The day of the month that you close on the purchase of your home is important and should be part of your contract negotiations. Whether you want to close early or late in the month depends whether you want to save money or ensure the process goes smoothly.

Mortgage interest is paid in arrears. The amount of prorated interest that you will pay at closing will be determined by the day of the month you close. A later date in the month means less interest paid as part of your closing costs. For example, if you were to close on May 30, then you would only pay two days of interest plus the interest due for June. Your first payment wouldn’t be due until July 1.

Because of these savings, 95% of closings occur at the end of the month. What this also means is that title and escrow companies are not as busy near the beginning of the month, and the closing process tends to go a bit more smoothly.

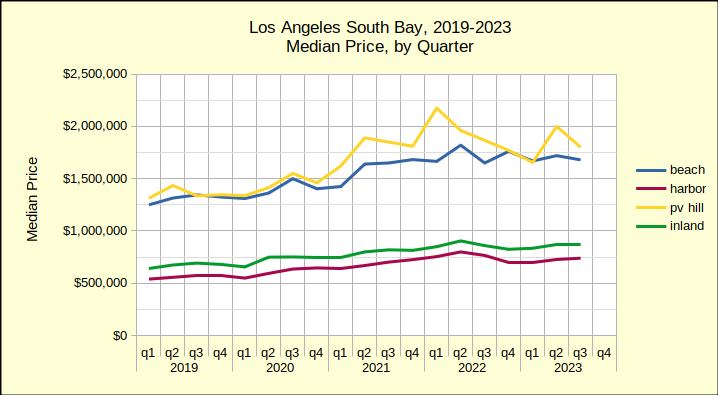

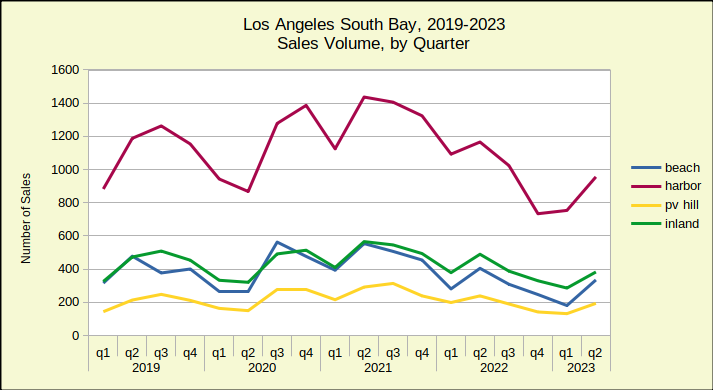

After a big 7% dive in October sales, annual real estate sales flattened out in November. Compared to November of 2024, the numbers are showing zero change for the Los Angeles South Bay. Sales were mixed across the areas. Median prices were mostly increased, though modestly compared to early in the year.

Downward pressure has increased in both sales and prices from month to month throughout the year. While 2025 continues to exceed 2024 in all metrics for all areas, the margin has grown smaller continually. Anecdotally, the real estate market has been slow and is slowing. This time of year slower sales are expected, though the seasonal slowdown this year seems to be a bit faster than usual. Median prices are not necessarily affected by the season, so the shift in pricing is one more indicator of a slowing real estate market.

Even two decreases in the prime rate by the Federal Reserve has done nothing to help. The most recent drop of .25% actually saw a .125% increase in the mortgage rate the next day.

In a couple weeks the year will be closing out and 2025 will become history. We’ll get the annual wrap-up out to you with a forecast for 2026 as early in January as possible. Enjoy your holidays!

Beach:

The number of homes sold in November in the Beach area plummeted in comparison to October. Sales dropped 30%, coming in at a mere 81 units. At the same time, the median price dropped to $1,750,000 to register an 8% decline. This is the sixth time this year Beach Cities sales have fallen compared to the prior month, and the eighth time the median prices have done likewise.

November of this year compared to November of 2024 showed mixed results. The volume of sales dropped 2%, while the median price rose 6%. This is the third month in a row annual sales have declined at the Beach. The annual median started in January at 32% increase, and has steadily dropped, falling below 0% four separate months.

With only one month remaining, the year to date numbers show a strong 12% growth in sales and 6% increase in the median price. The sales volume remains 17% below the number of homes sold during the same period in 2019. The median price at the end of November was higher than that of 2019 by 45%, significantly above the Federal Reserve System’s ideal of 2% inflation per annum.

Harbor:

November real estate was good for the Harbor area. At 262 homes, monthly sales volume looked horrible–down 19%–but that seemed really good next to the South Bay wide drop of 23% in home sales. A median price of $812,000, an increase of 3% above October figures, was impressive compared to an approximate drop of 6% in most of the South Bay.

On an annual basis, this November came in with a modest 2% increase over last year. Again, this was a marked improvement over the 0% increase of the South Bay as a whole. Year over year median price was the only market statistic for November home sales the Harbor area didn’t dominate. Both the Beach and the Hill areas showed greater increases, at 6% and 10%, respectively.

