There are many similarities and also many differences between the current recession and the Great Recession of 2008. Two of the core similarities — and the ones that define a housing bubble — are that prices are accelerating faster than purchasing power, and that there are changes in consumer values. While legislation and shifting values have addressed some of the issues that contributed to the Great Recession, most notably subprime lending, ultimately the crisis was a relatively natural economic response to the events that triggered it and followed a normal boom-bust-rebound cycle. The 2020 recession is somewhat of a reflection of this, though the specifics differ. The economy was already headed towards a natural downturn in the cycle, but the process was sped up by the COVID pandemic.

That’s where the similarities end, though. While nearly everything is ultimately tied to the economy in some way, it’s the pandemic, more so than economic conditions, that prompted valuation changes. Preference for larger homes and home entertainment, rather than homes closer to work and out-of-home entertainment, will probably continue as long as work-from-home remains a common practice, which will likely last a while. It’s true that people are leaving large cities and moving to cheaper areas, but this is more so out of necessity than desire. Peoples’ tastes have actually become more expensive, even if their wallet isn’t any larger. An economic downturn wouldn’t prompt this behavior. The only reason this isn’t currently sustainable is that the market hasn’t recovered yet. Once it does, probably around 2024-2025, it’s likely that the bubble will slowly deflate rather than explode.

I’m sure some of you haven’t heard of the term bioprinting. It’s a relatively new concept, combining stem cell research with 3D printing to print biological matter. Earlier this year, ribeye steak was printed using this method in Israel. The latest development out of Japan is a more complex cut of meat — Wagyu beef, known for its intricate fat marbling. The team at Osaka University has managed to perfectly replicate the look of Wagyu beef using 3D printed muscle and fat tissues, and their new methods provide a more accurate texture.

There’s still more research to be done, though. Though it certainly looks and feels like Wagyu beef, no one actually knows whether or not it tastes like Wagyu beef, or is even edible at all. More studies will be needed before the regulatory agencies in Japan will greenlight testing the cooking and consumption of bioprinted meat. In addition, the goal of sustainability is a long ways off with the cost of production being so high.

Fannie Mae keeps track of the Home Purchase Sentiment Index, or HPSI, each month. From July to August, the change in total value was negligible, from 75.8 to to 75.7, though it’s down 1.8 year-over-year. But the HPSI is a composite of six different categories, and none of them were without change. Three categories increased and three decreased.

Notable changes were an increase in those who believe it’s a good time to buy and a decrease in those who expect home prices to increase over the next 12 months. While the number who think it’s a good time to buy is still not a majority, it’s approaching a third at 32%. In July, only a bit less than half — 46% of respondents — expected home prices to increase. In August, this dropped to 40%. Only 24% of respondents believe home prices will decrease.

The Federal Housing Finance Agency (FHFA) established the First Look Program back in 2009, aimed at promoting neighborhood stability by facilitating occupation of real estate owned (REO) properties by owners. The program created a special time period during which prospective owner occupants, public entities, and nonprofits would have exclusive rights to purchase properties owned by Fannie Mae or Freddie Mac, before investors would have access. Until now, this time period was 20 days. On September 1st, the FHFA extended this period to 30 days. They deemed this move essential during a period of low supply, to reduce the level of competition prospective owner occupants have to contend with.

In July, the Pew Research Center conducted a survey that asked the following question: Would you prefer a community where homes are larger, farther apart, and farther from amenities, or smaller, closer together, and closer to amenities. The answer was 60% for the former and 39% for the latter. When they conducted a similar survey in 2019, before the pandemic, the numbers were significantly closer: 53% to 47%.

Because each of the two responses involves three separate categories, it may be difficult to tease apart which one respondents were most focused on, or if they were considering all of them equally. The survey didn’t ask that question, and it’s unclear why the three separate factors were lumped into one question. Still, we may be able to guess what changed since the pandemic. It’s already established that the advent of work-from-home has caused an increase in desirability of larger homes, with room for a home office, larger kitchen space, and additional personal entertainment space. For a time, lockdowns and increased reliance on delivery services also meant that people weren’t really going to stores or restaurants anyway, so they didn’t care how far they were. It’s possible that social distancing has conditioned people to want their homes farther apart as well, but this seems either unlikely or a negligible factor.

For a few decades, the average period of time that a family stays in their home before selling has hovered around six years. However, in recent years, this number has climbed up to around nine years. Why the increase, and what does this mean for the housing market?

