Staging can be very helpful in highlighting the best aspects of your home. Decluttering and rearranging furniture can make your home look bigger or more airy. In some cases, it can even hide some minor flaws with clever placement of furniture. But there are some things mere staging can’t hide.

Buyers aren’t going to move your furniture around, but they may check under rugs. Cracked tiles are easily noticeable, and if you try to hide them, buyers will think you’re hiding an even bigger problem. Every buyer is going to look at the windows, even if its just to check out the view. Broken or cracked windows are very obvious. Same with torn screens, which are easy to replace. The most important issue to fix is any roof problems. Having a roof over your head is the reason to live in a home. Buyers will expect you to take care of it.

Utilities generally cost around $2200 annually, but energy efficiency improvements can reduce this number by approximately 25%. This comes with a high up-front cost, but it definitely pays for itself over time. What’s more, even simply assessing the energy efficiency of your home can improve the sales value — homes with an energy efficiency rating sell for 2.7% more on average, even if the rating isn’t great. All this requires is ordering an energy audit, regardless of the results. If you are improving your home, consider solar panels, which can increase the sales price by about 2-4% depending on the area.

If you’re worried about the up-front cost, there are a few financing options. The FHA has an Energy Efficient Mortgage that allows you to exceed your loan limit by an amount dependent on your energy efficiency. This program requires an energy assessment, unlike the simple program version of Fannie Mae’s HomeStyle Energy Mortgage. This program allows you to borrow up to $3500 to pay for either energy improvements or an existing Property Assessed Clean Energy (PACE) loan, though PACE loans have had mixed results against more traditional forms of financing.

The primary obstacle to homeownership has always been the large up-front cost and necessity to get a loan. But the monthly cost of homeownership has generally been lower than rent prices, making homeownership significantly cheaper in the long term. And in 58% of counties right now, homeownership is actually more affordable than renting for the median priced home.

That’s still the case now, but things are trending in the other direction. While home prices, rent prices, and wages are all going up, rent prices are increasing the slowest of the three. There may come a time when home prices have outpaced rent prices enough that renting is a more affordable option, even if you have the up-front cost of homeownership covered. However, it’s important to note that changes in rent prices can sometimes lag behind changes in home prices. Renters usually aren’t able to capitalize on swiftly changing markets because they need to wait for their lease to expire, and in rent controlled areas, landlords can’t raise rents directly to market value for tenant-occupied homes.

For many people, buying a home — especially a first home — is a stress-inducing endeavor. It’s common to worry about whether you’re actually making the right decisions. While no one can tell you which home is right for you, it’s surprisingly simple to figure out whether homeownership is right for you. Chances are, if you can, it’s a good idea.

The most important factor is whether or not you can afford it. Most homebuyers don’t have the money to pay cash for a home, which means you’re probably going to get a loan. That requires two things: a down payment and a high enough credit score. While it’s possible to qualify for a loan with a down payment as low as 3.5%, it’s probably not a sound financial choice. Higher down payments translate to lower mortgage interest rates, and they are also more appealing to sellers. Qualifying for a loan also requires a minimum credit score, as determined by individual lenders. If your credit score is low, it may be difficult to find a lender who will give you a loan.

There is one scenario in which buying may not be the correct plan, even if you can afford it. While renting is certainly more expensive than buying in the long term, and less stable, it could still be cheaper if you don’t plan to stay in one place for long. If you get transferred frequently for your job, it may be better to stick to renting.

Most Millennials know how to unclog their toilet without calling a plumber, but there are still a lot of things they simply don’t know how to fix themselves. Three-fifths of them wouldn’t have any idea how to fix a leaky faucet. Roughly half don’t know how to caulk tile, fix a garbage disposal, or clean the dishwasher filter.