Year to date, the Harbor area gives a classic display of capital growth, with a 2% increase in sales volume and a matching 2% increase in median price. Sales have fallen to 21% below 2019 levels, while the median price remains at 40% above 2019.

Hill:

Like the Harbor area, the Palos Verdes peninsula slipped in the number of homes sold compared to last month. With only 45 properties sold in November, the Hill dropped 18% in sales. The median price of $1,990,000 gave an 8% increase over the October median sales price.

Year over year, November residential sales rose 13% above 2024. This was the highest increase in sales volume of the four areas, far exceeding the total South Bay number, which was 0% growth. The Hill also came in with the greatest median price, jumping by 10%.

Looking at the combined activity of January through November, compared to the same period last year, sales volume was up 7%. Median price for the period was up by 1%. Compared to pre-pandemic statistics from 2019, PV home sales were down by 15% year to date, and the median price was up 45%.

Inland:

For November the Inland area dropped in all four metrics, sales volume and median price, for month over month and year over year. The number of homes sold dropped 28% on 102 units. The median price fell 6% to $865,000.

Annually, volume fell 8%, the steepest decline in the South Bay. Compared to last November, the median price was off by 3%.

Year to date remained in positive territory with 0% change in number of sales and a 1% increase in median price. Sales volume continues to be off from 2019, showing a 19% decline. Median price compared to pre-pandemic pricing remains up by 33%.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

When a buyer makes an offer on a home where the proceeds from the sale would be less than the seller owes on the loan, this is called a short sale. At this stage, only the agreement between the buyer and seller is involved. However, in order for a short sale to close, the lender must also approve it.

The seller’s agent takes a short sale package to the lender for review and approval. The package includes the purchase contract, a hardship letter explaining why the seller can’t keep the home, and any market conditions that create the need for a short sale.

The lender will analyze the short sale request and determine how accepting less than what is owed affects their bottom line. The lender may come back with a letter stating the specific terms and contingencies that must be incorporated into the deal in order to release the lien and close. The sale will be “approved for short sale” if the buyer and seller can meet those specified terms.

Some people sell their houses before buying others, giving them clear budgets for their next places. It makes financial sense, but there’s the risk that you might end up couch surfing or having to rent somewhere in the meantime. Others buy first, locking in their dream homes before they’re snatched up, but that can mean carrying two mortgages at once. So is there a way to eliminate both issues, by both buying and selling simultaneously?

Absolutely. It will take some planning and help from an agent, but you can definitely buy and sell at the same time. The key is timing. Your agent will help align your sale with your purchase. You may have to negotiate a rent-back deal or a flexible closing date. It’s also smart to get preapproved for a mortgage early so you know what’s realistic. And if you need a financial cushion, options like bridge loans or home equity lines of credit can help you cover gaps between buying and selling. It’s something that requires both planning and flexibility on the part of both you and your agent, but it’s certainly a viable option. As an added bonus, it’s also faster than finishing out two separate deals.

A promissory note is a legal document that will be created if there is a loan being obtained as part of the purchase of real property. The written note is designed to enforce a borrower’s promise to pay back a lender. The payor agrees to pay a certain amount of money to a payee in the future on a specified date. The note must spell out the name of the payor and the payee, and it must be signed by the payor.

It does not have to be notarized, but to be enforceable, a promissory note must contain an unconditional promise to pay a sum of money under specified terms and conditions of repayment. The note must also include an absolute date for payment. A concise promissory note will also include an interest rate and describe the collateral being used to secure the note.

In a normal year, the interest rate for a conventional mortgage loan would be lower than the rate quoted for a “high balance” loan, which would be slightly lower than a “jumbo” mortgage. (Here in Los Angeles jumbo is more common than not.) The theory behind the differing rates is one of risk management. Lenders generally consider larger loans to be more risky, thus jumbo costs more.

Guess what! It’s not a normal year. It’s a Presidential Election Year. In addition to the political strife, our nation is closely involved in a couple of economy-disrupting wars in other parts of the globe.

The end result is jumbo loans with fixed interest rates that are as low or lower than conventional loans. Despite headlines touting strength in the economy, interest rates have increased by approximately .5% since the first of the year. The most recent announcements from the Federal Reserve System are hinting that anticipated rate reductions aren’t happening at all in the first half of 2024, and the number of potential reductions is expected to be less than previously expected.

