Most people want to buy a home that’s move-in ready, but if you don’t mind buying fixers, there are a couple of finance options for you. This doesn’t mean just anyone can renovate a fixer — there’s a lot that goes into it, and you need to make sure you have the know-how or the money to pay someone who does. It can be expensive, and the payout is in the return on investment. If that’s much later down the line because you also plan to live there, that’s okay if you have the money, but it’s important to keep that in mind.

If you don’t have the money, you still need at least a decent credit score. There are two kinds of mortgages designed with home renovation in mind. The 203k Mortgage, one type of FHA loan, is meant for a vast array of different construction projects. In order to secure one, though, you’ll need a credit score of at least 580. Fannie Mae has a loan type specific to renovations, called the HomeStyle Renovation Loan. The max borrow amount is 50% of the total value of the home, and it’s possible to borrow against projected equity. It requires that the renovation be completed within 12 months, and necessitates a credit score of 680 or higher.

If you’re struggling in the current competitive market, you may want to consider buying a new construction home. This isn’t going to be for everyone — new constructions are often more expensive and also come with additional up front costs, since it usually requires a 3% building deposit. Not to mention if you’re not hurting for money, competitive markets are going to be less of a problem for you. Still, if you play your cards right, a new construction home could be a great deal for you without much hassle, and is a much better investment later down the line as well.

Don’t be afraid to negotiate on a new construction home. It’s true that in a competitive market, you may be inclined to bid high to get the best chance at your offer being accepted. New construction is a much smaller market, and your chances are still good even if you bid lower. Alternatively, many new construction negotiations revolve around not price adjustments, but rather the construction materials and appliances. You still want to get ahead of the competition, though; builders aren’t as willing to make drastic changes if they’ve already sold multiple similar homes in the same neighborhood with their default materials.

Everyone wants their bathroom to be a place of comfort with a calm atmosphere. If you’re planning to renovate your bathroom before selling, or just want your guests to feel at home, consider current trends in bathroom design.

There are a few trends popping up recently. The new thing for sinks is the floating vanity. It’s not actually floating — it just may look like it is, since it’s sitting on top of a raised shelf instead of a large cabinet or a tall pillar. Thematically, nature is in. Botanical wallpaper, colorful flowers, bright leaves. And for those of you who want your bathroom to be your own private sanctum, and aren’t planning to show it to others, you can customize floor or shower tiles with your own prints.

Sellers do a lot of things to get their homes ready to show. Tidying messes, repainting walls, fixing deferred maintenance, getting their homes professionally cleaned, hiring photographers or videographers, and sometimes staging their home. What many of them forget to think about is the outside of their home. This is a huge mistake, as the outside is the first part of the home a prospective buyer will see when they arrive.

The first thing you should do is clear the area of objects lying around such as tools or toys, so that you have a clear space to work with. If you have a garden, remember to tend to it by removing weeds and pruning plants, or even getting fresh new plants. Be sure to replace mulch as well. If you have a lawn or shrubs, make sure they’re trimmed. Make sure your sprinklers are working and angled properly as well. Clean out your pool if you have one. Once everything is cleaned up, make sure to sweep any clippings and debris and wash down the driveway and walkways.

There are three primary ways to resolve disputes in business transactions, including real estate transactions: arbitration, mediation, and litigation. Arbitration involves no court activity at all except in choosing a neutral third party, and in fact courts must abide by arbitration even if the decision is erroneous. Mediation is similar to arbitration in that the initial decision is not made by the courts, but it allows to courts to intervene if a resolution is not found. Litigation involves a lawsuit in court.

Historically, businesses have favored arbitration since it was considered the quickest and cheapest method of dispute resolution, and having an arbitration policy protects them from many lawsuits. Now, businesses such as Amazon are quietly changing their policy. Arbitration has turned out more costly than they expected — primarily because they’ve been losing the disputes, in which case they are required to pay both sides. It’s also not always quick. And when the businesses are losing, they’re also not too hot on the decision being legally binding despite not necessarily being legally correct. Instead, mediation is turning out to be a cheaper, fairer, and sometimes quicker method of resolving customer disputes.

