If you are considering purchasing rental property and also thinking of moving, one possible option is to not sell your home when you move and instead rent it out. There are various pros and cons to doing this, and whether it’s the right option for you will depend on your situation.

The most obvious benefit is that there are fewer transactions involved. You don’t need to list your home for sale and you don’t need to find rental property to purchase, though you may still be purchasing a new residence if you don’t already have somewhere else to move. You may not even need to pay an agent at all — though an agent can still be useful in guiding you to the right choices for your situation. It could also be financially better for you to simply buy once rather than buy twice and sell once. This will depend greatly on several factors, including such things as the market conditions, neighborhood, property size and condition, budget, and mortgage balance. Even if you know you can afford to buy one property, you may not be able to afford to buy two properties and pay off your current mortgage, even with the income from selling.

However, converting a primary residence to a rental property is also a process, especially if you still have a mortgage. If you purchased the property as your primary residence, that was taken into account in your interest rate. The rate is probably lower than if you purchased it as rental property. Because mortgage companies don’t want you to lock in a lower rate then immediately decide you don’t want to actually live there, your mortgage contract may have a stipulation that you must have lived there for a certain length of time to convert it to rental property. Even if you don’t have a mortgage, property taxes are also lower for primary residences. There’s no time restriction on conversions for property taxes, but the rate will change.

Most condominium buildings or planned communities have a Homeowner’s Association, or HOA. The HOA is responsible for managing all of the common areas of the community, including such things as maintenance and gardening. Typically, the HOA is composed of several residents of the community, who collect money from residents — HOA fees — in order to pay specialists for maintenance. Residents usually aren’t required to directly interact with the HOA, but since the revenues they collect benefit the entire community, all homeowners in the community are required to pay HOA fees. In exchange, most of the residents don’t have to worry about routine upkeep.

Declining to participate may prevent your vote from counting when determining where the money goes, though. Except in smaller communities, most residents aren’t on the board of HOA directors. For the most part, HOAs do care about maintaining the community and have good intentions — they probably also live there, after all. However, they may not have the same expertise or connections as you, and it’s theoretically possible that the board members are primarily absentee owners renting out the units. So if you want your voice to be heard, consider joining the board. HOAs are not strongly regulated, so how difficult it would be to get on the board could vary.

One of the statistics used to track health of the rental market is Fair Market Rent, or FMR. By the name alone, one might think FMR is a normative measure that suggests what rent prices should be. Of course, such a measurement would have to take into account construction costs and home prices, but it would also have to take into account the tenant’s income. As a renter, you may be looking for rent prices at or below FMR thinking anything above that is simply a bad deal. But is it actually fair to anyone? Is it even a normative measure at all?

The first question that needs to be answered, though, is: What really is FMR? Well, at its core, it’s a series of vague estimates. The Department of Housing and Urban Development (HUD) calculates FMR on a per-metro basis for five separate categories of homes based on number of bedrooms. Homes with more than 4 bedrooms are excluded entirely. In reality, though, only one category is actually calculated. This is the category for the average home size of 2 bedrooms. The median rent price of 2 bedroom homes, excluding outliers, is averaged over a multi-year period, then the value is multiplied by various ratios to determine FMR for homes of different bedroom counts. Note that this calculation doesn’t factor in either construction costs or income, just rent price, although the price itself generally is indirectly related to constructed costs. This means that if it’s fair to anyone at all, it can only possibly be whoever bought the home. So, no, looking for a rental at or below FMR has no bearing on whether it’s fair to the tenant.

Does FMR perhaps still have some use, though? Though it’s a multi-year average, it’s based on actual rent prices, so maybe it be used to estimate current rent values. It’s a decent assumption, but unfortunately, it’s not actually very good at estimating rent prices. If you’re looking at FMR when considering whether to move to an area, don’t be surprised if your actual rent is far different, especially for multi-bedroom homes. Multi-year averages can’t very easily take into account economic cycles, and broad examinations of metro areas can significantly skew the numbers. Another issue the calculation faces is the notion of rent control. Rent control doesn’t generally happen in an entire metro, so the prices of rent-controlled units are significantly more likely to be taken as outliers and completely dropped. Even if they aren’t dropped, they will skew the median.