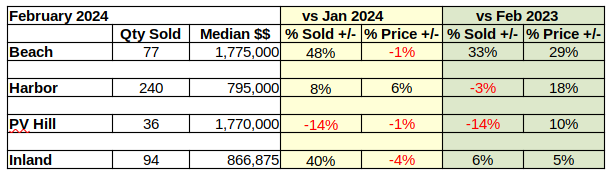

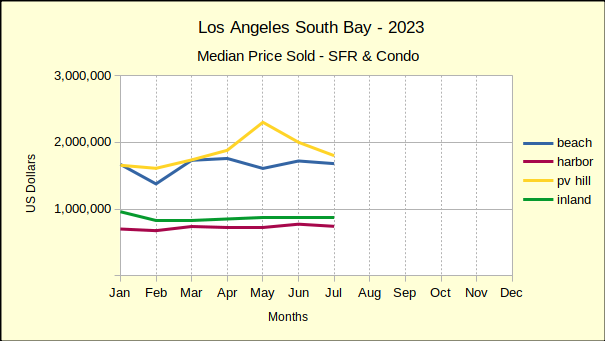

Last year saw median prices in the South Bay falling below 2022 prices through July. In August of last year price declines began to abate. By December of 2023 prices had started to stabilize. The new year continued that trend with only one negative median price result in January. Improving on that, February showed solid growth in prices across the South Bay. The real estate market seems to be reacting to what is touted as an improving economy.

However, compared to last February, sales volume this February was a mixed bag with overall positive growth of 2% despite declines of 3% in the Harbor area and 14% on the Hill. These weaker sales figures follow a strong growth in the number of homes sold in January versus the same month in 2023.

Recent month to month history has shown that a decline in sales volume is typically followed by a decline in median price. This “tit for tat” resonance indicates a market where buyers are at the edge of their ability to buy and sellers are feeling the resistance. Indeed, following the upward movement of mortgage interest rate activity for the first two months of the year leads to the conclusion sales volume will drop, followed by more substantial price decreases in coming months.

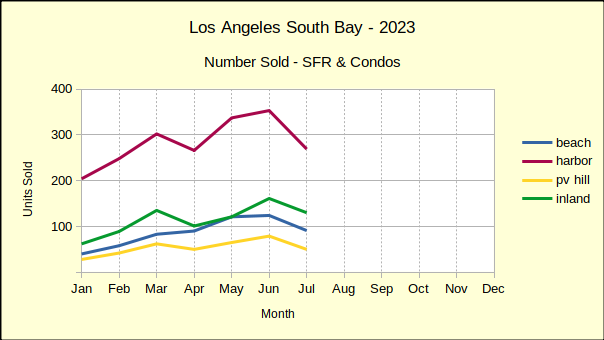

Beach: Sales and Prices SeeSaw

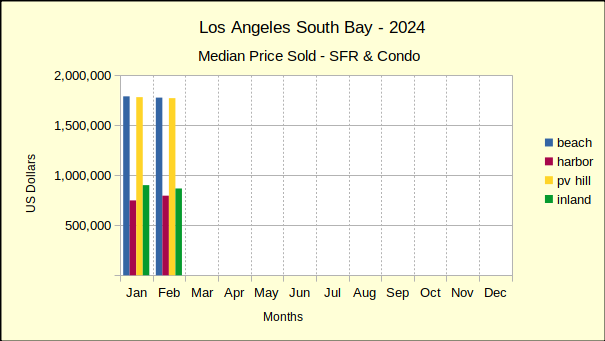

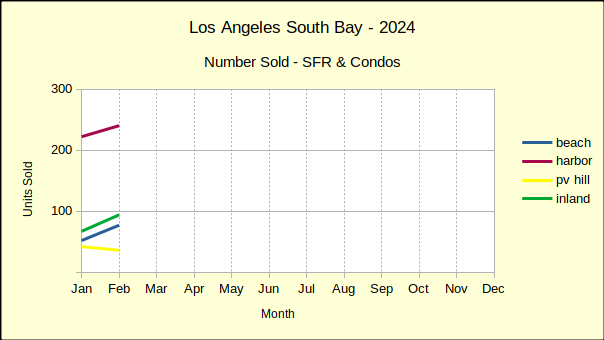

On a month to month basis, the Beach area has seen serious ups and downs in the number of homes sold and in the median sales price. January started with a massive 46% drop in sales from December, then February showed up with a 48% increase in sales volume. By way of contrast, Palos Verdes sales were down 16% and down 14% for the same months. The median price for Beach homes slipped 1% in February versus a 13% increase in January.

February sales volume versus February of 2023 was also steeply higher at 33%, the largest increase of the South Bay areas. At $1.175M the median price was up 29% over the same month last year. This is a somewhat surprising median price increase in light of other annual increases around the South Bay falling in the range of 5-18%.

Looking at year to date for the first two months of 2024, the Beach area had positive sales volume of 32% with a median price increase of 17%.

Harbor: More Up and Down

Responding to the volatility of the economy, the Harbor area flipped from negative numbers in January to positive in February. The number of homes sold was up by 8% over the prior month, while the median price of those homes increased 6%. The largest of the South Bay areas, the Harbor area typically has less variability in both sales and prices than the other areas.

Annual figures, looking at change from one year to the next in the same month, is usually a predictor of long term direction. February home sales in the Harbor area seem to be close to the bottom of market. Volume dropped by 3% from 2023, the smallest annual decline since the end of the pandemic.

At the same time, the median price rose 18% above that of February 2023. It should be noted that the median price in the Harbor last February was exceptionally low at $675K. In contrast, the $795K for this year appears to be on the high side and should be expected to moderate as the year goes on.

