities have the same deadline for submitting plans, but there are already 124 cities in Southern California that are out of compliance. Northern California has until January to submit plans.

Opendoor is an online real estate business based in Arizona that buys directly from sellers instead of going through the market process. While nothing about skipping the open market is illegal, the problem comes from Opendoor’s claim that its service saves sellers money. As it turns out, this claim is entirely false.

Opendoor claimed that those who use their service save money because they will be selling at market value with reduced transaction costs. There’s no evidence whatsoever that these claims are true. In fact, there is evidence that many sellers who go through Opendoor actually net thousands of dollars less than they would on the open market, despite cutting out the middleman. As such, the Federal Trade Commission voted unanimously, 4-0, to approve a final order against Opendoor. The final order requires Opendoor to pay $62 million in consumer redress, prohibits them from making deceptive, false, or unsubstantiated claims, and requires them to provide evidence of their claims.

Construction has had multiple ups and downs in recent years as a result of the pandemic and surrounding economic factors. Throughout it all, multi-family construction has actually done pretty well. In fact, it’s currently at its highest rate in the last fifty years in terms of total number of new multi-family constructions. Unfortunately, that doesn’t mean it’s high — construction has been in a slump for the past thirty years, and meanwhile the population has been increasing.

Los Angeles has it the worst of any US metro, underproducing by about 400,000 homes. This is despite the fact that it’s also one of the top metros for multi-family construction. In large part, this can be attributed to the fact that it is the second most populated metro in the US. But the real issue is restrictive zoning laws, which are only recently being changed in California. The vast majority of homes in the Los Angeles metro are single-family residences because that’s what the lot’s zoning allows.

After the pandemic forced many employees to work remotely, it was initially unclear how long the remote work trend would last. Some thought everyone would return to the office after the pandemic was over. Some saw that remote work was actually working surprisingly well, and expected fully remote jobs to rise in popularity. The latter has definitely happened, however, employers’ attempts at a gradual return to office work have caused another trend to emerge: the hybrid work model.

It turns out an office has benefits and so does remote work. And this is true regardless of an individual’s preference, if they had to choose just one. So why not get the best of both worlds, and just go into the office sometimes? This will be great for workers — though not for owners of office buildings. Those who held onto the office space they owned may have expected a full return to office work, which would result in a return to normalcy for the office building market. What is happening in reality is a gradual reduction in office space. Office space isn’t being eliminated completely, since it’s required for a hybrid work model. But companies won’t need nearly as much office space, and are already making plans to repurpose the space they already have.

One of the offerings of the Department of Veterans Affairs is mortgage loans. Of course, this is limited to current or past members of the US military. With this restriction comes a few significant benefits if you qualify. VA loans have perks for both low-income and high-income homebuyers.

If you have the money to buy a more expensive home as long as you can get a loan, VA loans may have you covered. There are jumbo loans available which can even exceed $1 million. This may be a good bet even if you are not currently a high-income earner, as long as you are purchasing investment property. This is because there is no minimum down payment for VA loans; you can borrow up to 100% of the home’s value. You don’t even need to worry about private mortgage insurance (PMI), which is required for conventional loans with a down payment under 20%, but not for VA loans regardless of your down payment amount. If your investments pay off, or you start earning more money, you can also pay off the loan faster. VA loans have no penalty for accelerating payments.

Insuring your home against natural disasters can save you quite a bit of money in the event such a disaster occurs. Frequency of different types of natural disasters varies by region. While this is also true of floods, floods can occur pretty much anywhere, so flood insurance may be worthwhile regardless of whether you are in a flood zone or not. So what do you need to know about flood insurance?

Flood insurance is not legally required. However, some mortgage lenders may require it, especially if the property is in a flood zone. As can be expected, flood insurance premiums are higher in flood zones, since there is more risk. That also means it can be relatively inexpensive if your area is not flood-prone. Since floods still occur at a significant rate in such areas, it’s probably a good deal even if the lender doesn’t require it. If you do get flood insurance, whether you chose to or your lender asked for it, make sure to compare plans. Premiums vary by company, and most companies have more than one insurance policy. Most policies cover damage to both the building and the contents of the home, but you should check to make sure. Some plans also include replacement expenses.

If you’re selling your home, or getting ready to do so, you may have thought about some of your prospective buyers’ potential questions and what the answers would be. Many of these probably relate to the home itself or the neighborhood, and can be expected questions. However, some not so uncommon buyer questions are decidedly more bizarre.