After an intensely competitive market, things are finally starting to slow down, with pending sales dropping by 12% nationwide since May. We’re not quite sure if that’s good or bad, though. Part of it can be attributed to seasonal variation — the market does start to slow heading into Q4 — but it never slows this much. It’s unclear whether the steep dropoff is because the market was already incredibly hot, or because buyer demand has lost its momentum. Either way, 2021 was decidedly not a normal year for the real estate market.

And it will continue to not be a normal year. Foreclosure moratoriums have ended, but people are still protected from evictions until September 30th. After that, expect a huge increase in supply as a result of distressed or forced sales. The good news is that rising supply will prompt decreasing prices. But demand is already decreasing, and we aren’t sure yet if it’s going to continue to decrease. People are going to be forced to sell, but may not be able to find buyers. Experts expect that demand will still be high enough in California to soften the blow, and we shouldn’t see prices plummet too far until 2023.

Though certain areas have always been at higher risk for certain types of natural disasters, only since climate change have people heavily prioritized climate risk as a factor in their search. Wildfires, droughts, and floods are becoming much more common, so people are avoiding these areas more. People don’t necessarily know how to research which areas are high and low risk, though. Fortunately, one real estate service, Redfin, is noticing the need and has begun publishing climate ratings.

The ratings aren’t from Redfin — they’re from ClimateCheck, a company which assesses future risk and change in risk on a scale of 0-100. They start with several different global climate models to project risk on a global scale. Then, they localize the data to specific areas by filtering the global risk through local weather patterns. ClimateCheck is now also sending that data to Redfin so that it’s easily accessible for people searching for a home. Of course, you can also visit the ClimateCheck website directly at climatecheck.com.

While it may seem like it was pandemic restrictions that forced the US further into the digital era, most people are actually not uncomfortable with it at all. In a recent survey, 81% of respondents trust online transactions. They don’t necessarily trust all online transactions, though, and they disagree on what exactly makes a transaction feel safe to them.

Predictably, some of the older generations aren’t aware of all the options available to them, such as online notorization services. Perhaps not so predictably, the older generations are actually the most likely to feel safe with digital forms of security. These include two-factor authentication (53% of older respondents), security questions (61%), and PINs (49%). The younger generations, on the other hand, would rather talk to an actual person (53% of younger respondents), even if the discussion is held remotely by phone or online, and don’t want to go through too many online steps to make a transaction go through (22%).

We’ve mentioned a few times that people now working from home more often have been making purchases to make their home more comfortable to live in. This doesn’t merely extend to smart technology, entertainment centers, or upgraded appliances, though. Home renovation projects increased by 25% in the first half of 2021.

36% of people renovating are trying to make better use of the space their have by remodelling rooms, including basements and attics. In many cases, this is probably to create a home office space. 12% have decided they want an entirely new room and are building an addition. 17% are aiming more for the comfort and entertainment aspect, and have opted to add a pool or hot tub. Such renovations are likely for personal reasons as a response to the work-from-home model, but they will also add value to the home later down the road.

In San Francisco and surrounding areas, wage growth has recently outpaced home price growth. Some real estate analysts are now calling the area “affordable,” since prices are dropping relative to wage growth. That label discounts a few rather important factors, though.

First, the majority of wage growth in the area was for high income jobs. These people were already homeowners with stable, high-paying careers. Wage growth doesn’t actually help them purchase a home, it just gives them more disposable income — which they aren’t necessarily lacking.

Second, only in San Francisco itself are home prices actually dropping. In the rest of the region, they’re still going up. And throughout the entire region, they remain exorbitantly high. The Bay Area is one of the most expensive regions in the world.

Third, wages actually may not have gone up at all overall when factoring in unemployment. Unemployed people aren’t considered to have an average wage of $0.00. They’re just not counted in the data. Therefore, the unemployment rate doubling to 5.45% in May from pre-pandemic numbers may have caused average wages to become artificially inflated. Not to mention that no home is actually affordable to unemployed people.

Inventory may be low, but housing isn’t the only thing in short supply. Once work from home became more popular, homeowners started looking to upgrade their homes since they would be spending more time there. Part of that was updating their appliances and buying new furniture, particularly stoves and grills because homeowners would be cooking at home more often. Combined with a decrease in manufacturing productivity due to labor shortages, appliances and furniture are selling out quickly.