Part of this is because of the advent of self-cleaning appliances. When the self-cleaning fails, or their replacement model doesn’t have it, Millennials simply never learned how to deal with it. It’s also the case that the Millennial generation has taken longer to move out on their own, which means they’ve had the help of parents or roommates to cover their gaps in knowledge. In other cases, they simply don’t bother. 36% don’t feel the need to clean the showerhead, even though only 29% don’t know how.

It’s not necessarily even a problem of the proper equipment. The vast majority own some of the most common tools, though a tenth don’t know the difference between a Phillips and flat-head screwdriver, even if they own both. Still, 27% don’t own a level, 30% don’t own a ladder, and 54% don’t own a stud finder.

Kitchens are generally a relatively small space. Unfortunately, they need to fit a lot of things — refrigerator and freezer, pantry, oven, dishwasher, sink, counter space, pots and pans. How do people find room for all these things in such a small area? Your kitchen space is probably already cramped, but you may be able to maximize the capacity even further.

Fridge magnets aren’t uncommon, but what is uncommon is that they’re used for any useful purpose. Knife blocks and spice racks can be magnetized and stuck unto your refrigerator. Just make sure the magnet is strong enough; these are not things you want falling. Speaking of racks, overhead racks utilize ceiling space rather than floor space, expanding the effective size of the room. In addition, wine racks don’t necessarily need to be used for wine. They can hold many kinds of bottles. Your cutting board may not actually need to be stored. It’s possible that it fits neatly over your sink. Another thing is drawer inserts. It may seem like they reduce your available space, and they do, by a small amount. But they increase the usability of your space by ensuring that you don’t need to dig through things you don’t need to get to what you do need.

2021 was a year of tears for many people. But, not so for most South Bay property owners. Briefly, median sales prices across the area increased between 9% (the Inland areas) and 24% (on the Hill). Those are incredibly large increases. To put it in perspective, the median price increase the previous year, 2020, was less than half that, ranging from 4% (at the beach) to 9% (Hill and Inland).

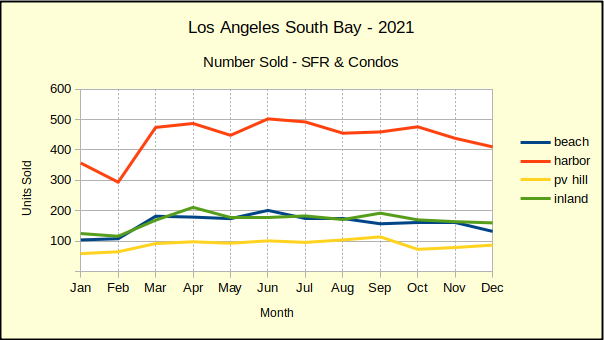

Similarly, the year over prior year sales volume for 2021 was up in a range from 18% (harbor area) to 22% (beach and hill). This compared to a range from decline of 6% (inland area) to an increase of 7% (hill) for 2020.

Along with median sales value increasing and number of units sold increasing, we also saw astronomical increases in total sales dollars for the year. The change from 2020 to 2021 ranged from 33% (harbor) to 52% (hill). That compared to a range from 2% (inland) to 20% (hill) for the transition from 2019 to 2020.

These huge percentages are uncomfortably like the years 2006 and 2007 leading up to the Great Recession. It’s highly unlikely that 2022 will continue at this pace. We anticipate the year starting out with listings priced on the high end, with subsequent price reductions as “distressed” properties come on the market with more appealing prices.

So called “distressed” properties include those which have been hidden from the market by the Covid-inspired moratorium on foreclosures and evictions. Now that lenders are allowed to process foreclosures, we are beginning to see properties come on the market as “pre-foreclosure.” Here in the South Bay we have yet to see any significant number of bank-owned property come on the market, though at least ten distressed homes have been listed in the past three months in Los Angeles county.

In the end, most real estate sales involve a family home where buying or selling is dictated by events beyond the property owner’s control rather than by market trends. Births, deaths and new employment top the list of reasons for transactions that will happen regardless of market conditions. If you anticipate a need to sell in the next few months, we recommend you consult with your broker/agent early. Ask about marketing or negotiating techniques that will deliver the best result in a slowing market given your circumstances.