Perhaps not entirely unexpected is the question of whether or not there have been infestations, and it’s a common one. This would obviously be a major concern for a buyers, but be prepared for buyers to be overly concerned about certain unlikely infestations. Buyers may ask about pests that don’t even live in your area. Another very common question that may seem a bit silly to some people is whether or not someone has died in the home. Certain superstitious buyers may think this means the home could be haunted, which would be a major turn off. You may not even know yourself whether someone died there or not if it happened a long time ago, but buyers like this will still want to know. A less common death-related question, though perhaps one grounded more in observable reality, is whether anything was buried in the home’s yard. It’s not uncommon for people to bury their pets in the backyard, but buyers or their own pets may not want to unearth something like that.

This month brings blues singer songwriter Teresa James, songwriter, producer, bass player, Terry Wilson (Teresa James and the Rhythm Tramps),guitarist, singer, songwriter Shawn Jones and our hostess, Jodi Siegel!

Every third Tuesday of the month, 3-4 singer songwriters of all genres, come and play their tunes in front of an intimate audience. Admission has been free but donations are strongly encouraged to help pay the musicians. It has become more than a local showcase, but a concert in an intimate setting and a great hang of like minded music lovers!

The venue has the down home feel of a neighborhood bar, with the ambiance of a small concert hall, an excellent sound system and every seat is VIP. The Showcase has gained a very loyal following of not only fans who attend every month, but it has also drawn some amazing music makers and hit songwriters too. Many have toured the world with legends.

Project Barley’s is located at 2308 Pacific Coast Highway, Lomita, CA 90717 They have award winning crafted beer, wine, sandwiches and their amazing pizza. For more information about the venue go to their website https://projectbarley.com/

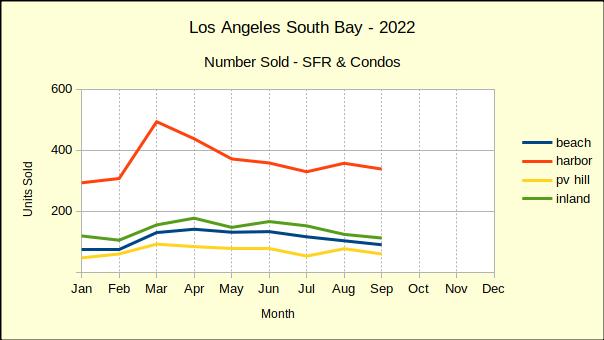

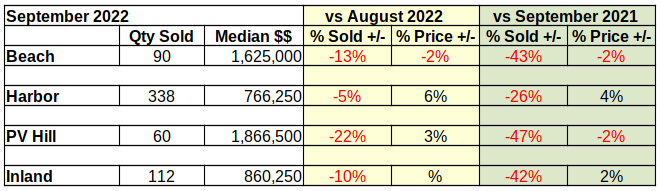

Last year saw home sales in the South Bay escalate dramatically as buyers sought to become homeowners while interest rates were still abnormally low. With interest rates rapidly rising it’s no surprise that sales are plummetting in 2022. The Harbor area, traditionally an entry level market, handily out-sold the balance of the South Bay with a drop of only 26%. The remaining areas suffered sales drops ranging from 42% to 47%, with the South Bay as a whole dropping 35%.

Compared to last year, cumulative South Bay home sales were down 21% as of September. The first three quarters of 2021 saw 7767 townhomes and single family residences sold, versus 6163 during the same period this year.

Recognizing that 2020 and 2021 were exceptionally aberrant, we also compared the 2022 year-to-date sales volume to 2019, the last normal year of business prior to the pandemic. As of the end of September 2022 cumulative sales volume was 4% lower than it was for the first nine months of 2019.

The decline from 2019 sales is uneven in that the biggest drop, 15%, is seen in the Beach area, which is typically at the high end of the market. Sales in the Harbor area only dropped back by 2%, while sales in the Inland area fell by 4%. The Palos Verdes peninsula fared best, actually increasing in quantity sold over 2019 by 4%. As always we offer a cautionary note when looking at statistics for property on the PV Hill. Because there are considerably fewer homes in that area, percentile statistics can take large swings.

Median Prices Mixed in September

The number of homes sold in 2022 has declined, indirectly affecting the median price of those homes, as well as the total dollar value of all the homes sold in the same period. A closer look at the median price of homes sold through September yields some surprising changes.

Since prices increased dramatically during the coronavirus pandemic we anticipated finding the median price from 2022 to be considerably higher than that of 2019. Indeed, that is the case with the median in the Beach area up 31% over that of 2019, the Harbor up 36%, PV Hill homes up a staggering 47% and the Inland area up 30%. But, that is gradually reversing.

July and August of this year showed depreciation in the median price across the South Bay. Prices consistently dropped in a range from 2% down (Inland) to 18% down on PV Hill. September sales broke the pattern with only the Beach cities losing value per the median. The Inland area was flat, showing no change from August. In an unexpected twist, both the Harbor area and the Hill came in with an increase in the median price. The growth was modest, up 6% for the Harbor area and up 3% for the Hill. Despite the slight improvement in September prices we anticipate continued downward pressure as inventory grows and time on market stretches.