For a specific example, let’s take the local area — the Los Angeles metro. This metro area is rather large, and includes multiple cities of highly varied income levels. Despite this, the FMR for the Los Angeles metro is actually lower in every single category than that of the City of Los Angeles. The LA metro FMR for a studio is $1631, quite a bit lower than than actual median rent price for a studio in Los Angeles of $2100, between mid-June and mid-December. The difference only gets larger the bigger the home. The metro’s FMR for 4 bedroom homes is $3377. But the actual median rent of a 4+ bedroom house in LA is $8995, over 2.5 times as much. Considering homes larger than 4 bedrooms to be outliers, as the FMR criteria do, doesn’t do much to help the case for FMR, as the actual median rent is still $7900. The disparity is even greater for higher income regions of the metro, such as the Beach Cities — Manhattan Beach, Hermosa Beach, Redondo Beach, and El Segundo — with a studio median of $2495 and a 4+ bedroom median of $9175. This suggests that high-income units are being excluded as outliers, which isn’t particularly useful if you’re looking to rent in a place such as Manhattan Beach.

Why is FMR lower even for smaller homes, though? Well, there may be a valid reason for that. The actual median data presented here is calculated using information from a Multiple Listing Service (MLS), which is a service used by real estate agents to upload and search listings. Because this is an agent service, only properties listed by an agent will appear in the list. For lower income rental properties, the owner is less likely to use an agent, because they may feel it’s not worth the expense with a small revenue. But the HUD can access that information, which could drag the median down for smaller homes. So, the FMR may be useful to a tenant planning to rent a low-income property. However, remember that the studio FMR isn’t directly assessed, but rather calculated as a ratio of 2-bedroom FMR, so if FMR is more consistent with real values for studio rentals, this is at least partially coincidental and could mean either the 2-bedroom FMR is low or the ratio is off. Moreover, off-market rentals do very little to explain any disparity for larger homes, and especially not such a large disparity.

City National Bank, based in Los Angeles, was accused of refusing to underwrite mortgages in predominantly Black and Latino communities. The Justice Department alleged that this occurred between the years of 2017 and 2020. They used two major pieces of evidence: First, other banks operating in the same areas with predominantly people of color received six times as many mortgage applications during this time period. Second, of the 11 branches City National opened in the past 20 years, only one was in a neighborhood with predominantly people of color, and this branch did not have a designated underwriter. While it’s theoretically possible that City National Bank simply doesn’t have many customers that are people of color, discrimination is a likely reason for that.

While City National Bank denied the Justice Department’s allegations, they seemed cooperative with the investigation. They claimed that they supported efforts to ensure equal access and readily agreed to a settlement. The terms were a $29.5 million loan subsidy fund for Black and Latino borrowers as well as an outreach campaign costing $1.75 million. The 31.25 million dollar value makes this the largest settlement ever for the Justice Department.

We’re taking a little different approach with this post. Because it’s not only the end of the month, but the end of the year, we’re doing a quick summary of the monthly data, followed by some more detailed discussion of how the individual areas have fared over the past year. We’ll even try some crystal gazing while we walk through the annual data for each neighborhood.

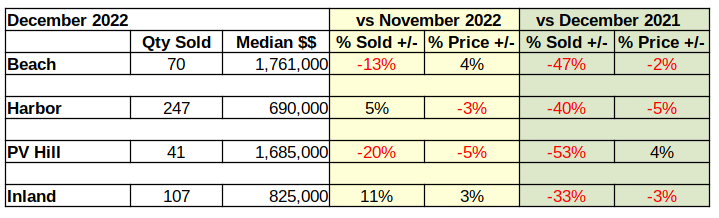

This is a great place to bring in our At A Glance table. It displays in just a few numbers how all the areas of the LA South Bay are doing compared to last month, and compared to this same month last year.

Looking at December vs November, once again the percentage of unsold homes has increased and the number of homes sold below last month’s median price has also marginally increased. More importantly, on a year over year basis the amount of red ink is even greater. Losses in number of sales and in the value of those sales is clearly growing.