While increased new construction is a potential solution to low housing inventory, it’s definitely not going to help the appliance shortage. Even with construction being low, the increased demand for already existing homes is stretching the appliance supply thin — and new constructions would require all new appliances. It’s even affecting the timing of real estate transactions. Closing time is being delayed because the new owners want the place to be move-in ready when it closes, and they aren’t able to get their hands on appliances and furniture.

The second quarter of this year was thought to be a potential turning point in our recovery, as fewer and fewer people were missing payments. This includes rent payments, mortgage payments, and even student loan payments, though the frequency of missed student loan payments is still alarmingly high at 44.8%. Renters received assistance both from government entities and also from their landlords, and the government provided mortgage assistance as well. However, students with loans haven’t been given much help, and there’s been another recent surge of COVID-19 cases due to the delta variant. Some regions that had previously eliminated mask mandates are now requiring them again. The economy won’t recover until the job market stabilizes, which is made much more difficult by health concerns.

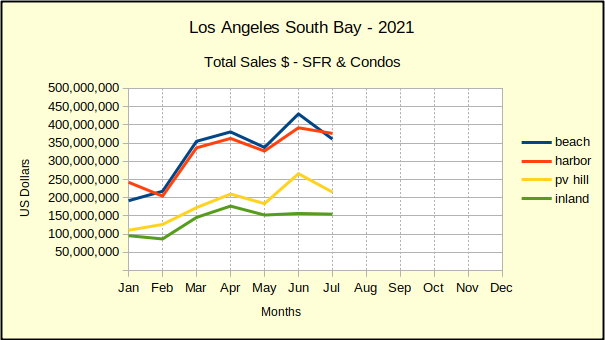

Even with mortgage interest rates under 3% the July market had a hard time keeping momentum. March looked like a game changer, but May went soft. Total dollar sales were up in June but by July prices and sales volume were both headed down again.

So what’s going on here? Sales are yo-yoing across the charts like the economy can’t make up it’s mind. Are we leaving a pandemic or entering one? Banks have started raising the interest rates multiple times. Each time buyers walk away and the rates come down again.

The Coronavirus pandemic has been so pervasive most of us haven’t noticed there is a concurrent recession happening. One pundit I follow recently referred to it as a “two month recession–the shortest in history.” That’s a great punch line, but highly mis-leading. Real estate is a long term business proposition, not an impulse buy.

That’s part of the reason forecasting is so challenging this year. The statistics we would normally compare are last year versus this year. To do so is meaningless in today’s situation because last year was anything but normal and the result of a comparison makes no sense. To demonstrate, this table shows the comparison from this month to last month of the current year, and from last month of the current year to the same month last year.

Is the market good? Or just looking good?

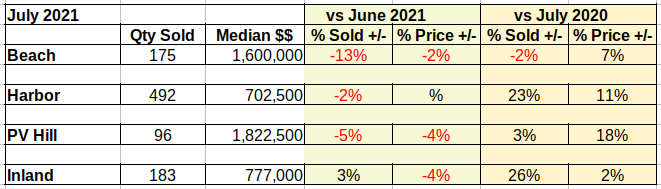

Notice that comparing June to July of 2021, nearly every statistic is negative. Quantity sold was up 3% for the Inland cities, but down in all other areas. Prices were flat in the Harbor area, but down in all other areas. Looking just at the current stats, it looks like a slowing market.

However, it’s easy to portray everything as rosy when you only compare 2021 activity to 2020 activity. Reading it that way, sales volume is down 2% at the Beach, but volume and pricing are up in big numbers everywhere else. For those readers who like to study punditry, watch the authors you read to see who compares both ways, versus who only talks about positive numbers.