Looking at the median price on a year-over-year basis, we find September with minor declines from August. The Palos Verdes cities showed prices dropping by 2% last month and this month. At the same time the Beach cities dropped 2%, while the Harbor and Inland areas increased by 4% and 2% respectively.

Median prices started 2022 with increases regularly coming in well above 10% growth. In April we saw the first negative where the median for the Hill fell 2% from 2021. Since then we have watched the rate of price appreciation decline from double digits until now in September with both the Beach and PV areas losing value.

We fully expect all areas of the South Bay to reflect declining median prices before the end of the year. While prices will be down on both a month-to-month and year-to-year basis, we don’t anticipate the median to fall below 2019 price points this year.

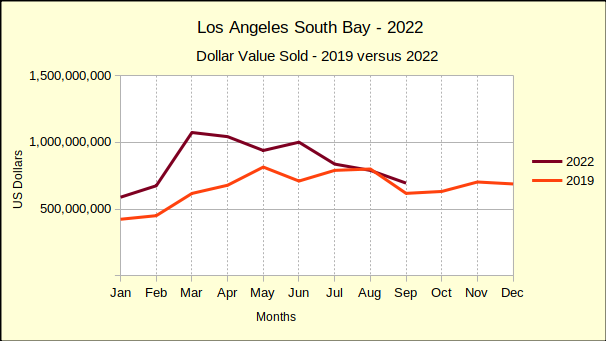

Total South Bay Sales Dollars

When the number of sales is decreasing and the median price of those sales is also decreasing, one has to assume the gross revenue will also decrease. Governor Newsome has been warning for several weeks that the 2022-23 fiscal year will not see the State level revenue surpluses California has been enjoying.

During the first quarter of 2022 gross revenue from real estate sales remained predominately positive, with year-over-year growth rates of about 6% per month. Since March the South Bay has only seen two instances of sales growth, 7% in the Harbor area for April and 3% in the Inland area for June. Every other entry on the chart is negative, with September declines averaging about 40%.

Cumulative sales for the first three quarters of 2022 were off by 29% compared to 2021. Our monthly sales dollars chart shows a zig-zag downward trend since spring of this year. Of course, 2019 is a more realistic point of comparison as a result of market gyrations created by the pandemic and our government’s fiscal response.

Comparing 2022 sales totals to 2019 yields a clearer picture of the current direction of the market. Instead of a sea of red ink, we can clearly see that 2022 sales have remained above those of 2019 with the exception of August. Sales started normally, then in March the Federal Reserve Bank announced a .25% interest rate hike, and promised more to come.

Buyers threatened with increasing monthly payments jumped into the fray and pumped sales up for a couple months. Then a new .5% increase, accompanied with the promise of multiple .75% increases throughout the year began a downward slide in home sales that is continuing.

Following the trajectory of the maroon line, and assuming the interest rates continue to increase, we predict 2022 sales will drop below 2019 again in October. The Federal Reserve Bank has already announced plans for another .75% increase in November, followed by a .5% increase in December. Adding another 1.25% will bring the full increase for the year to 4%. We envision the fall in sales growing steeper, bringing total sales below that of 2019 for the final quarter of the year.

Statistical Summary

This would be the heart of the discussion if we were dealing with a normal fiscal environment. Here we could talk about month-to-month changes and changes from the same month last year to this year. Instead we’re faced with an unanticipated side effect of the pandemic—out-of-control inflation followed by a steep recession.

The areas are: Beach: comprises the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: comprises the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: comprises the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: comprises the cities of Torrance, Gardena and Lomita.

Goodbye Marymount, Hello UCLA!

Marymount California University, is no more. But, shed no tears! The prestigious University of California at Los Angeles plans to open the site for classes in the fall of 2023-24. Escrow had not yet closed as of this writing, but all appears to be moving forward at good speed.

We are told the finalists included four developers and three educational institutions. We’re pleased that UCLA was the successful bidder. We’ve heard some of their ideas and look forward to having them as neighbors.

However, we’re also interested in what kind of potential the developers saw in this deal. There’s a total of 11 acres already developed as residential and 24.5 acres developed as a campus. What would that have looked like if a residential developer purchased the site?

The 24.5 acres, some of it with gorgeous ocean views, is the jewel in the transaction. A little “back of the envelope” calculation says that using an average of 15,000 square feet per lot, Which is about the average in that neighborhood, one could build about 70 high end homes at the location. New construction on similar sites is selling for about $7.5M today, giving a value for the finished project of approximately $525M. Not bad for a land purchase of $80M, especially considering we haven’t started looking at the 11 acres.

There exist some legal complications in the 86 unit, 11 acre property. Deed restrictions purported to require the land to be used to house students. That can readily be accommodated by an educational institution, like UCLA. Developers on the other hand might have to pay some serious legal costs to do anything else with the land.