Year-End Housing Sales Drop

Regular readers will recognize that we’ve been seeing the sales volume declining for a couple months now. On the one hand, it’s understandable because we report actual sales results, as opposed to seasonally adjusted results. Being the winter season, sales are slower.

On the other hand, nearly everyone has been ignoring the white elephant in the marketplace. Let’s face it, prices have gone up dramatically, the interest rate is climbing at a quickening pace, and inflation is on the rise. Combined, those factors foretell fewer qualified buyers, more inventory on the market and some pullback on the recent price increases. We’ll talk more about that next month when we take a first look at real estate in 2022. If you’re about to make a move and need information sooner, give us a call.

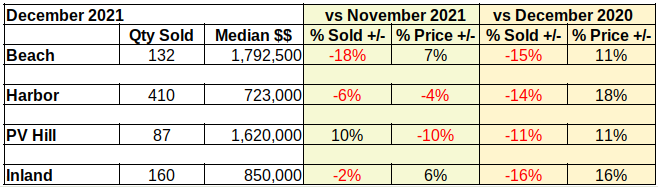

Sales quantity fell off from the November numbers everywhere except in the Palos Verdes area. There we found a healthy 10% increase in activity for December. (With a hundred or fewer units sold in any given month, statistics related to sales volume on the Hill can have some wild variations.) Sales rose by 10% from last month, but fell 11% from last year.

Harbor area sales slowed the most in the South Bay. Of course, sales there and in the Inland cities had increased dramatically early in the year. The confluence of low interest rates threatening to go up, with burgeoning demand from first time buyers, drove sales numbers all year. As the mortgage interest rate passed three percent, many of those first timers fell out of the market.

Year-End Median Prices Mixed

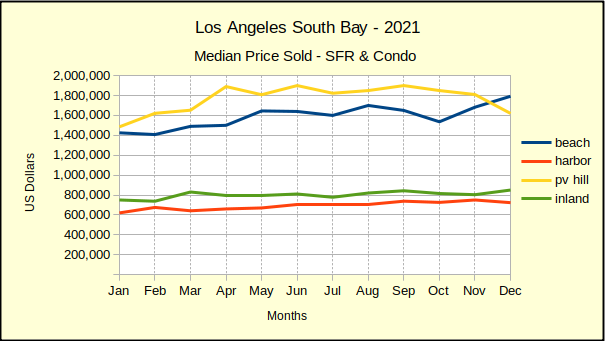

Palos Verdes homes brought in 24% more in median prices last year than the year before, which was 9% above 2019. Most of the 2021 increase came in the first three months of the year. Prices were stable for the summer before dropping in the fall. At the same time, Beach homes went up 19% in 2021, compared to a 4% increase in 2020 over 2019. Much the same in the Harbor area, median prices doubled, up 15% over 2020, compared to 7% above 2019.

In an interesting anomaly, prices in the Inland increased 9% over last year, which was 9% above 2019. It seems the purchasing mania and bidding wars didn’t have as much impact to Inland areas.

By mid-year all areas had seen one or two months of declining median prices on a month-to-month basis. As the year wore on, the “down” months grew and the “up” months shrank. Despite the year-over-year median price being up, three out of the final six months of the year saw declining median prices in all areas.

On a month over month basis, selling prices on the Hill were the most impacted in December, dropping 10% from November. Harbor area homes fell by 4%, while Inland property values were up 6% and homes at the Beach grew 7%.

The Beach areas enjoyed significant appreciation in 2021. Prices at the Beach started the year at just over $1.4M, moved quickly up to $1.7M in August, then lost $150K of those gains before springing up to close the year out at a median price of nearly $1.8M.

