When considering whether to take on a home improvement project yourself or hire a contractor, what immediately comes to mind is cost savings. While this is a real benefit of DIY home improvement, it’s not the only one. So even if you don’t need to cut costs, don’t write off the idea immediately. There are other considerations that may sway you.

Besides cost savings, the most significant advantage is control. You can work on your own schedule; no need to clear your calendar for appointment times. Contractors usually get materials from the same source every time, so the quality and range of choice isn’t guaranteed. Some will let you purchase the materials, but if you do it all yourself, you know that option is available to you. Another benefit is skill development. Whether you’re a contractor yourself or just a regular person, DIY projects are an opportunity to expand your knowledge base and practice practical skills. Once you do your first DIY project, future projects will be much simpler for you, so you can potentially avoid calling a contractor at a later date as well. A less practical, but still noticeable, benefit of DIY work is personal satisfaction. It’s well established that seeing a project through yourself from beginning to end, no matter what type of project it is, is highly fulfilling. It’s a very good confidence booster.

The current housing market is in an interesting position. Mortgage interest rates are high, but home prices are starting to cool off. It raises the question of whether it’s a good time to buy. The advantage of buying now is that home prices, while expected to continue to drop, are the lowest they’ve been in quite a while. That means you may be able to get a home at a decent price without heavy competition, and start to build equity. The disadvantage is that you’re locking in a high interest rate.

That’s where refinancing comes in. While the price of a house can’t be renegotiated once the sale is finalized, your interest rate can. This is why buying with a high interest rate can be appealing if other conditions are favorable. But this is risky, because you never truly know how long rates will remain high. It could take a long time for interest rates to drop, and it’s even possible that by that time, home prices will also be lower. In this situation, not only did you essentially overpay for your home, but you’ve been stuck with a high interest rate for longer than anticipated. It’s also worth noting that if the current interest rates scare you enough to already be thinking of refinancing in the future before you’ve even bought the home, there’s a good chance it’s because you can’t truly comfortably afford the payments for any considerable length of time.

So should you consider buying now and refinancing later? What it ultimately comes down to is that it’s a risky time to buy, and it’s not entirely clear whether it’s worth the risk even if it pays off. What is clear is that if you can’t afford to task risks, you definitely shouldn’t. But if you can comfortably wait as long as you need to, it simply boils down to real estate as a long-term investment. In that case, it’s actually one of the lower risk types of investments, but that doesn’t negate the fact that the risk is higher than usual in the current climate. The actual answer will depend on the individual and on the future, but likely answers are either “no” or “probably not.” What are some alternatives, then? Waiting for mortgage rates to drop, or even just waiting for home prices to drop more, since that can’t be renegotiated. In the meantime, you can also consider upgrading your current home to increase its sale value for when you do buy.

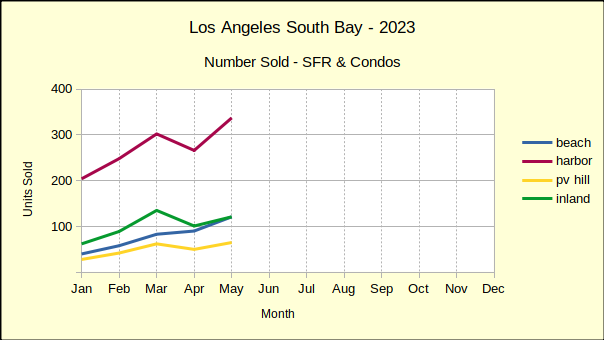

The number of homes sold in the Los Angeles South Bay during the first six months of 2023 is the lowest sales volume for a first half in the past five years. Fewer homes have been sold since the new year than sold during the same period of the worst year of the pandemic.

The first half of 2023 has ended with 24% fewer sales than the same period in 2022, which was itself down 15% from 2021. The peak of the market was early 2021, when interest rates were among the lowest in history, exploding the number of potential buyers. The lowest sales volume was during 2020 when 3311 homes were sold, which was still greater than the 3221 sold the beginning of this year.