There could be multiple factors contributing to the increase, but a couple are fairly easily understood. The market crash in the late 2000s led to a price decrease, which encouraged sellers to wait longer for home values to go back up. Even once prices starting increasing again, not everyone was confident in the stability of the market or their own personal economic stability. Another reason is that the largest market group is currently Millennials, who have a relatively low homeownership rate, in no small part due to various economic factors largely outside their control. Not being homeowners, they aren’t able to sell, so they have no impact on the average length of homeownership.

Average length of homeownership is an interesting statistic to follow, but since it hasn’t changed in so long, it’s not entirely clear what the impact could be. One could guess that it would have a negative impact on available inventory. This could be a problem for anyone looking to buy, but also could further contribute to increasing average length of homeownership for people who don’t actually want to stay in their current homes, but have no option.

Credit information is valuable to hackers looking to open accounts in someone else’s name. If you don’t need to access your credit report yourself in the near future, one action you can take to avoid this is a credit freeze. Not everyone is aware that any consumer is allowed to freeze their own credit reports, and potentially their dependents’ credit reports. And it’s now easier than ever, since it recently became free to do, as opposed to incurring a fee.

The process doesn’t take long to do, and is easy to reverse if needed. Any of the major credit bureaus — Equifax, Experian, and Trans Union — must freeze your credit if requested within one business day. Unfreezing your credit if necessary only takes up to an hour, but you’ll need to contact all three major credit bureaus rather than just one.

The US Senate has now passed a bipartisan bill aimed at improving infrastructure. The bill details budget investments for repairs, updating, new construction, and weatherproofing. Much of the money is aimed at roads and bridges, and various different budget plans all focus on clean environmental efforts, such as clean water, clean energy, and electric vehicle chargers. The bill doesn’t have many provisions that explicitly focus on housing, but improving infrastructure will have an indirect impact.

The most significant impact on the housing industry will be in job creation. While some of the positions that are being funded already exist, others don’t and will need to be created. This means more people will need to be hired. The slow recovery of the job market is the primary reason our recovery from the recession has been so drawn out. The infrastructure bill will hopefully not only establish a better infrastructure for the future, but also create more jobs now to speed up recovery. With a recovery of the job market, housing market stability will soon follow.

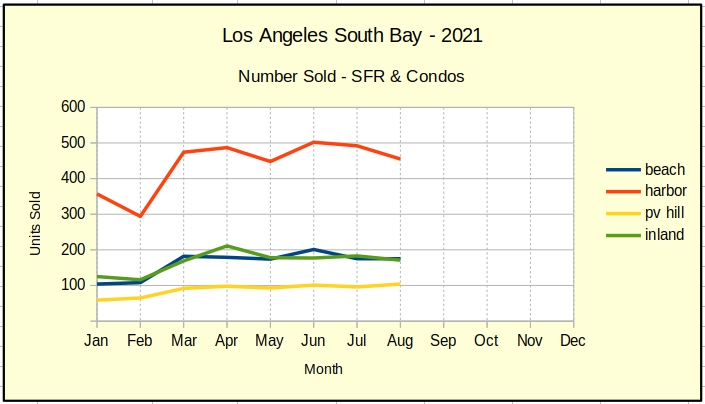

Back in 2019 the first eight months of the year saw 5,706 homes sold. During the same period in 2020, in the early response to Covid-19, sales dropped off by 12% to 5,003. As the market came out of the Covid doldrums in 2021, sales took a dramatic 57% jump. It’s most easily seen looking at the sales volume for the Harbor area in March on the chart below.

Part of that jump was the approximately 700 sales which didn’t happen in 2020. We don’t know how many of those “deferred” transactions have jumped back into the market. As of August the South Bay sales were at 6845, a 20% increase over the 2019 sales for this point in the year.

Seeing that a huge part of the March increase came in Harbor home sales tells part of the tale. The biggest piece of that market in recent months has been entry level or first time home buyers. Closely following are investors in small income properties.

Stories from the street imply that the growth in ADU additions and conversions has had an out size impact on that market as well. Both homeowners and landlords benefit from having additional living spaces.

For right now, the pandemic appears to be fading, which would tend to boost sales. Similarly, the low mortgage interest rates continue to support the market. At the same time we’re moving into fall and winter, when sales typically slow. August showed just a hint of a seasonal downward movement. September should be a directional indicator.