Despite all the negative numbers, there may be a light in the future. For the past couple weeks we have observed a softening in the mortgage interest rates. If that turns out to be more than a mid-winter teaser rate, this spring may shine a bit brighter than previously anticipated. We’re not holding our breath though. Recent speeches from Federal Reserve Bank leaders have stated a clear intent to “hold the line” on driving down inflation with mortgage interest rate increases.

Beach Cities Home Sales Down 47%

Compared to 2021, fewer homes have been sold in the Beach Cities every month of 2022 than the same month the previous year. January started the trend with a decline of 28% versus the number of homes sold in 2021. That difference continued to increase all year. By December sales were 47% lower than the previous December.

As the interest rates climbed, the number of home sales dropped. Looking at the total sales volume for the year, 35% fewer homes were sold in the Beach area during 2022, than were sold in 2021. Of course, 2020 and 2021 were the highly erratic pandemic years. So, looking into sales at the Beach for the last few years we find the number of homes sold has already dropped 21% below the number sold during 2019, our last normal economic year. Effectively, the Covid-19 pandemic created. Then erased any gains of the past three years at the Beach.

Homes sold in: 2019 – 1572 (market normal) 2020 – 1572 (market direction down six months, up six months) 2021 – 1910 (market direction down two months, up ten months) 2022 – 1242 (market direction down twelve months)

While the Beach Cities suffered the largest drop in sales volume for 2022, the South Bay as a whole has also dropped below the sales figures for 2019.

Sales Volume Down Across the Board

All areas started the 2022 year down from the prior month and down from the same month in the prior year. February results were mixed with the Harbor and Palos Verdes areas showing stronger results. March sales jumped up as buyers realized the rising interest rates were about to price them out of the market. From April on, sales volume across the South Bay was trending down on a year over year basis.

In sheer number of sales, the Harbor area fell the farthest. In 2021 annual sales 5292 homes were sold in the Harbor cities, while in 2022 the number dropped to 4017. That amounted to only a 24% decrease compared to the 35% annual collapse in the Beach areas.

On a month to prior month measure, sales declined six months out of nine across the South Bay. Occasionally one or two areas would post a positive sales month, but in the end, 2022 showed a 26% drop in sales volume from 2021 across the South Bay.

Sales Dollars Diving

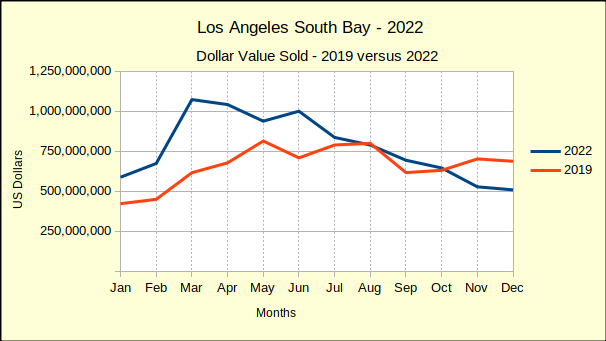

With the number of sales dropping in a range of 25% to 50% it’s not a surprise to discover the total dollar value of those sales has taken a dive. As the chart below shows, the first quarter of the year was generally positive, then reality set in and the buyers started walking away. The rest of the year was little more than a measure of the recession.

Monthly revenue in the Harbor area alone dropped $200 million between March and December. The Beach cities and the Palos Verdes area lost about $150 million a month in sales value. Inland area sales for the same period are off approximately $75 million.

One should consider these declines in the context of the pandemic. Early on, while much of the world was in lockdown, the government flooded the citizenry with easy money, hoping to keep the economy afloat. Mortgage interest rates were already at the bottom because the economy was just recovering from the last recession. The result was a real estate boom starting in summer of 2021, which continued until March of 2022.

The housing market is now in the “bust” part of the cycle and we anticipate it to last through 2023. Gross sales across the South Bay jumped up from $8 billion in 2019 to $12 billion in 2021. That’s clearly unsustainable, especially from the perspective of a Federal Reserve System which is looking for 2% growth. So far the market decline has taken back about 23% of that $4 billion bubble.