Year to date, the number of homes sold has increased by 2% over 2023. The median price has gone up 12%.

Hill: Numbers Continue to Fall

Real estate on the Palos Verdes Peninsula was off more this month than last. Month to month sales volume dropped by 14%. Median price, which was flat last month, has fallen by 1% this month. This kind of back and forth jockeying in price and volume looks jerky in the month to month statistics.

When viewed against the backdrop of annual data one can more readily see the direction. Annually, residential sales dropped by 14%, roughly the average of the past few months. While sales volume was dropping, the annual median price rose a surprising 10%.

Combining January and February for year over year numbers shows the number of homes sold increasing by 11% and the median price increasing by 9%

Inland: A Mixed Bag for Sales and Prices

Like the Beach cities, the Inland area enjoyed a huge surge in the number of homes sold for February, after suffering a large drop in sales January. Volume was up by 40% for the month. Median price dropped 4% after an 11% jump last month. So far this year the market has been very unpredictable.

As mentioned early, the “same month, last year” perspective is starting to level out. Residential sales volume for February of 2024 increased by 6% compared to 2023. The median price was up 5% over for the same period. The annual percentage of change seems almost stable by comparison the the monthly.

Year to date, Inland sales have increased 7% while the median price has declined by 1%. So far in 2024, only the Inland median price has declined from the first two months of last year.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

You may have received a loan payment notice from a company you don’t recognize or you know you haven’t taken a loan from. That doesn’t necessarily mean it’s a scam, but it could be. Loan servicing is a real thing, whereby lenders outsource their payment collection to a loan servicing company. In addition, lenders can and do sell their loans to other companies, or companies could merge or get bought out. These are all legitimate reasons you could get a notice from an unfamiliar company.

Unfortunately, scammers are aware of all these methods, and attempt to convince you that what’s happening is legitimate. So, if you notice any deviation, you should always check to make sure it’s real. If the lender’s policy changes or the company is sold, you should receive a letter notifying you of this before any new collections occur. Beware that this process could be disrupted by improper transfer of records or collection dates coinciding closely with the change. Make sure to communicate directly with your lender, not the company that is collecting, until you are sure that it’s legitimate.

There’s a strong tendency to want to pay off your mortgage as quickly as possible. There’s also a strong reason for lenders to not want you to do that — they get less money because you aren’t paying as much in interest. Because of this, they frequently use prepayment penalties. This is an extra fee for paying off your mortgage too quickly or before the term of the loan ends. If you’re simply paying the minimum amount anyway, this won’t affect you, but if you think you may want to pay off your loan early, you’ll want to know your options.

Different states have different laws regarding prepayment penalties, and some don’t allow them at all. In states where they are allowed, they come in two types: hard prepayment penalties, which are fixed fees regardless of the reason for prepayment and that are usually a percentage of the loan amount, and soft prepayment penalties, which are only charged if the borrower pays a large amount in a short time period. Even in states that allow prepayment penalties, not all loans will have them, and you may be able to negotiate with your lender for their removal. When shopping for loans, make sure to read all the terms of the agreement, and talk to a legal professional if there’s anything you don’t understand or want to learn how to negotiate.

You might think lenders would need to do a bunch of fancy calculations to determine how much money you can borrow. There are certainly several factors that go into the final calculation, but if you want a rough estimate, it’s actually relatively simple. Lenders tend to use one of two formulas, either mortgage payment as a percentage of gross monthly income, or debt to income ratio.

Both of these factors involve your gross monthly income — that is, the amount you were paid before deductions from social security and taxes and before making any payments or contributing to savings. Where they differ is what your gross monthly income is compared against. The first method calculates what your monthly mortgage payment would be based on actual interest rate and ensures that it doesn’t exceed 28% of your gross monthly income. The debt to income ratio method compares your gross monthly income against your debts, such as credit card debt and other loans. These existing debts plus your new loan payments should not exceed 36% of your gross monthly income. Both these methods do require knowing the interest rate, which is determined by several factors, but if you know about where interest rates are, you can make an educated guess.

Every month we compare the level of home sales from the preceding month to the same month of the preceding year. For example, November of 2023 is compared to November of 2022 to determine whether the number of homes being sold is growing or shrinking. The year over year number of homes sold across the South Bay has been shrinking every month since October of 2021–until now. November of 2023 marked the first time since October of 2021 where the number of homes sold increased over the same month in the prior year.

Lest we become overly enthusiastic, we need to remember that at this time last year successful sales figures were plummeting, Closed escrows were shrinking at up to 50% below the prior year in fall of 2022. So a positive value could only mean we’re bouncing along the bottom.

Also on the positive side, there is some improvement in median price which has been shrinking most of this year. At least as of November, it’s looking like “scattered improvement” in the South Bay real estate market.

Beach: Home Sales Pull Out of Dive

After two successive months of declining sales volume and falling median prices November real estate activity brought positive news to the Beach Cities. Last month saw a 9% jump in sales volume over October, and a 4% increase in the median price. The number of homes sold climbed from 79 last month to 86 in November. Concurrently, the median price gained nearly $70K.