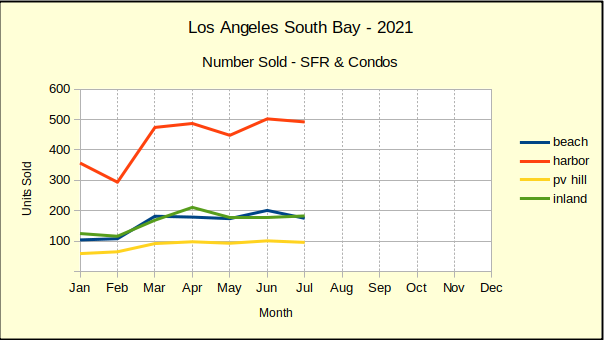

Sales volume flat last four months

By March of this year, all areas took a big jump upward in the number of units sold. The Harbor area, which is often the most friendly to first time buyers, took the biggest jump increasing from roughly 350 units per month to nearly 500 units per month.

Since March the number of units sold has remained stubbornly flat across the South Bay. The Harbor area showed strong activity, recovering almost immediately from a sharp dip in May.

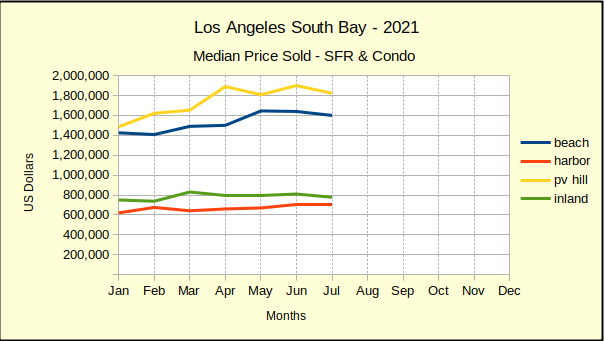

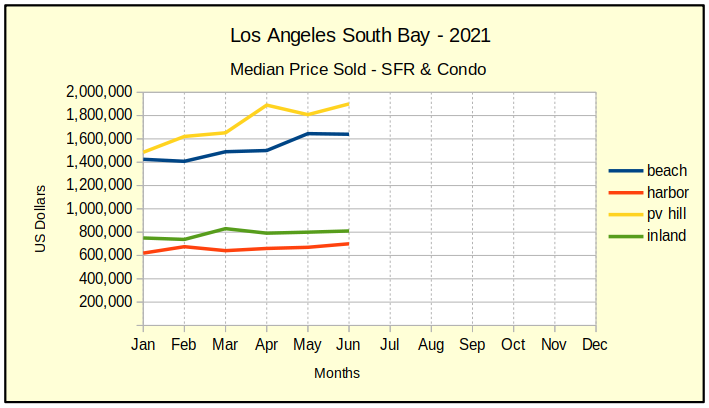

Prices flat last four months

More accurately, Beach prices have been flat the last three months after a $100K jump in May. Inland and Harbor prices have seen very little change since the first of 2021. PV moved upward from January through April, picking up about $400K in median price appreciation. Since then the Hill has also been stable.

Usually more stable than the Beach or the Hill, the median Inland prices have remained very close to their starting point in January. Harbor area prices have bumped up about $100K since the first of the year. We see some of that in appreciation related to retail growth and renewal in San Pedro. On the Long Beach side, we’ve seen good appreciation in the first time buyer community and in the 1-4 rental community.

In summary, real estate in the Los Angeles Suth Bay is on the mend. Don’t mistake that for astronomical growth. We’re getting back to where we were and leveling out.

As more and more employers are considering the possibility of permanent work-from-home, homeowners need to think about ways to create dedicated office space in their home. Of course, if you can afford it, you can make an addition or even just buy a larger home. But not everyone can afford that, so for those who can’t, here are some ways to turn existing space in your home into office space.

For most jobs, a home office needs a desk. But a desk is just an elevated flat surface — it doesn’t have to look like an office desk. You can use a simple table or even just the shelf of a cabinet. You can also just use your dining table. You probably aren’t eating dinner while working. Other types of rooms can also become split-purpose, such as a guest bedroom. If you don’t have guests over — which you probably don’t during a pandemic — you’re free to use it as your office space whenever you want. Even if it’s occupied during the night when your guests are sleeping, you can still get work done there during the day. If you want to get creative and aren’t too spooked out, you can also turn your attic space into a home office with a table and proper lighting.