Median Price Is Slipping

There is a lull between when buyers stop buying and prices start dropping. Most sellers need to see headlines about the market change before they make a price reduction. Median prices started to slide in August at the Beach and on PV Hill. The year ended with most areas having experienced multiple monthly declines in the median price. Despite that, median prices still exceeded those of 2021 by roughly 7%.

Comparing 2022 to 2019 better shows the inflation factor. Generally speaking the South Bay ended the year with median prices 30%-35% higher than they were in 2019.

The Palos Verdes market is comparatively small, thus is typically volatile on a monthly basis. The yellow line on the chart above shows the range of high and low median prices. Since mid-year the median price has drifted down and merged into the downward trend.

Year End Versus 2019

We’ve been comparing 2022 to 2019 all year because real estate sales during the height of the pandemic were so out of the ordinary, regular year over year comparisons yielded untenable results. The chart below depicts the current year total sales for the South Bay compared to sales from 2019.

Tracking the blue line, one can see where sales dropped below 2019 values in August, recovered in September, then slipped below again for the fourth quarter of the year. December sales didn’t fall quite as far as projected, but still came in about $200 million less than December of 2019.

The end of the year reflected accumulated sales of approximately $9.3 billion. That would mean 2022 total dollar sales come in at $1.3 billion above the $8 billion total dollar value sold in 2019. Across the South Bay that was an 18% increase.

Broken out by community, we found total dollars sold in the Beach cities to be 4% above 2019, followed by the Inland area with a 20% increase. Harbor came in next with a 21% increase and the PV Hill with a 35% increase.

We expect both sales volume and median price to continue declining through most, if not all, of 2023. By mid-year of 2024 there should be evidence of the beginnings of a recovery.

Disclosures:

The areas are: Beach: includes the cities of El Segundo, Manhattan Beach, Hermosa Beach and Redondo Beach; PV Hill: includes the cities of Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills and Rolling Hills Estates; Harbor: includes the cities of San Pedro, Long Beach, Wilmington, Harbor City and Carson; Inland: includes the cities of Torrance, Gardena and Lomita.

Data from December 2022 shows us that home prices in California are unquestionably going back down. December 2022’s median home price of $774,580 was just barely below November 2022’s median price, only by 0.4%. This isn’t necessarily a trend, but what is a trend is that it’s 2.8% below prices at the end of 2021. Home prices are down in every major region of California, and across both single-family residences and condos. However, all regions except for the San Francisco Bay Area had at least one county experience price growth.

The far northern regions of California had the most notable shifts. Year-over-year, prices are down a whopping 41.8% in Lassen County. Granted, this isn’t a massive dollar value given that Lassen County is the least expensive county in the state, with a median home price of just $170,000 in December 2022. Even so, it was actually the third cheapest at the end of 2021 — both Del Norte County and Siskiyou County were cheaper in December 2021, but both actually experienced price growth this past year. In fact, Del Norte was the county that had the most significant price growth at 13.8%. Del Norte and Siskiyou counties both border Oregon, and Lassen County is just south of Modoc County, which also borders Oregon but is not included in the rankings.

Forbes has compiled a list of its top 10 California cities to live in, aggregating data from various different sources. Their methodology includes comparisons of population, median home price, cost of living, personal income per capita, unemployment, community well-being, and crime rate. The community well-being score is itself an aggregate score taken from the ShareCare Community Well-Being Index. Note that all of the criteria used by Forbes are objective measures focused on health and economic stability; they do not factor in self-reported happiness of residents. According to Forbes, the top 10 California cities to live in are Sacramento, San Diego, San Francisco, Los Angeles, San Jose, Vallejo, Oxnard, Modesto, Fresno, and Bakersfield.

It’s unclear whether Forbes considers high or low population to be preferable, but the measurement is still useful in calculating crime rate, which Forbes provides in raw numbers as opposed to in proportion to population. Forbes is also only reporting on violent crime; nonviolent crime is far more common. California has a rather high violent crime rate in general compared to the US average of approximately 0.4%. But San Diego, the #2 city in Forbes’ list, has a violent crime rate lower than the national average at 0.38%. The city with the lowest median home price is #10 on the list, Bakersfield, whose other primary attraction is also one of its most detested qualities — it’s a major business hub, and therefore also a major traffic hub. Interestingly, the top city, Sacramento, holds a rather middle-of-the-road position in all categories, instead of being particularly strong or weak in any one area.