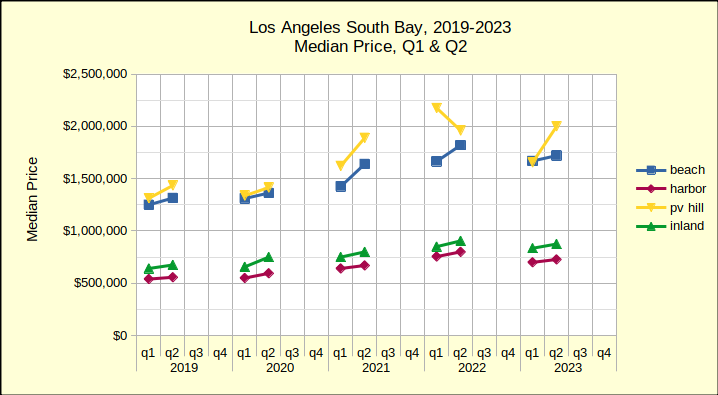

Median Price Begins Downturn

Coming right on the heels of the sales volume collapse is a drop in the median price. Prices today are down from where they were in 2022, which was the peak of the recent market. The chart below reflects the median price for the first and second quarters of the past five years. Typically, the first quarter is the slowest, with the number of sales increasing through the second quarter and then slowing again for the third and fourth quarters. Here the growth from Q1 to Q2 shows and we can see the change from year to year.

As always, bear in mind that the Palos Verdes Hill offers a comparatively small sample size, so a couple of significant sales can shift the plot lines dramatically on a chart. The chart above shows one such anomaly where PV the median price actually declines in the second quarter.

Looking across the years from 2019 all four areas show the same upward movement in median price until the second quarter of 2022. Then, comparing it to the second quarter of 2023, we can see the trend shifting downward. For example, the Beach Cities median fell from $1.82M in the second quarter of 2022 to $1.72M in the second quarter of 2023. The weakness in median prices is driven by increasingly steeper mortgage interest rates. Barring a change in market dynamics, anticipate this line turning into a steeper downslope for residential prices starting in winter of 2023/24.

When Is the Bottom?

The market is clearly taking a downward turn. Sales volume is off, median prices are turning down. Sellers are not putting properties on the market. Buyers aren’t buying. The few forecasters willing to make a guess this early are saying real estate won’t come back until 2025, possibly 2026. For those who are “waiting for the bottom of the market,” remember that by the time you read it in the headlines—you’re too late—the bottom is gone.

Beach Cities Sales Dropping Fast

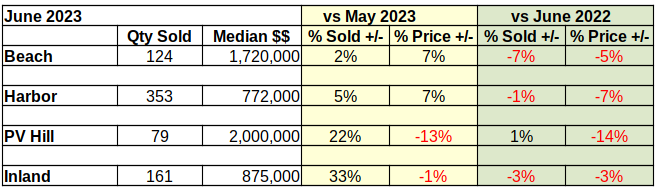

Median prices at the Beach have fallen 5% from last June, coming in this year at $1.72M, an even $100,000 below June of 2022. Year to year sales for June are down 7% from last year, at 124 units compared to 133 in June of 2022.

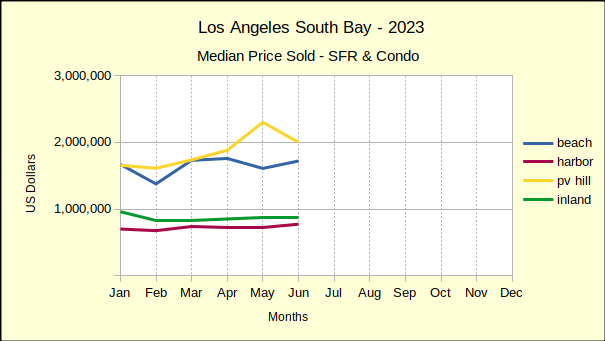

Month over month statistics have been highly volatile since the beginnning of 2023. Interest rates and prices have changed erratically, making short term forecasts nearly impossible. Month to month sales volume has bounced in a range from 2% to 45%. In just six months, monthly median prices in the Beach Cities have ranged between -18% and 26%.

Year to date sales volume at the Beach is down 25% from last year and is off a full 35% from 2019.

The year to date median is down 3% compared to 2022, though it is still 32% above the median in 2019.

Despite market conditions, homes in the Beach Cities remain highly desirable. For June, 78% of sales transactions closed within 30 days of listing and sold for 2.61 % above asking price. Beach homes also offer a great deal of diversity. June sales showed a 19 million dollar range between the low sale at just over $500K and the high sale at $19.5M.

Harbor Area Home Sales and Prices Down

Year to year-same month sales in the Harbor area have been negative since the first of the year. Prices were still holding up in June of last year, but sales volume had been dropping through all of May and June. As a result, the number of homes sold dropped a mere 1% coming into June of 2023. That looks good until compared with the year to date decline of 24%.