The downside was a 3% drop of the median price versus November of 2022. The sold median for last November was $1.700M compared to $1.656M this year. The year over year sales volume gained 8% with 86 sales versus last years 80 transactions.

Year to date remains in red ink with sales down 14% January through November. For the same time period, the median price has fallen by 2%.

Harbor: Volume and Prices Turn Upward

Compared to November of 2022, both sales volume and median price climbed by 7% last month. This is the second month of solid upward figures for residential home sales in the Harbor area. Sales figures for the area have been in red ink since the beginning of the year, so these are welcome statistics for home owners wishing to sell.

On a monthly basis, the number of homes sold in the Harbor area fell by 6%, dropping from 267 in October to 252 in November. despite a median price increase of 1%.

Looking at the longer term, median price for the first 11 months of the year has fallen from $756K in 2022 to $740K, for a decline of 2% in the year to date median price. Sales volume for the same 11 months went from 3,770 in 2022 to 3,076 this year, a decrease of 18%.

Hill: Sales Volume Down, Prices Up

Comparing November of 2023 to November from last year shows a 10% drop in sales from 51 units in 2022 to 46 units this year. Despite the decline in number of sales, the median price for November climbed 19%, going from $1.77M in 2022 to $1.94M this year.

Monthly changes to the median price are much smaller and have been getting smaller as the year progresses. The November decrease was 1%, having dropped from $1.96M to $1.94M. The median price has varied monthly throughout the year. It ranged from a high of $2.3M in May of this year and fell as low as $1.6M in February. Year to date the median for the Hill is up 1% from 2022.

After having risen in September by 14% and in October by 13%, the number of homes sold on the Hill fell by 27% in November. Of course, part of the decline is seasonal. However, month to month sales volume for the first 11 months of 2023 was off by 19% in Palos Verdes with a similar drop of 16% overall for the South Bay.

Inland: Median Price Up from 2022

November 2023 was a good month for the Inland area compared to the same month last year. The number of homes sold climbed 11%, from 96 sold last year to 107 this year. Median price turned upward by 6%, ending the month at $851K, changed from $800K in 2022.

Compared to October of this year, Inland homes sales fell 8%, dropping from 116 homes to 107. That rate of change was slightly higher than the 6% drop across the South Bay. Median prices fell 7% for the month.

Year to date, the Inland area sales volume is off by 12% while the median price is up 1% from the same period in 2022.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

A mortgage buydown is an option to pay an extra upfront fee to reduce your mortgage interest rate. They come in two types: permanent or temporary. Permanent mortgage buydowns last for the entire length of the loan, resulting in decreased interest expenses at the cost of an upfront fee. Temporary buydowns last for a specified length of time, and typically are gradually phased out over the course of the buydown period. However, it’s possible for the upfront fee of a temporary buydown to exceed the interest reduction.

The decision of whether to take a permanent buydown or no buydown is relatively simple and only depends on whether you think you can afford the upfront payment. The decision of whether to take a temporary buydown or not is more complex. At first glance, those with a higher upfront fee than interest reduction can seem like a scam — paying more now in order to pay more over the course of the loan? Seems like a terrible idea. And it would be, if it were you as the buyer paying the upfront payment. However, with temporary buydowns, unlike with permanent buydowns, it’s most often something that the buyer requests that the seller pay for as part of the negotiation process. This way, the buyer gets to pay less in mortgage interest for a short time, and the seller pays extra to guarantee that the sale goes through. And if the upfront fee is less than the interest reduction, the buyer also has the option to pay for a temporary buydown themselves if the seller doesn’t want to.

It can be very attractive to pay off your mortgage early. The reason for this is both financial and psychological. Paying down the principle means you’ll be paying less total over the duration of the loan than if you simply made the minimum payments, since interest is based on the principle, not the original loan amount. It will also give you some peace of mind to know that you no longer have any mortgage payments. But those aren’t the only factors at play, and depending on your financial situation, it may actually be better to keep making steady minimum payments.

Of course, if you can barely afford the minimum payments in your budget as-is, the decision is made for you. However, there could be reasons for someone who can afford to put a bit more towards payments to instead hold onto it. One reason is that mortgage interest payments are tax deductible. You may be paying more in mortgage payments, but paying less in taxes. Whether or not this is in your favor in your specific situation is a question for a tax professional. Another is the effects of inflation: as prices and therefore the cost of living continue to increase over time, as long as you make only minimum payments, the total amount you will have owed by the end of your mortgage doesn’t change at all. That means the amounts for payments made towards the end of the loan’s life tend to have lower value in terms of purchasing power, and may be less of an economic burden than other payments you may need to make.

The latter reason doesn’t mean much if you aren’t spending the money on something else, but there’s a good chance you should be. Savings funds, such as retirement funds, and investments both require money to be put into them to gain a profit later. If you don’t have money to invest, you won’t get any in return. Even holding onto the money can be useful, in case it’s needed for emergencies, or a very good investment opportunity crops up.