Sales Prices Up

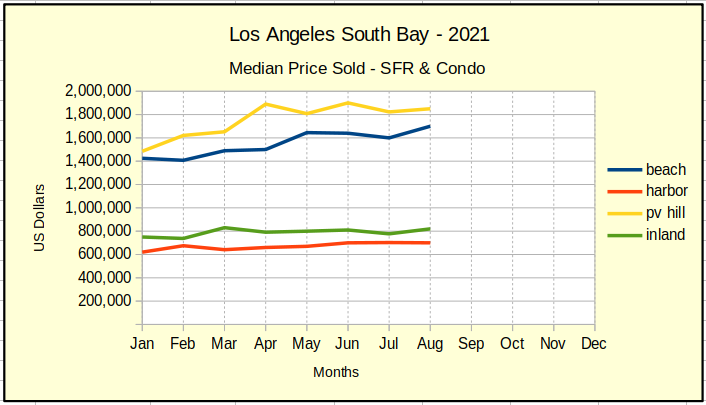

That jump in sales volume was accompanied by a bigger jump in the median price of the homes selling. Pent up demand and low interest rates combined to create bidding wars and drive median prices up. As of the end of August, the median price of a home at the Beach was $1.7M. That number was $1.5M in 2019 and $1.4M in 2020.

Median prices on Palos Verdes trended about the same at roughly $100K more per unit.The Inland cities and the Harbor area both showed mosest increases in the $50K neighborhood.

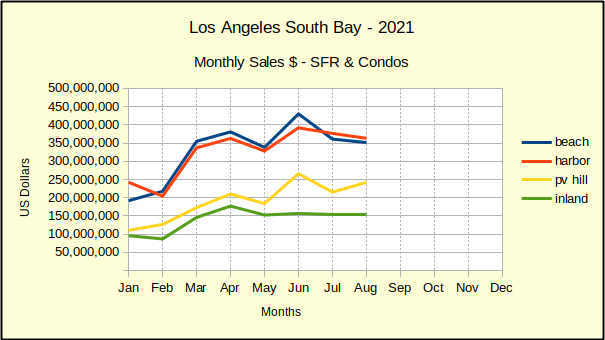

Area Sales Dollars Slowing

The monthly sales value of homes sold across the Los Angeles South Bay for August declined in all areas except the Palos Verdes Peninsula.

Compared to July, the number of sales on the Hill increased 8% in August, with a 2% increase in median price. That translated into a $150M increase in monthly sales since the first of the year.

Activity in the Inland cities has been stable for three months already, having risen about $50K per month since the first of January.

Monthly sales at the Beach and in the Harbor area pulled back for a second month in succession. Looking at the blue line for the Beach, we see a sharp drop in July which softened considerably in August. The Harbor area shows a steady decline over the same period.

As of August monthly sales totaled ~$150M higher than the beginning of the year at the Beach. During the same period monthly sales totals were up ~100M. As we move into the fall and winter season these numbers should slow somewhat.

Statistics – by Month, by Year

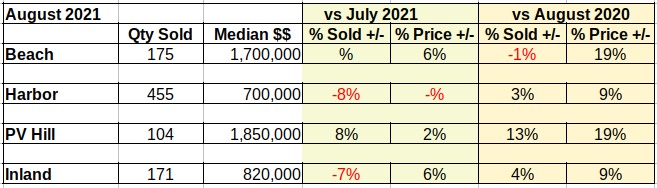

Interestingly, the number of homes sold in the Beach cities was unchanged from July, while the median price increased 6% at the same time.

There were 175 homes sold in both months. So how did Beach homes grow from a median price of $1.6M to a median price of $1.7M in one month? In July, 27 of those properties sold below $1M. In August, only 20 sales closed escrow for under $1M. The entire market simply moved up, pushing the median price up $100K in one month.

On a month to month basis, prices are holding or increasing across the board. At the same time we’re seeing slowing or flat sales everwhere but Palos Verdes. Continued slowing for the season is to be expected.

There’s still a lot of buyer traffic at open houses, but sales volume is slowing and buyers are showing price resistance. There’s also some chatter out there about what’s beginning to look like inflation in the real estate market. My crystal ball is showing a slow steady ride through the next month. It’s all cloudy after that.

Many renters feel like they will always be stuck renting. For some of them, that may unfortunately be true. But for those who are able to afford to buy but are afraid of mortgage debt, you may actually be better off buying a home. It’s true that sale prices are still increasing, but so are rent prices, which hit new highs in July in 40 of the 50 largest metro areas. The median rental price in the US is $1607 as of last month. The median mortgage payment for a starter home is about 15.5% less than that.

Of course, there are many factors that can adjust these numbers. Rent prices and home prices both vary depending where you live. It may not be easy to find a starter home in some neighborhoods. In areas with rent control, your rent may be relatively low if you’ve been in the same place for a while. Mortgage payments depend on your down payment as well as the home’s price. If you’re a renter, it’s not a guarantee that you should go out and look for a home right now, but you certainly shouldn’t dismiss the idea.