Market conditions in the Harbor last year gradually changed from joy for rock bottom interest rates at the beginning of the year to caution as sales tapered off and sales figures stated taking a hit. Median prices for June of the current year have fallen 7% from the June 2022 median of $830K.

Until now, the Harbor area has shown mixed results in the month over month statistics. For June compared to May sales volume was up by 5% (353 versus 337), while median price was up 7% ($772K versus $720K). Like the Beach Cities, the Harbor Area is following a more normal upward swing from the winter doldrums into the spring selling season.

That upward swing is not expected to go very high or last very long. At 1710 homes sold, year to date sales volume from January through June is down 24% versus 2259 sold in 2022. Sales volume is likewise down 17% from 2071 during the same six months in 2019. The variance in monthly sales is expected to drop into the single digits starting in July.

Median prices are down 4% compared to 2022 though still up 33% versus 2019. (Note: Using The Federal Reserve’s “target inflation rate”of 2% annually would have put the Harbor area median price increase at a little over 8%. That implies an “excess growth” of about 25% in median price during the pandemic buying splurge. Much of that difference, if not all of it, is expected to disappear over the next 18 to 24 months.)

June sales detail shows 77% of sales closing escrow within 30 days. Buyers were still bidding up, with the sales price exceeding the list price by 2.61%. The highest sale recorded in June for the Harbor was $4.25M; while the lowest was $527.5K.

PV Peninsula Volume and Prices Mixed

Palos Verdes, contrasting May versus June of 2023 shows a 22% increase in the number of homes sold for a monthly total of 79. At the same time, the median price dropped by 13%, falling to $2M even. Expectations for month over month statistics include fewer sales and more aggressive price reductions as 2023 wears on. The summer and fall months are projected to have weaker home sales, both in volume and pricing, as interest rates increase and buyers and sellers who “must move” run out of options.

Year over year same month sales, showed a volume growth of 1% (one sale), accompanied by a 14% drop in median price from $2.3M. That 1% increase is the first time in 2023 that any of the areas has shown positive growth in the number of homes sold. As such, and knowing that the PV Hill is considerably smaller that the other areas we measure, readers are cautioned about the wide swings in PV statistics.

Sales volume for the first six months of 2023 is down 26% compared to 2022 (326 homes in 2023 versus 438 in 2022. Similarly, sales are down 9% from 2019 when sales of 358 homes were recorded. Median prices of $1.8M for the same period are down 13% from 2022 prices of $2.1M and up 36% from $1.3M in 2019.

Market time has remained good, with 75% of sales closing withing 30 days. Sellers have enjoyed selling prices 2.3% higher than asking prices, a trend expected to disappear before the end of summer. Once again showing the range of homes available in the South Bay, the high sale in PV was $10M while the low was $610K.

Inland Area Makes Strong Showing

Sales volume of 161 homes in the Inland Area for June was up 33% over sales of 121 in May. With 33% more activity came a 1% reduction in median price, which fell to $875K after reaching $880K in May.

Comparing June of this year to June of last year showed a volume decrease of 3% from 166 in 2022. Likewise, this June showed a median price decrease of 3% from last year’s $905K.

Year to date volume for the first six months was down 68%, for 669 units sold, versus 869 in 2022. Going back to 2019, the most recent “normal business year,” sales volume was down 21% from 799 sold in 2019.

Median price of Inland area homes for the same six month period showed at $863K, down 3% from $887K in 2022; and up 32% from $652K in 2019. Days on market remained under 30 for 82% of the Inland area homes sold in June. Buyers offered 2.6% above asking price. The high market sale was $2.2M while the low was $390K.

People get the recommendation to “go green” all the time. But how does one actually do that? Well, there are several ecologically friendly options that you can take advantage of when making home improvements. The benefits of natural light and recycling are well known, but some of there tips you may not be aware of.

Eco-friendly materials doesn’t necessarily mean recycled. Bamboo and cork are particularly sustainable, and cork can be re-used easily. Locally sourcing materials can also reduce environmental impact by reducing transportation emissions. Look within 500 miles of your home if possible. Unfortunately, neither bamboo nor cork oak grows natively in California, but you can still source the products from local businesses. If it’s an option, choose programmable thermostats, low-flow showerheads, faucets, and toilets, low-VOC (volatile organic compound) paints, and Energy Star rated appliances.