And it might have been worth the legal expense. A quick look at the apartment building market in the South Bay shows roughly comparable buildings selling for about $420K per unit. That would make 86 units worth about $36M, almost half the stated purchase price.

We’ll never know what might have been. The entire South Bay can look forward though, to an educational revival. A refreshed campus with UCLA’s academic resources and access to the university program at AltaSea and other port projects is a great starting ground.

It’s long been suggested that one should put down at least 20% of the purchase price as down payment. While this is probably a good idea if you can afford it, many people have taken this advice a bit too much to heart, and are reluctant to try to buy with a lower down payment amount. A third of homebuyers even think it’s a requirement to get a loan.

In reality, most loans have a much lower minimum down payment, with one of the most common types — FHA loans — having a minimum of just 3.5%. Some even have no minimum. In addition, the median down payment is significantly less than 20% for first-time homebuyers at 7%. It’s higher for repeat buyers at 17%, but that’s still under 20%. What’s more, there’s a good chance you can get homebuyer assistance to help cover the down payment. While a majority of homebuyer assistance programs are specific to first-time homebuyers, over a third of the approximately two thousand programs do not have this restriction.

Investors are frequently asking whether the current investment market is better for stocks or real estate. Usually, there’s a correct answer. Right now, the best answer is probably not to invest at all. When this happens, it’s called a hold phase. Real estate being both a less volatile and more long-term investment makes it a slightly better method of investment during a hold phase, but it’s still likely better to hold off until home prices reach a bottom, which is likely to be around 2025.

Stock price movement is a bit harder to generalize since it changes so much more frequently than real estate prices. This is mostly because stock trades can be initiated and completed near instantaneously, while home sales typically take a few weeks between listing and accepting an offer. That said, it’s clearly evident that stock prices are on a downward trend right now, with an annual change of -17%. Until this bottoms out, it may be too risky to invest. Home prices, on the other hand, increased 12% in the past year. Normally this would make it an absolutely terrible time to invest in real estate, and it’s certainly not a good time to do so, but home prices are now decreasing. Better investment opportunities in real estate will crop up in a few years.

Much of the danger to tenants is being unable to pay rent, as both rental prices and cost of living continue to increase while the job market is still in recovery. However, that isn’t the only way tenants can get evicted. There are even a few ways landlords can legally evict tenants that haven’t done anything wrong. That isn’t enough for some landlords though, who are actually resorting to illegal methods of eviction instead of notifying the tenant and potentially going through the court process.

Though both are legal, the court process distinguishes at-fault and no-fault evictions. At-fault evictions are the category where failure to pay rent lies, and this category also includes various contract violations and criminal activity while on the premises. The no-fault category includes landlord’s intent to occupy the property, withdrawal from the rental market, property being deemed unfit for habitation, or landlord’s intent to demolish or substantially renovate the property. Some of these can be used misleadingly as the landlord can simply change their mind later, but the real problem is unlawful evictions. The Office of the Attorney General (OAG) is particularly concerned with the type known as self-help evictions. This includes the landlord shutting off utilities, changing locks, or removing the tenant’s personal belongings in order to force them out of the property. Landlords initiating a self-help eviction can get charged with a misdemeanor, and the sentence is either a fine or a jail term of a maximum of one year.

Home staging is one of the best ways to garner interest in your home. Your home should look like someone lives there, otherwise buyers won’t be able to imagine themselves living there. At the same time, it shouldn’t be too personalized, otherwise it will look like a home for you rather than a home for them. Fortunately, some of the most cost effective methods of home staging are also impersonal.

While it’s certainly more cost effective if done for you rather than a buyer, updating your lighting to more energy-efficient models is sure to relieve some stress from buyers. Purchasing new furniture is expensive, but a similar effect can be achieved at much lower cost with new slipcovers and bedsheets. Even if you plan to keep them yourself, or just use them for staging, a few plants can add vibrancy to your home, particularly if they are in bloom. An important step that costs next to nothing in money, albeit a significant amount of time, is giving your entire home a thorough cleaning.

Due to the Fed increasing benchmark rates, the rates of fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs) are both continuing to increase at a rapid rate. The current average 30-year FRM rate is 6.70%, and it’s 5.96% for ARMs, as of Sept 30th.

It’s normal for FRM rates to be higher than ARM rates, but that may not be the case soon, because of the reasons for the rapidly increasing rates. The ARM rates are directly tied to the benchmark rates — as the benchmark rates increase, the ARM rates will also increase proportionally. While FRM rates are also increasing, it’s not directly because of the increasing benchmark rate. FRM rates are actually tied to bond market rates. However, since the FRM rates are already increasing much faster than bond market rates, they can’t sustainably go much higher, while ARM rates don’t have that restriction and are quickly catching up.