When budgeting monthly costs, homeowners generally take into account mortgages, real estate taxes, and homeowner’s insurance. Unfortunately, they all too often forget about maintenance and repair costs. It’s a good idea to set aside 1-3% of the home’s value for repairs and maintenance. You may not always know when you need repairs, but you do need to be prepared to pay for them.

Regular maintenance can also help lower the costs of repairs. Major repairs are less likely to be necessary if you can catch problems before they get too big, and you’ll probably end up paying more for even a single major repair than for regular maintenance and minor repairs across the year. A few things you should do every month are check HVAC filters, look for water leaks, check the vent hood in your kitchen, ensure carbon monoxide and smoke detectors are operational, and look for cracks in the foundation. All of these can be done yourself, and if there’s no issue, you don’t need to pay anything.

Here in California, we don’t have much in the way of seasons, but there are still certainly cold or rainy areas of the state. If your area freezes in the winter, look for ice dams on the roof, inspect for gaps under doors and windows, and consider protecting your AC unit from snow and ice if necessary. Your windows and doors should also be inspected during the spring, if your area gets a lot of rain. You should also get your HVAC and roof professionally inspected. Take care of any clogged gutters as well.

Our recovery from the 2020 recession has been described as a K-shaped recovery. Generally speaking, this means that the recovery occurred at starkly different paces for different segments of the population. More specifically for 2020-2021, while wealth decreased for many groups, it actually increased for those who were largely unaffected by the circumstances of the recession — in this case, primarily job losses and lockdowns. Many of those who were able to keep their jobs and continue to work from home during lockdowns enjoyed their reduced daily spending and lower mortgage rates.

This led to a increase in demand across the board, but notably in one sector of the market: vacation homes. Those who were affluent enough to possibly purchase an additional home were encouraged to do so by low mortgage rates and increased savings, and higher-income jobs are actually more likely to be able to be done from home. In California, the trend was first made obvious in October 2020, which saw a 120% increase in second-home demand from the prior year. The trend continued, though, demand for second homes increased 178% between April 2020 and April 2021. Rising prices dampened the effect, but it only slowed when lenders tightened restrictions on mortgages for second homes and lockdowns ceased being much of a factor.

Much of California, especially Central and Northern California, is experiencing a major drought much like the one from 2012-2016. Temperatures are going up and precipitation is going down. While water usage is still below 2013 levels due to lasting changes in water use habits from the last drought, conditions aren’t currently improving. It’s not precipitation levels that directly affect how much water a community receives, though. Some of the communities struggling the most actually have more rainfall than others but are lacking the infrastructure to account for drought conditions, and possibly the money to build said infrastructure.

Speaking of building, the drought is also affecting home construction. At a time when lumber prices are just starting to slip back down, a new threat emerges. And this one hits even the wealthiest of construction companies, who didn’t necessarily mind high lumber prices. Under drought conditions, some areas have placed restrictions on new construction to ensure that they meet water availability standards, and several areas simply never will meet the standards. The city of Marin is considering a move that would effectively ban all new construction for a time — temporarily banning all new water hookups. The legislation isn’t aimed directly at builders, but of course, all new constructions do require water hookups.

On average, the smaller a home, the less expensive it will be. So you’d think that buying a tiny home — one under 600 square feet — is going to save you a lot of money. Well, that’s only true if you’re looking at just the total purchase price, which is $52,000 on average. That’s 87% less than the average price of a typical home. However, most tiny homes are actually significantly smaller than 600 square feet, averaging only 225 square feet. This makes them about 62% more expensive per square foot than your typical home.

Of course, price per square foot only matters if you actually need the square footage. But at only 225 square feet, you probably do. For comparison, the typical bedroom is about 132 square feet — more than half the size of an average tiny home. Even the smallest of kitchens is usually just over 100 square feet. That leaves absolutely no room for storage, and you’re going to need to do your laundry at a laundromat. Many tiny homes are also completely off-grid and may even lack a sewage system and utilities. Not only is this highly inconvenient, the expenses can rack up, and they’re costs you aren’t likely to be able to easily recover by selling the home later.

Everyone knows college is expensive. Tuition costs aren’t the only reason. Room and board can also be rather expensive. In fact, it’s quite possible that it would be more than the mortgage payment on a new house. That means it may actually be financially beneficial to just purchase a house for your college kid, instead of sending them to the dorms or campus apartments.