Obviously, when looking at a home appraisal, the appraiser is the expert. But appraisers are still human, and can make mistakes. Make sure to read over the appraisal report, especially if you feel the appraisal value is wrong. It’s possible the appraiser entered something incorrectly or there was a communication error.

If you review the report thoroughly, you may be able to find discrepancies even if you don’t know much about appraisals yourself. If you do, don’t be afraid to talk to the appraiser about it. Sometimes just pointing out a mistake can solve the problem. If you do need to argue your case, though, having thoroughly read the report can only benefit you. This lets you potentially gather enough evidence that the appraiser revises their appraisal.

If that doesn’t work, you may have to request a reappraisal from the lender. Though, you should note that not all lenders allow reappraisals, and even if they do, they won’t accept your request without sufficient evidence. If you can’t get a reappraisal — whether the lender doesn’t allow them or the request was denied — the next person to talk to is the other party in the transaction. Be open with them and discuss the situation so they understand why you want to renegotiate. If you’re the seller, you may need to adjust the purchase price, and if you’re the buyer, you may need to explore other financing options.

For a long time, a new homeowner’s first purchase has likely been a starter home. A starter home means that the homeowner expects to live there a short time, sell once it appreciates, then buy a larger home. People generally live in starter homes between three and seven years. That trend is going away, though, for a few different reasons.

The largest contingent of homebuyers, and also first-time homebuyers, is currently Millennials, who are between 27 and 42 years old right now. This roughly corresponds to the 25 to 44 age range homebuyer contingent used by the National Association of Realtors (NAR). NAR discovered that among those in this contingent who bought a home last year, 40% planned to live in the home at least 16 years. Not only is this more than triple the average length of ownership of a first home, it’s also double the average length of homeownership overall. This value is 48% for the lowest age bracket, between 18 and 24 years old. For reference, Generation Z is currently between 11 and 26 years old.

The major reasons for this are economic. Interest rates have skyrocketed so high this year that those who have managed to find a home last year likely locked in a low interest rate. They’ll want to ride that rate as long as they can. Even those who weren’t able to find a low interest rate aren’t going to want to go through the hassle of finding a new home to purchase, as there simply aren’t very many homes available. Supply is lower than demand, and construction is still failing to meet demand, even as the construction rate inches back upward and demand has somewhat dropped off. They’re more likely to refinance once rates drop than look for a new home. Home prices are also a factor. Rising prices means needing to save up for longer, both before you buy your first home and while living there. There’s also a bit of a psychological factor here; if you need to wait a while to buy, you want it to be something worth the wait. There’s also another potential reason that economists may not notice at all, since it’s more cultural. Millennials are less likely than older generations to marry young or have children. This means they are also less likely to need a larger home. Their first purchase could look like a starter home, but it may actually be perfectly well suited to their long-term needs.

Real estate is widely considered one of the most reliable forms of investment. But that doesn’t mean you can go into it completely blind and expect profits. It’s entirely possible that even a bad real estate investment could net profits eventually, but you shouldn’t count on it. If you’ve never done any real estate investing before, make sure to do your research first. Even if you have, you need to be aware of shifting market conditions.

For those just starting out, start by gathering information. This could take some time, so don’t expect to start investing immediately. Build networks with more established investors as well as agents, property managers, and contractors. Do your own research as well, particularly by learning about the various property types, relevant laws, and financing options.

Once you know about investing in general, you can move on to researching specific properties to invest. Determine the goals of your investment. How much profit do you want? When do you need the money? What sort of risks are you willing to take? Knowing the different property types is particularly important for this step, since it allows you to better pick the right investment as well as diversify your investments. Now you can examine the market trends and see what’s available that fits your plan. If there isn’t much around, you may need to adjust your plan. When identifying properties, take into account factors such as the location, expected appreciation, rent values, and property condition.

Home improvement doesn’t have to mean large projects. There are plenty of quick and inexpensive DIY options that provide additional value to your home with minimal cost and effort. Some of these are frequent suggestions already, but you may not be aware of how efficient they are at improving the value of your home.

Some very common suggestions are repainting, improving curb appeal, and upgrading lighting. Repainting yourself sounds like a lot of work, but it’s still one of the highest value-to-cost investments possible, and may not actually take as long as you expect depending on the size of your home. There are many ways to improve curb appeal, but one of the simplest ones, adding plants or maintaining existing ones, doesn’t cost much at all in terms of either time or money. Upgrading lighting is generally a longer term investment, but this is not because it takes time to achieve, since it actually takes very little time. However, the benefit comes in the form of savings from reduced energy costs over time.