In September, the share of homebuyers paying all cash was 34.1%. This is the highest it has been since the beginning of 2014, and an increase of 4.6% from September 2022. However, this doesn’t mean homes are more affordable; in fact, it’s the opposite.

While it’s true that a significantly higher share of buyers are paying all cash, there are much fewer sales overall. Total sales decreased by 23% over the past year. Compare this to a decrease of only 11% for all cash sales. Cash sales aren’t going up, rather sales overall are going down, and cash buyers are less affected.

The reason for this is high interest rates, since cash buyers don’t care what the interest rate is for a mortgage loan they aren’t getting. Interest rates fluctuate up and down on a daily basis, but rarely change by much at a time. But in this case, they hit a two decade high in September at 7.2 and then continued an upward trend into October, almost reaching 8%. As of last week, they had started to drop back down. Despite this decrease, with how erratic rates can be, that isn’t a sure sign that rates are now trending downward.

It’s very common to submit late payments, for any of various types of bills or loans, including mortgage loans. Sometimes people just forget to pay. Sometimes they’re waiting for their next paycheck. Maybe some bills are more lenient on late payments than others, so they’re prioritized lower in the budget.

Whatever the reason, most people assume the only downside to a late payment is an extra fee. That’s not the case. The occasional late payment won’t have any impact, but repeated late payments do show up on your credit report. This will reduce your credit score and make it more difficult to qualify for a loan. If possible, you should make sure to pay bills on time, even for small things like phone bills.

When applying for a mortgage loan, your lender may ask you for an insurance binder. In that event, you’re going to need to know what it is, and how to acquire it. An insurance binder is a temporary proof of insurance. If your loan is being insured, you’ll need to ask the company insuring it to provide an insurance binder before the loan can be approved. This temporary proof of insurance exists because the official proof of insurance probably won’t come until after the deadline for loan approval has passed.

Mortgage loans aren’t the only situation in which you may need an insurance binder. You may also need proof of insurance to buy a car, start a business, or rent property. Some of these may involve loans as well, but even if they don’t, it’s still possible you need to be insured for other reasons. The insurance binder in these situations is exactly the same thing — temporary proof of insurance before the official proof of insurance arrives.

As of August 2023, interest rates are somewhere around 7%, possibly higher. While this isn’t astronomically high — they have historically been over 10% — it’s too high for current homeowners to want to exchange their homes. This is because 92% of current homeowners with a mortgage have an interest rate below 6%. Almost a quarter even have locked in an interest rate below 3%.

High home prices are actually somewhat helping current homeowners, since the price boost increases their equity. Prices have increased 14% in the past two years, which results in approximately $86,000 in equity over that time period. However, this may not be enough to offset the increased mortgage costs, especially for those with very low interest rates. Assuming a mortgage of $500,000 and a current interest rate of 3%, a new purchase with the same loan amount would result in a $1,200 increase in mortgage payments per month.

Normally, when demand is low like this, supply is high. This isn’t the case right now. Previously, we would have been able to blame declining construction due to increased construction costs. That’s no longer the case, though, as construction has largely, though not completely, recovered. It may even be simple lack of demand that is the final obstacle to a full recovery for construction. To see the real problem, remember which group we’re talking about — current homeowners. These are the same people who would be selling to buy a new home. If they’re not willing to buy in the current mortgage climate, they’re not selling either.

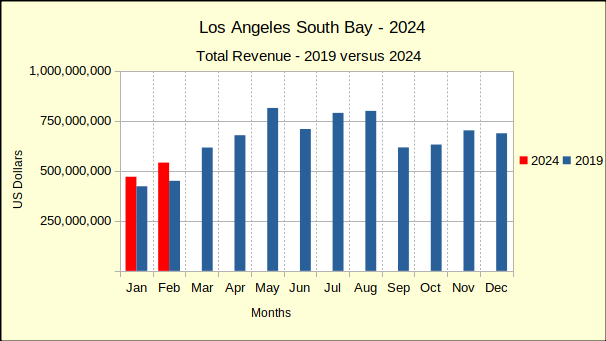

Year to date through July, the gross revenue for South Bay is a mere 3% above that of 2019. At the same time, sales volume, the number of homes sold, is 23% below the sales of 2019. By most standards, 2019 was the pinnacle of real estate business prior to the turbulent years of the Covid pandemic.

Many sources compare current business to that of the pandemic years, partially because it’s easy and partially because the “numbers look better.“ Undeniably, the statistics do look more favorable, however, this analysis takes comparisons beyond the normal “last month” and “same month last year” to include 2023 versus 2019. This allows our readers to see 2023 in a historical context and to more readily recognize the unfolding recession.

While median prices are still above those of 2019 right now, we project the median prices will also drop below the 2019 level before this recession ends. On a month to month basis, prices are falling approximately half the time. On a year to year basis, 2023 prices have dropped below 2022 medians 82% of the time. Median prices for June and July of 2023 fell below 2022 in all four areas both months. Buyers and sellers should anticipate the bottom of the recession in late 2024, or possibly 2025. Normal growth should return in 2026.