Wells Fargo is one of the biggest banks in the nation as well as one of the top mortgage lenders. In fact, it was the number 1 mortgage lender in 2019. However, that’s about to change. 2019 was also the year that Wells Fargo acquired a new CEO, Charlie Scharf, who inherited a company under strict scrutiny as a result of a 2016 fake account scandal. Among the changes Scharf is making is a massive shift away from mortgage lending to focus mainly on investment banking and credit cards.

According to Wells Fargo exec Kleber Santos, investigations into the 2016 scandal also revealed that their mortgage lending business was simply too large in scope. The implication is that it was too difficult to manage oversight of all the facets of the company, and that mortgage lending was the one that needed to be trimmed down. Wells Fargo will not be completely eliminating its mortgage lending business, but it will be cut down dramatically to prioritize existing customers and borrowers in minority groups.

When prices are changing rapidly — whether they’re going up or down — there’s always a risk of appraisers not being able to catch up. Most of the data available to appraisers is at least a week old, usually a few weeks. Most of the time, this is good enough, but not when price fluctuations are happening quicker than that. It’s expected that prices will be dropping rapidly throughout 2023 and 2024, which increases the risk of overappraisal. This is especially harmful to buyers who may end up paying more than the home’s actual value, immediately falling into negative equity. Lenders also want to avoid this, since they can incur losses when lending to a buyer who is suddenly in debt.

It’s not an issue that can be eliminated entirely, but luckily, there’s a way to at least mitigate it. In 2007, Fannie Mae encouraged appraisers to start including an assessment of the current market direction. Since 2009, oversight for appraisals is not handled by Fannie Mae but rather by appraisal management companies, but its still good advice. It means that even if the appraisal is off by a bit, involved parties will know in what direction the error is likely to be and can plan accordingly. Fannie Mae suggests that the assessment be limited to the neighborhood of the property in question and include data on recent price changes, average days-on-market, and inventory.

Home sales volume tends to follow a similar seasonal pattern each year. It most often peaks in the middle of the year, falls off rapidly once winter arrives, and is at its lowest point the following January before restarting the cycle. The pandemic didn’t completely upset the pattern, but there were some noticeable shifts.

2020 could actually be described as having two cycles — one in the first quarter and one during the rest of the year. The first cycle peaked just before lockdowns in March, while the seasonal variance was on its upswing, before crashing down to the lowest point of the year in May. The peak of the second cycle was towards the end of the year. Home sales predictably shot up as the year entered June, but then continued their slight upward progression. The second cycle did reach bottom in January, as expected, but the low was significantly higher than prior years, as pent-up demand was still high.

The first half of 2021 seemed fairly normal. Home sales volume increased fairly steadily until the summer months. The peak was higher than normal, likely for the same reason the year started at a higher point. But the decline in the latter half of the year was quite a bit sharper than usual. The trough in January was lower than that in the beginning of the year, despite coming down from a higher point.

The shape of 2022 was rather odd. Like 2020, the peak was actually in March. But this time, it wasn’t because of a pandemic. It was the realization that we’re at the start of a downward cycle in the housing market overall. There was no steep increase just before June; it just continued to decline, though there was a minor upward bump later in the summer. The data is not yet available for December or January, but considering November’s home sales volume was already lower than the trough in January 2019 — the most recent trough of a normal cycle as well as the lowest value during a normal cycle in the past decade — and sales are continuing to decline, one can expect the numbers will be quite low.

If you’re just looking at the raw numbers, California looks pretty good as far as homeowners living free and clear, that is, having paid off their mortgage or never having had one. 2.4 million households belong to this category, third in the nation, just below Texas at 2.9 million and Florida and 2.5 million, and followed by New York at 1.7 million and Pennsylvania and 1.5 million.