Less common suggestions include replacing hardware and fixtures, adding mirrors, and decluttering. Fixtures can be expensive sometimes, but they’re a solid investment in terms of value when you go to sell. When you’re living in the home, you often don’t notice small things like old doorknobs and drawer handles, but buyers will take notice if these things have been upgraded recently. Mirrors are surprisingly effective at improving the atmosphere of a room. They reflect natural light, making the space appear brighter, and also create an illusion of more space. Decluttering may not seem like it would affect your home value at all, since those items aren’t really part of the home. But prospective buyers will still take note of it and have a negative reaction to a messy-looking home, even if there’s nothing wrong with the home once it’s cleaned up.

The space mission Huginn, planned for August 2023, will be a six-month long research stay at the International Space Station. One of the astronauts on the mission, Andreas Mogensen, wanted to bring some sort of snack from Earth to keep his energy up during long research hours. Mogensen decided to look to his friend Thorsten Schmidt, a Danish chef who had previously worked with him on another mission.

Schmidt’s solution was a new kind of chocolate bar. These bars, which he calls SPACECRAFTED, have a dark chocolate base and contain over 70 natural ingredients. Schmidt checked with a food chemist with over two decades of experience, Lisbeth Ankersen, as well as the European Food Safety Authority to make sure SPACECRAFTED is packed with nutrients. But you don’t need to be an astronaut to get these chocolate bars. They’ll be available on Earth starting mid-August, with three flavors to start and more to come.

Starting from the beginning of 2023, and going until 2032, the federal government has announced tax credits for improving the energy efficiency of one’s home. Some of the credits apply only to primary residences; others apply to both primary residences and second homes. In either case, a tax credit of 30% of the cost of improvements can be applied to federal income tax.

The energy improvements that apply to either type of residence are rooftop solar panels, wind energy improvements, geothermal heat bumps, and battery storage. The types of improvements that apply only to primary residences, as long as they are energy efficient varieties, are heat pumps, heat pump water heaters, insulation, doors, windows, and electrical panel upgrades. This tax credit also applies to home energy audits. The primary residence only tax credit has a limit of $3200 annually.

Real estate has long been considered one of the least risky investments. The market always has its ups and downs, but this is also true of any other investment, and real estate never disappears entirely. As with any investment, it’s best if you know what you’re doing. However, even if you don’t make the best investment possible, investing in real estate rarely becomes disastrous except in the event of economic conditions that reach multiple markets and negatively affect large segments of the population. A mediocre real estate purchase generally just means you may have to wait longer than anticipated to profit off your investment.

With some other investments, bottoming out may mean the product is all but dead and it’s pointless to invest, so it’s better to wait until the prices are increasing, but still low. Not the case with real estate, given its cyclical nature. This gives you a lot more leeway in term of when to invest in real estate. Part of the reason for this is that homes tend to appreciate over time, rather than depreciate as many other products do. If inflation is high, while it may not be the best time to invest in general, diversifying into real estate is a solid option. This is especially true if you purchase a rental property, as rent prices also go up with inflation.

The scientific consensus up until now has been that the universe has been in a constant state of expansion since the Big Bang. The reason for this belief was the phenomenon of redshift. Redshift is the stretching of light wavelengths as an object moves away from the viewer. Because more distant objects had higher redshift, scientists interpreted this as universal expansion. There have certainly been disagreements on the various details, but this general assumption has remained relatively constant. But one topic of disagreement — the cosmological constant — has led some scientists to look at the issue from a different perspective.

But what is the cosmological constant, and why is it so contentious? The cosmological constant is the term for the background energy of space. When originally conceived, Einstein thought this constant to be equal to zero. However, when scientists began to notice that the expansion of the universe — as measured by redshift — appeared to be accelerating, they needed an explanation. It turned out that their hypothesis could be explained by having a cosmological constant that is not zero, but a positive number. Unfortunately, while this solved one issue, it created others. More and more calculations started simply not lining up to observations.

Lucas Lombriser, a theoretical physicist at the University of Geneva, thinks Einstein was right about the cosmological constant being zero. Lombriser proposes an alternate explanation for changes in redshift. He suggests that the identity of the elusive dark matter is an axion field. An axion is a hypothetical particle that is already one of the strongest contenders for the true identity of dark matter. According to Lombriser, the specific properties of an axion field could account for both dark energy and changes in redshift, preventing the need for universal expansion as a cause of redshift changes, thereby solving the dark matter problem and the cosmological constant problem at the same time.