The July report from the Federal Reserve Bank (Fed) notes that inflation is expected to continue above the target of 2% through 2025. Accordingly, the Fed efforts to “restrain” the economy (meaning increase interest rates) will continue into 2025. The report indicates that while housing costs are slowing, they continue to increase at inflationary levels, necessitating further reduction.

In the meantime, buyers who are financially able should plan to acquire desirable properties at substantially better prices than will be available after recovery begins. Sellers who anticipate a need to sell before the economic turn-around, should look toward selling sooner rather than later, to minimize the impact of the down-trending market.

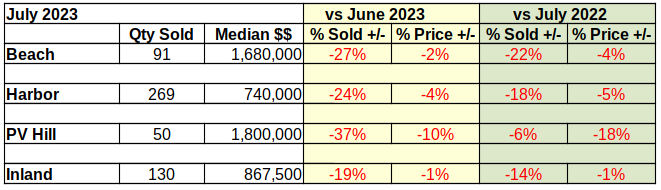

Beach Cities Summer Market Fizzles

From June to July the number of homes sold in the Beach Cities fell 27% and those sold for a median price of 2% less. Some of the decline in sales is attributable to fewer homes available, as sellers hold properties off the market in hopes of improving conditions. Even more is a result of buyers who have lost significant purchasing power as mortgage interest rates have rocketed to over 7%.

Compared to July of 2022, the number of homes sold this July dropped 22% with a decline in median price of 4%. This set of statistics is somewhat deceptive in that last July the real estate market was still in the early stages of the downturn. As the current year progresses, year over year figures will demonstrate the slide more clearly.

Comparing the first seven months of 2023 to both 2022 and 2019 (the most recent year of business not impacted by the pandemic) shows the drift of sales and prices. The number of homes sold fell 24% from 2022 (802 homes) to 2023 (607 homes), while it was down 35% from 2019 (930 homes). The Fed dropped mortgage interest rates to essentially zero during the pandemic to keep the general economy afloat, which resulted in rapid price escalation which ultimately made purchasing a home unaffordable for about 25% of potential buyers. Then to control the resulting inflation, the interest rates jumped up around the 7% mark, which further slowed the real estate market by “pricing out” another 10-15% of buyers. With fewer buyers and stagnating prices, sellers are reacting by pulling property off the market and delaying planned sales.

Median prices fell 4% from 2022 and are still 28% above the median price of Beach Cities homes in 2019.

Harbor Area Sales VolumePlummets

Sales volume in the Harbor area has held up better than the Beach, possibly because median price has taken a greater hit. On a monthly basis, 24% fewer homes were sold (269 in July versus 353 in June). Comparing July of 2023 to July of last year, only 18% fewer closed escrow (269 versus 329).

Generally being an entry level market, the Harbor area tends to react faster to changes in market condition. More upscale neighborhoods frequently “stick to the price” for a longer period of time when markets are declining. Month to month median price dropped 4% in July to $565K. For July of 2022 versus July of 2023, the median fell 5%, from $780K to $740K.

Year to date through July, sales volume was off 24% from last year. Median price was down 4% when compared to the same period in 2022. Looking back to 2019, the number of homes sold during the first seven months of 2023 dropped by 21%. Median price for the same time frame shows up at 32% higher than 2019. Given the median price dropped 4% over the past month (from $772K to $740K), it’s reasonable to project the Harbor area median will end the year near $600K, as it was in 2019.

PV Hill Shows Volatility

Month over month, the number of homes sold on the PV Hill fell from 79 units in June to 50 in July, a decline of 37%. At the same time, the median price dropped 10%, ending the month at $1.8M. This despite a high sale of $12.5M, up from the high of $10M in June.

Year to year, July volume dropped 6% from 53 units in 2022, while median price plummeted 18%, from last year’s $2.2M. Palos Verdes is a unique community with large homes on large lots, many of them highly custom. Combined with the small overall number of homes, these properties truly need to be assessed on an individual basis for realistic projections.

Comparing cumulative sales data for January through July, volume is down 23% and median price is down 17% versus last year. Going back to the stable year of 2019, the number of sales is down 16% while the median is up 34%.

Interestingly, if the Fed’s annual 2% inflation target is added to the years between 2019 and 2023, the median on the Hill would be $1.5M today, instead of $1.8M. Under those circumstances, it would only take a decline of $300K to erase all gain from the past three years. Not a comforting thought for anyone who purchased recently.

Inland Cities Most Stable

The Inland area typifies a classic “middle of the road” performance in the real estate world. Generally the homes are everyday family properties, the sales trends are at the middle of the current South Bay market, and everything seems to happen with minimum drama. So there is little surprise at the minimalist 19% decline in monthly sales volume, the lowest of the South Bay. Likewise there is no shock the Inland cities came in with the lowest monthly price decline, a mere 1% below June.