Year-End Total Sales Dollars

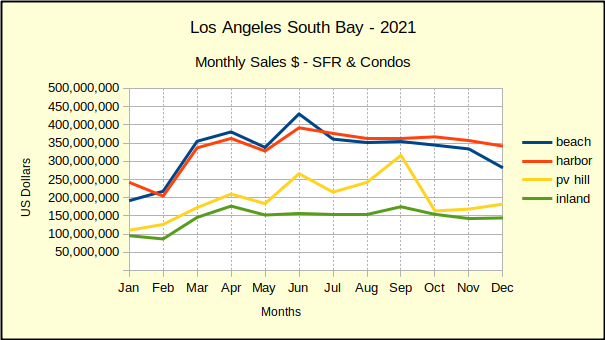

The total dollar value of all the homes sold in the South Bay in a given month or year is probably only useful to investors or economists. At the same time it can be instructive by way of demostrating market direction. For example, let’s look to total sales on a monthly basis.

In total dollars South Bay homes sales for 2021 were up 38% from 2020 sales. That compares to a 10% increase from 2019 to 2020. Looking at individual months, the bulk of that revenue increase happened between January and July. By August the 2020 to 2021 increases had slowed to single digits. By December, the Beach and Inland areas were already seeing monthly declines compared to 2020.

The December year-to-year decline in total sales dollars was only 5% at the Beach but compare that to an increase of 156% in April. The Inland areas dropped 3% for the same period, compared to a 159% increase in sales for May. Harbor area sales were up 8% compared to 106% in May. Palos Verdes December sales were up 2% compared to 228% in May.

What does all this mean? For most of 2021 we cautioned readers that year to year comparisons were problematic because in 2020 no one was truly prepared for Covid. Business exploded in the first three quarters of 2020. It took until August and September of 2021 to get past the previous year’s damage, so camparisons were even explicable. Until then nothing is there to compare to. Businesses were locked down. Consumers and retailers alike were hunkered down at home. That’s why 2021 annual percentages are so large–they’re an anomaly! Only the last few months of 2021 are valid comparisons to historically relevant statistics.

In Summary

From our perspective it looks like we’re headed into a correction. One might even look at it as a correction from a correction. It’s as though the real estate market over-corrected from the Covid collapse and boomed for about three quarters. Now we’re coming back down to some pretty solid numbers.

We expect January 2022 to look a lot like this table, with some moderation of the numbers. That moderation should continue into the year as sellers and buyers move closer together on their initial expectations. By the end of summer we predict the market will show the first indications of pulling together for another roughly 10 year cycle.

We like to think of the proverbial real estate cycle as three steps forward–one step back. It’s important to note that this is the “back step” of the cycle. As such, it’s probably the lowest price a purchaser can expect to see for that product in the next decade, if ever again. At the same time, it’s probably the last opportunity for a seller to trade up without having to make significant upgrades to the product, or taking a big hit for deferred maintenance. By 2023 we should be working on building long term market value.

Thank you for reading. Our lead photo is courtesy of Michael Fallon. See https://unsplash.com/@fallonmichaeltx . As always, we’re here if you have a question or want to bounce an idea off us.

Traditional water heaters are generally not visually appealing, and are often hidden as much as possible. But a water heater is a pretty important appliance, so no one wants to go without one. There is one potential solution: a tankless water heater. This choice isn’t for everyone, though. Going tankless has pros and cons.

You aren’t going to be worried about someone seeing your tankless water heater. They’re much smaller — about 20 in by 28 in, rather than 24 in by 60 in — and feature more appealing designs. This also means they free up more space, which always impresses buyers. Tankless water heaters also are significantly more energy efficient. This is because they heat the water only when needed, rather than constantly. It also leads to them lasting about twice as long as traditional water heaters, about twenty years rather than ten.

The big drawback? Well, they don’t have a tank, which means they can’t store large quantities of water. Their effectiveness is limited to a few gallons at a time, so running the dishwasher and washing machine at the same time, or two people taking a hot shower simply won’t work. The other con to tankless water heaters is that they’re more expensive, at approximately $1000 compared to $300-400 for a traditional water heater. Given the higher energy efficiency and longer lifespan, you’ll likely save money in the long run, but the upfront cost difference is significant.