Many people try to reduce their energy bill by limiting their usage. While this will indeed reduce your bill, it also reduces your comfort. There are better ways to save money on energy bills without sacrificing anything. All these ways cost money, but the investment is worth it to save money over longer periods.

A couple things you can do are one-time investments that will continue to pay dividends. These are both simple modernization. Incandescent bulbs are largely outdated, and should be replaced with LED bulbs, which are more energy efficient and last longer. Expect to save around $75 per year. Smart thermostats are the other one-time investment that will work wonders to save you money. Your HVAC doesn’t need to be working when you’re working, and it can sleep when you’re asleep. A smart thermostat lets you manage that without much effort.

The other way to save money may need to be redone periodically, but it’s still worth it. That’s just simple routine maintenance. Not only does routine maintenance reduce the likelihood of needing to pay gigantic repair costs further down the line, but it can actually improve efficiency even if no repairs become necessary. Clogged HVAC filters won’t stop it from working, but they will make it work harder and expend more energy. The other type of maintenance you may not think of is sealing leaks. Up to 20% of the money you spend on heating and cooling may just be flowing out of small cracks near doors, windows, lighting units, and chimneys. Trapping the air by sealing these leaks with caulk will reduce stress on your HVAC unit.

In order to understand what a stepped-up basis is, first you need to know what a basis is. Basis in real estate is essentially the value of a home discounting any effects of appreciation or depreciation, and is used for tax purposes. It’s calculated as a property’s cost when it was purchased plus the value of any improvements made to the property. When determining the amount of taxable capital gains when selling the property, this is the amount subtracted from the sale price.

Where stepped-up basis comes in is in the case of inherited properties. When a property is inherited, the basis is recalculated based on market values, ignoring both the purchase price and any improvement values. It’s possible that this stepped-up basis causes your capital gains amount to be negative, in which case this can be deducted from your taxable income if it is not your primary residence. Only up to $3000 can be deducted in this way per year, but you can continue to deduct in later years until the loss is settled. The estate can choose to use the market value on either of two dates: the date of the previous owner’s death, or six months from that date, called the alternate valuation date.

Between April 2020 and March 2021, foreign investors purchased 31% fewer properties than the previous 12 months. The total sales volume was down 27%. In a way, this should be expected, since pandemic lockdowns made transactions more difficult. But it comes at the same time that domestic competition was, and still is, heavy. Competition shouldn’t be a huge issue for foreign investors, since they’re usually already wealthy and intending to pay cash.

That said, restrictions are still loosening in other countries, and they’re in a volatile place even in the US. It’s likely that foreign investment simply needs a bit of time to settle back into place. Though there was a drop of over 50% in dollar volume in China, Canada, and Mexico, they’re still all among the top investors in the US, along with India and the UK. This means it was probably a temporary drop-off due to adverse conditions, not a radical shift in general sentiment towards the US.

Mortgage rates have been low for quite a while, even despite a bump earlier due to pandemic-related fees. Those fees have now been eliminated, allowing lenders to drop their rates back down. The current average of 2.78% is not quite as low as the January record low of 2.65%, but anything below 3% is very good.

With rates being so low, now is probably a good time to refinance if you didn’t take advantage of the low rates already. But refinancing is not always the right choice, even with low rates. If you’ve already had your loan for a long time, starting over could just make you end up paying more overall. If you do think refinancing may be right for you, get multiple quotes and take steps to lower your rates. You can do this by improving your credit score, increasing your home equity, or paying optional fees upfront called discount points.

Before we get into the run-of-the-mill analysis of real estate, let’s look at the real estate market in South Bay from a different perspective. We’ve been using a microscope to zoom in on the details of sales volume and median price in various locations, etc. Pretty traditional stuff.

For a couple paragraphs, let’s zoom out and look back at what has happened to the LA South Bay market over the past few years. I want to take a moment to acknowledge my friend James Allen for prompting me to do some research and analysis along this vein. James is editor and publisher of Random Lengths News in the Harbor area. We trade thoughts occasionally about one aspect or another of local real estate and economy. Earlier this month he asked me what I thought about the recently announced 2021 property rolls for Los Angeles County.