Similarly, the annual sales volume showed July of 2023 only 14% below last July and the median price just 1% below the same month a year ago.

Year to date for the first seven months of 2023 compared to 2022 looks much the same. The number of homes sold dropped by 22%, 799 in 2023 versus 1021 last year. The median price fell 2% to $868K from $883K. Looking back to the 2019 sales volume for the same time period, the Inland area is off by 18% for the current year. Much like the rest of the South Bay, the median price in 2023 ($868K) remains above that of 2019 ($662K) by 31%.

You might think that once you’ve qualified for a mortgage loan, it’s locked in and you’re free to take on debt without affecting the home purchase. This is not the case. Lenders continue to look at your debt until the purchase is finalized, and taking on additional debt could increase your interest rate, or potentially even disqualify you from the loan.

You certainly don’t want to take additional loans during this process. This includes personal loans and lines of credit. Both can affect your credit score as well as your debt-to-income ratio, both of which lenders look at. Large purchases are also not advisable, especially if they’re paid in installments. This includes vehicles such as cars or boats, and may also include furniture or large appliances. Lenders also look for consistent employment. Even if you’re getting a pay increase by switching jobs, you probably shouldn’t do it just before finalizing a mortgage. At best, it delays the process, and getting paperwork in on time is very important, even if you’ve already locked in the rate.

There are many barriers to homeownership. Many of them are economic, and unfortunately no small percentage of them are the result of discrimination. But one very frequent barrier to homeownership is lack of understanding of the process. Plenty of people who can afford to buy don’t think they can, or don’t think they should, because of misconceptions about mortgages.

One myth that, despite repeated attempts by experts to clarify it, continues to plague prospective homebuyers is the 20% down payment requirement. There is actually no such requirement — it’s a suggestion. It’s a rather economically sound suggestion in many cases, but that doesn’t mean you can’t buy with a lower down payment. The reason it’s so heavily suggested is that not only does a higher down payment translate to reduced loan value and potentially a lower interest rate, but it also avoids private mortgage insurance (PMI). PMI is an additional cost that you won’t incur if your down payment is at least 20%. So a minimum of 20% down payment significantly reduces your overall monthly cost. These high monthly costs are perhaps what’s leading people to believe that renting is cheaper than buying. It can be, in the short term, but almost never is in the long term. But the reason it can be cheaper in the short term is not high mortgage costs; it’s actually the upfront cost of buying a home. Monthly rents usually go up at the same time house prices do, and are often fairly close to monthly mortgage payments. Moreover, buying a home builds equity and allows for resale, while there is no return on investment for renting. Another misperception that leads people to think they can’t get a mortgage is credit requirements. Lenders do look at your credit, but it doesn’t need to be perfect. Most people do not have perfect credit. As long as the lender believes you could reasonably pay back the mortgage, you can qualify with a credit rating as low as 500, though you may only qualify for mortgages with higher interest rates.

The misunderstanding doesn’t stop with whether or not one can qualify for a mortgage. Even once a prospective homebuyer gets to the stage of choosing a mortgage option, there is some confusion about which mortgage options are the best for you. Many people categorically refuse adjustable-rate mortgages (ARMs) and always pick the loan with the lowest interest rate. Neither of these are necessarily the right idea. Fixed-rate mortgages (FRMs) definitely offer stability and can be excellent for people who plan to keep their new home for a while or who are uncertain about their future. On the other hand, ARMs typically have a lower initial interest rate than FRMs. This means they can be more financially sound for people who don’t plan to own the home very long, or who are better positioned to take risks. A low interest rate is obviously a good thing, but it’s far from the only cost associated with getting a loan. If you need to pay PMI, that’s also a factor. But even if you don’t, there will always be closing costs, property taxes, homeowner’s insurance, and maintenance costs. Some of these depend on the price of the home, but some depend on the lender, so be sure to get a breakdown of all the costs before committing to a loan.

Freelance workers and some self-employed people typically don’t have a consistent income. This leads some to doubt whether or not they qualify for a mortgage loan. Lenders will never blanket deny everyone with an irregular income, but it certainly could be more difficult to get a loan. As long as your credit history and debt-to-income ratio are good, it shouldn’t be too much of an issue — you simply may need more documentation to prove that you’re good for it. While lenders will always look at recent income, in the case of irregular income, they may also consider whether or not you’re likely to have clients in the near future based on your occupation.

If you get rejected outright, it’s likely that now isn’t a good time for you to buy in the first place. As long as you aren’t getting rejected, the worst case scenario is a non-qualified mortgage loan, or non-QM loan. Non-QM loans don’t meet the Consumer Financial Protection Bureau guidelines that are designed to ensure borrowers are able to repay their loans, and not all lenders offer them. They may be used for self-employed people, people with irregular income, people with low credit scores, or non-traditional types of properties. Because non-QM loans are riskier for the lender, they do have a drawback for the borrower. They typically have higher interest rates, larger down payment minimums, and/or shorter repayment periods.