With government support having ended, this may prompt people to think the economy has stabilized and recovery is imminent. But this is just the precursor to a stable market. The market needs time to adapt under normal conditions, and probably won’t become stable again until 2024. The main factor in overall recovery is the job market, which has yet to fully recover, and a stable real estate market requires construction to catch up to demand.

Some policies remain from government actions during the recession, though. Three laws — SB 10, AB 345, and AB 571 — will help out in construction efforts. SB 10 allows more areas to be zoned for up to 10 units, AB 345 allows ADUs to be sold separately from the primary residence, and AB 571 prohibits impact fees on affordable housing. Two more laws, SB 263 and AB 948, reformed bias training for real estate professionals. This legislation should have lasting impact in making the recovery more comfortable.

The percent of income put into savings on average fluctuates rapidly, but for the most part tends not to be subject to sudden large shifts. There have been a few notable spikes or dips across the decades, but nothing like the pandemic spike. April 2020 saw a record-breaking 34% savings rate, attributed to lower spending during lockdowns in tandem with stimulus payments. There was a second less major spike after the second round of stimulus payments.

The 34% rate was approximately double the record in prior years, which was back in the 1970s. That prior record was still only a 2% difference from the prior year. By contrast, in October of 2019, the personal savings rate was 7.2%, a 26.8% difference. The most recently calculated rate, in October 2021, was nearly identical to the pre-pandemic rate, at 7.3%. The savings rate has still been trending upward in the past couple of decades, though, after a relatively steady decline since the 70s, bottoming out in 2005.

Increased demand following the lockdowns meant that many people were eager to buy in 2021, especially first-time homebuyers, 85% of whom were renting at the time. Unfortunately, many of them weren’t able to because of heavy competition, with over 25% making an unsuccessful attempt. That hasn’t deterred most of them, though, with 72% of prospective first-time homebuyers expecting 2022 to be their year.

However, it’s important to note that less than 15% of those now looking to buy in 2022 were already looking in the beginning of 2021. That means it’s unclear whether they’re only recently planning a move to homeownership, or they deliberately avoided the highly competitive phase. It’s possible that they’ve only recently acquired the means to purchase, but it’s also possible they’ve had the money lined up and held off for a better time. In any case, optimism is strong among the current group of prospective first-time homebuyers.

Two-thirds of homeowners feel they spend a large portion of their annual income just on their house. For 54% of homeowners, it’s their single largest financial burden. Most homeowners are well aware that homeownership is costly, yet still worth the price. Nevertheless, just over a third are struggling more than they expected with the annual cost of things such as mortgages, property taxes, and maintenance.

Housing costs are also increasing over time, which is contributing to the unexpected struggles. Single-income households are certainly worse off, but even dual-income households are having financial woes. But the most significant contributor to unexpected costs is repairs and maintenance. It seems most homeowners simply don’t consider how much it could cost to maintain their home. However, even costs that are laid out ahead of time are causing more strain than people realize. Almost half of homeowners didn’t think HOA costs would be such a big deal.

Interest rates are by no means high right now, but they’ve been steadily rising and can no longer be considered low. Prices have also been high, but they’re predicted to drop dramatically, for a couple of reasons. First, inventory is opening up as foreclosure moratoriums and forbearance programs are ending. The other reason is that the Fed has been reducing their mortgage-backed bond (MBB) purchases. Tapering back MBB purchases will both lower prices and increase interest rates.

The Fed had previously announced plans to keep the Federal Funds Rate at its current value of zero through 2023. However, they’ve now decided that 2022 the year to begin returning to normalcy. With scaled back MBB purchases, the zero benchmark rate is the only remaining factor in economic stability that isn’t transitory. Increasing the benchmark rate will further increase interest rates, though, so 2022 is going to be a year of higher interest rates, but lower home prices.