Of course, this depends on multiple factors. Of course you’ll need to take into account the actual cost of room and board as well as expected mortgage payment for the property, but there are other financial considerations as well. You’ll need to be able to afford a down payment, first of all. Are you able to turn it into a profit opportunity by renting out some of the rooms? If so, do you need to hire a property manager? Once your kid graduates, are you going to keep the house for them, sell it, or continue to rent it out?

There are additional considerations that aren’t necessarily even financial. How far away from your kid do you want to live? Maybe you should consider moving with them, if that’s a possibility for you. Is giving your kid the responsibility of owning a house a good learning opportunity for them, or is it just going to result in disaster? Are you sure that they will continue at this school, or is it likely they’ll either drop out or transfer? This option certainly isn’t for every family, but it’s a strategy that most families don’t consider.

If your home is a bit on the smaller side, it may start to feel cramped once you get all your furnishings and decorations in. You also can’t forget to leave space open for people to walk though. There are a few solutions that can help you make the most of your space without hyper-focusing on space efficiency.

The first is a huge one — decorative storage space. This serves dual purposes by getting clutter off the ground and into a more compact area, without sacrificing aesthetic. You can find both functional and appealing furniture such as ottomans or coffee tables that feature hidden drawers to store things such as the TV remote, coasters, or a few books. Speaking of books, that doesn’t have to be the sole purpose of a bookshelf; it can be used to store any manner of items.

You shouldn’t exclusively focus on ground-level decoration, though. Decorate vertically to save room for foot traffic. These can be things such as paintings, photos, or tapestries, but they can also be functional, such as wall-mounted cabinets, or bookshelves that are tall rather than wide.

Another thing you can change to make your home feel larger doesn’t actually affect your space at all: color. Lighter colors give an illusion of airiness that can make even a small space seem less cramped. Painting every room white or beige, or even light blue or yellow, may not be the best idea unless you don’t have very many rooms. But you can still achieve the same effect by using furniture or décor in lighter colors.

Mortgage delinquency rate reached its lowest level since before the recession in June of 2021, at 4.37%. This is down from 7.6% in June of 2020, approximately a 42% decrease. The significant decrease can be attributed to both fewer new delinquencies as well as more mortgage holders catching up on payments.

That’s where the good part ends, though. A delinquency of over 90 days is considered a serious delinquency, and this category accounts for 3.2% of homeowners, or 1.55 million. This is a rather significant proportion given a total delinquency rate of 4.37%. And when forbearance programs end — which is slated to happen very soon, on September 30th — it’s likely that about two-thirds of these will still be behind on payments.

While everyone agrees the pandemic and recession were terrible events, there’s at least one good thing that came out of them: People are paying more attention to their credit. The sudden loss of jobs made consumers realize that in the event of a huge financial crisis, they’re going to be heavily reliant on credit. It also didn’t hurt that the government and media were both more focused on helping people learn to understand and utilize their credit better. As a result, the average FICO score increased by 8 points over the past year, up to 716.

There are a few ways of improving your credit score that people surely have been taking more advantage of. During lockdowns, some people had fewer expenses, allowing them to instead use their money to ensure that they made payments on time instead of letting them become late or missed payments. The stimulus bills also helped, letting people pay down existing debt in addition to not accruing additional debt. To top it off, the percent of hard credit inquiries, which temporarily decrease credit score, has decreased by 12.1%. A large part of this is because fewer new lines of credit are being opened, since a hard credit inquiry is required to open one.

Builder confidence plummeted in April 2020 after the start of the pandemic and recession. As time went on, they slowly regained confidence since demand was high. But demand was too high, and lumber prices accelerated upward, causing builders to hesitate again. Builder confidence is below the levels from the start of 2021, though higher than it was in mid-2020.

Now, lumber prices are starting to fall back down. But the reason for that is decreasing demand and rising interest rates, the exact opposite of what caused prices to rise in the first place. With demand decreasing and prices now on a downturn, builders still aren’t sure whether it’s a good or bad time to buy lumber. They’re expecting more vacancies, which means less need for new construction.

While mortgage rates are certainly not high, we can no longer safely call them low. The average rate for a 30-year fixed conforming loan is considered low when it’s below 3%. They’ve been slowly increasing. In the first half of August, it barely qualified at 2.99%. Now, the number sits at 3.06%.

As a result of increasing mortgage rates, demand for refinances has also decreased, dropping by 5% as soon as the rate passed 3%. Applications for purchase loans are less sensitive than refinance applications, and dropped only 1%. Despite the decreases in number of mortgage applications, the total dollar volume is still high, as a result of high prices fueled by heavy competition.