This sounds great, until you realize that the top five most populous states are — you guessed it — California, Texas, Florida, New York, and Pennsylvania. While there are a lot of people living free and clear in California, as far as percentage of homeowners, it’s near the bottom of the barrel at just 32%. Only four states are faring worse, Colorado and Utah at 30%, Maryland at 28%, and D.C. at 24%. The top five states for share of free and clear homeowners are West Virginia at 53%, Mississippi at 51%, North Dakota and New Mexico at 47%, and Louisiana at 46%. However, Louisiana is the only one of these states in the top 25 of population. Compared to California, both Texas and Florida are actually doing very well, ranked at number 11 and 12 respectively in share of free and clear homeowners.

Financial technology company SmartAsset has used federal and local data to compile a list of what they consider the happiest cities in the US. SmartAsset ranked the largest 165 cities according to 13 different metrics, focusing on personal finance, well-being, and quality of life. Among the top 50 cities, 17 of them are in California, just slightly over a third.

Not only that, but California actually boasts the city with the number 1 spot, Sunnyvale. Five other California cities are in the top 10; these are Fremont at #4, Roseville at #7, San Jose at #8, Santa Clarita at #9, and Irvine at #10. Of course, since these are aggregate scores, the cities in the top 50 don’t necessarily perform well in every category. For example, even though Hayward, CA is ranked a rather respectable #17, it ranks among the lowest in finance related categories. The four top 10 cities not in California are Arlington, VA at #2; Bellevue, WA at #3; Frisco, TX at #5; and Plano, TX at #6.

A build-to-rent community is a community in which single-family homes are build solely for the purpose of renting them out. It isn’t a new concept, but it’s been under the radar for quite some time, comprising only 3% of the single-family residence (SFR) market. As just one of many changes in the type of demand brought in the wake of the pandemic, that number is now up to 12%.

Many people who transitioned to work-from-home needed more space for a home office. That meant looking for a larger home. For renters, that often wasn’t possible, since they were priced out of the homebuying market. But what if they could rent the type of home people normally would buy? In a build-to-rent community, they can. The SFRs in such communities have significantly more space than apartment units, and while they are certainly more expensive to rent than apartment units, rising home prices meant renters definitely couldn’t buy if they weren’t able to before. It’s definitely possible to find SFRs that are not in a build-to-rent community, but looking for such a community guarantees it, and also comes with community amenities.

According to a report from real estate brokerage Redfin, the share of home sales that were paid fully in cash reached 31.9% as of October 2022. This is the highest value since 2014. It’s been steadily increasing since April 2020 when it immediately plummeted down to 20.1% due to lockdowns, a record low. At the time, the general trend was downward, though the share of cash sales went up and down in cycles, and continues to do so. Now, the trendline is going back up.

There are actually a couple of different reasons for the shift, depending when you’re talking about. After the lockdowns, mortgage rates had a period of extreme lows, followed by extreme highs after federal intervention. Finally interest rates are starting to fall back down, but throughout all of this, the cash sale share was still trending generally upwards, albeit with some dips as usual. It’s not that mortgage rates don’t influence share of cash sales. They can actually influence it quite a bit, but at least since the pandemic, in the same direction for either extreme. In the first year since the pandemic, cash sale share shot up rapidly because low interest rates increased demand, which in turn increased the attractiveness of cash offers. Once interest rates skyrocketed during a time of already high prices, lower-income earners were effectively kicked out of the running entirely. This left wealthy buyers who, of course, didn’t want a high interest rate mortgage if they could avoid it, so they paid cash because they had the means to do so and it was the best financial decision for them.

The California Department of Insurance (CDI) has provided the latest update to their resources on the effect of wildfires on insurance. Statewide data on policy counts is now available for 2021, and county-level and zip code-level multi-year data has been updated to 2021, going back to 2015. You can also view archives of older statewide data up to 2015. In addition to policy counts, the CDI has compiled updated info on coverage limits, premiums, losses, and claims.

Also available are additional resources for those wanting to know their wildfire risk or looking for insurance. A report with a large amount of data, including but not limited to coverage amounts and losses for each zip code, is available for download under the “SB 824 Wildfire Risk Information” header of the CDI’s Rate Filings page. This data is from 2018-2019. There is also a list of insurance companies offering incentives for wildfire safety, last updated in November, as well as a searchable list of insurance companies and real estate agents that work with high-risk areas.