Thank you for asking, James.

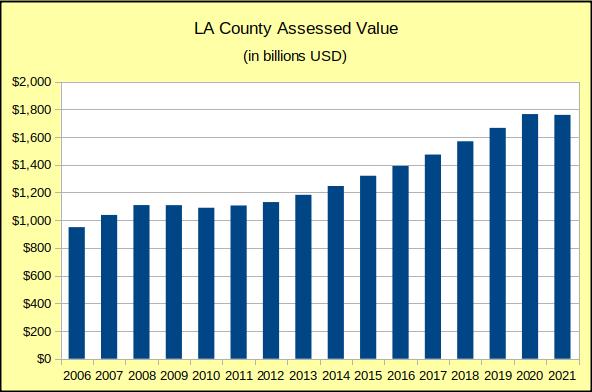

Let’s start by saying the primary task of the County Tax Assessor is to establish every year a value for all the property subject to tax in the county. This year the Assessor has given the total value of LA County property as $1.76 trillion.

Not knowing what to expect, first I pulled in the immediately available data from the Los Angeles County Assessor’s new web site. (I noted a couple of inconsistencies along the way, but given the relative size I decided to consider them rounding errors.) I pulled data back to 2006, which includes the “Great Recession.” The result is shown here and discussed below.

This chart shows the total assessed value, before exemptions, of all property assessed in Los Angeles county. It’s a snapshot in time, taken mid-year corresponding with the tax assessment year. The county has had a steady upward climb with the exception of a flat spot and a shallow trough following the Great Recession during 2007-2008. Taxes are paid in arrears, so the losses didn’t show up until about 18 months later. It took that long to work through the system and show up as a $20B drop in 2010, and then stretch into 2011 and 2012.

The loss of property values following the lending collapse is appears surprisingly shallow. Looking closer at the detail, we see that two of the three primary property value categories offset much of the decline in Single Family Residential (SFR) category. Residential Income (ResInc) values increased .3% and Commercial/Industrial (Comm) values increased .7%, while SFR decreased 1%.

The pattern since 1975 has been that each year the Residential Income category (that’s 5 or more residences in one complex) is stable and brings in about 14% of real property tax revenue. In 1975 ResInc represented 13.5% of real estate values in the County. In 2020 it represented 13.9% of the County value.

The Commercial/Industrial category, which deals in the sale/manufacture of products, has a slightly decreasing percentage of the tax revenue each year. In 1975 Comm property represented 46.6% of taxable real estate value in the County. By 2020 it had declined to 29.2%, about a 17% tax savings for business.

The Residential category represents single family homes and residential complexes of 2-4 units. Commonly termed Residential 1-4, this category has borne an increasing share of the tax burden since 1978. In 1975 SFRs represented 39.9% of taxable real estate in the county. By 2020 homeowners were paying 56.9% of the County’s real property taxes, about a 17% tax increase for homeowners.

Another interesting thing is the strong similarity between 2009 and 2021 relative to the surrounding history. Both years show the market rolling up to the top of the chart, and then taking a slight dip. If 2022 follows the same pattern we should be looking at 12-18 months of flat market followed by several years of steady appreciation.

We do want to be careful here to recognize that there will be adjustments after the fact. Some of these numbers may be changing for years as errors are discovered. Historically, those late changes seldom have a measurable impact.

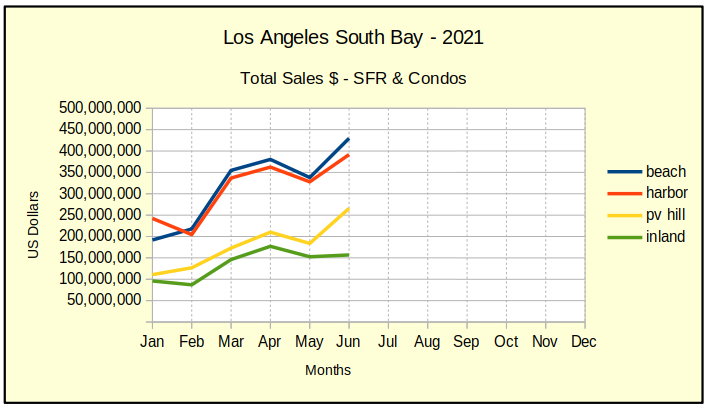

June 2021 Total Dollars Sold

Continuing the trend of recent months, total sales dollars for residential real estate in the Los Angeles South Bay went up in every area. We saw the slowest growth in the Inland Cities which remained nearly level with dollar volume from May.

As usual, the Beach and the Hill had the steepest growth incline on the charts. Overall sales activity has been showing strength in the harbor area. Smart money would consider the future potential from both a residential perspective, which is the primary zoning of both San Pedro and Long Beach, but also from the Commercial/Industrial perspective. The Harbor area has one of the largest concentrations of manufacturing in Southern California.

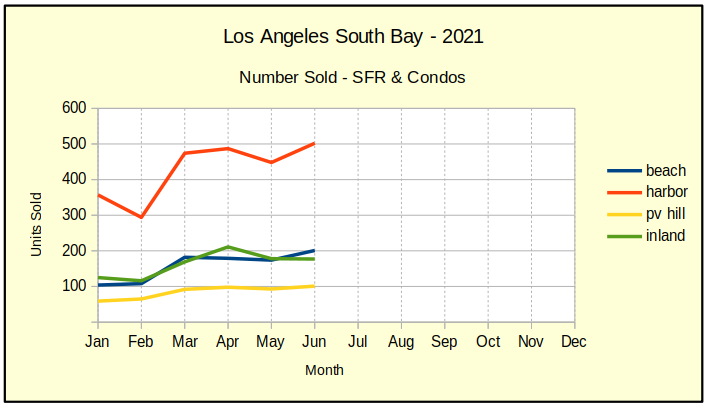

June 2021 Inventory is Rising

June enjoyed a larger inventory of available homes in the South Bay than we’ve seen recently. Earlier this year the shortage of property on the market had reduced listings to as little as two weeks of inventory in some areas.

Active listings right now show that if we stopped listing homes today, all available properties in the Inland cities would be sold within 21 days. That’s a far cry from a normal inventory of 5-6 months, but is better than the 1-2 weeks we’ve been seeing. Similarly, inventory levels are up to 24 days in the Harbor area, 30 days in the Beach Cities and 32 days on the peninsula.

As the inventory climbed, June saw a sizable increase in sales. Back in May, every area recorded declining sales, not because no one wanted to buy, but because not enough people wanted to sell. The chart below shows a healthy increase in volume nearly everywhere. Sales dropped a mere 1% in the Inland cities and were up as much as 16% at the Beach.

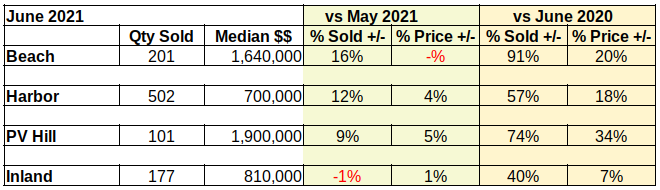

Median Prices are Stabilizing

Let’s face it. Society cannot afford prices that climb 10+ percent in a month. Those are numbers that bespeak failing economies. So, watching South Bay prices level off on the chart below is a good thing. To put perspective on the matter, housing prices traditionally tend to rise at about 4% per year.

June brought some relief in that the steepest price increase was 5% on the Hill, closely followed by the Harbor area at 4%. (Keep in mind that the Palos Verdes peninsula is a very small market area and subject to more vacillation than the other, larger markets.) The Beach came in with no increase in prices and the Inland cities showed a restrained 1% increase.

While homes are selling quickly in the current market, the vast majority of those are existing homes. Construction has been slow for quite some time, and is weakened by high lumber prices. Though lumber prices are below their peak in May, wildfires are still hampering the ability to procure lumber. With so few homes being built, sales of new homes hit a 14 month low in June.

This is a problem not only for construction companies, but for the economy as a whole. Without many homes being built, supply is significantly lagging behind the already high demand. What’s more, many existing homes are not in the category of affordable housing, meaning low-income homebuyers are struggling to find something within their budget, especially with prices being high right now.