When the lockdowns hit, homeowners very quickly realized what their homes were lacking in terms of comfortably getting through the lockdown period. The result was a shift in which home features were most in demand. People began to favor more outdoor space so they weren’t stuck inside, home amenities, and variable living space, among other things. While the virus certainly hasn’t disappeared, lockdowns are no longer in effect, masks are no longer mandatory in most cases, and people are gathering together more. But the lockdown-era trend shifts continue to be apparent.

Backyards are a popular feature, with 22% of listings highlighting them. Patios and pools are also the focus of an increasing amount of marketing, with 13% of listings mentioning patios and 11% calling attention to the pool. Home gyms are also increasing in popularity. Of course, this doesn’t prove that buyers want more outdoor space and home amenities, but it does say that’s what agents think buyers are looking for. The same is true of multipurpose spaces. The ideal kitchen now includes a kitchen island, which has the flexibility to be used as a dining area, workspace, or entertainment table. It’s even extending to the way the home is organized — open-concept living had been popular for a while, but it’s now fallen out of favor as people realized they had no private or quiet spaces with everyone at home at the same time. The motivation for this shift is no longer present, but the experience seems to have changed peoples’ minds about open-concept living.

In the last 80 years, a particular species of salmon, the Chinook salmon, has not been found in the wild in one of its previously most important areas, the McCloud River in northern California. The Chinook salmon has been endangered since 1994, possibly as a result of dam construction, but it’s gotten worse in recent years. They’re also dying off in the Sacramento River, which is becoming too warm for many young salmon to survive. Now, a joint conservation effort between the State of California, the federal government, and the Winnemem Wintu Tribe of Native Americans is looking to reintroduce Chinook salmon to the McCloud River.

There isn’t anything wrong with the McCloud River itself. It’s still a good spawning point for Chinook salmon, even with climate change threatening young salmon in the Sacramento River. The problem is that they can’t actually get out because of the dams. This new conservation effort seeks to aid them with human intervention. They transported 40,000 Chinook salmon eggs to the McCloud River and measured how many spawned. About 90% of the eggs hatched. The next step was to help them along their migratory route when it came time. In order to do this, they’ve recaptured the salmon along their migration, bypassed the upper Sacramento River, and redeposited them in the lower Sacramento River. This has been successful, but the next step is still a work in progress. The group hasn’t quite decided the optimal way to get the adult salmon to return. Options include an additional recapture and redeposit, the construction of a fish ladder, or the demolition of some dams. The first two options would use a route across the Shasta Dam, while the last would involve smaller dams and a new route.

In recent years, a few states have created laws regarding pay transparency in an effort to reduce discriminatory wage gaps. Colorado was the first to introduce a statewide law in 2019, though it didn’t take effect until 2021. New York City’s law will soon expand to all of New York. A new law just took effect in Washington as well as our own state, California, on January 1st. California’s law requires that companies with at least 15 employees post pay ranges in their job listings, as well as requiring that current employees have access to the pay range for their current position. The penalty for violating this requirement is between $100 and $10,000 per violation. The first violation only gets a warning as long as the information is added. Some companies also don’t currently have pay bands — the new law requires them. Companies with at least 100 employees will need to provide more detailed information.

Unfortunately, the new law may have to contend with some resistance. In New York City, employers chose to display incredibly wide price ranges. This doesn’t help prospective employees at all to figure out how much they would actually be getting. In one extreme example, Citigroup claimed a range of $0-$2 million, though they later said this was a computer glitch and changed it to something more reasonable. In Colorado, employers created remote job openings — with the stipulation that they could not be in Colorado, so the state requirement didn’t apply to that listing. Colorado’s method probably wouldn’t work in California, since California has such a large population that employers would miss out on a huge segment of potential employees. But New York City’s method is actually already in use in California, even without a requirement to list pay ranges at all. This is because prospective employees tend to disregard a listing entirely if there’s no pay range provided.