The Millennials are currently the generation that makes up most first-time homebuyers, and they’ve certainly been looking for homes with home offices so they can work from home, or extra rooms for their young kids. But there are also many Millennials that already own a home, and they’re probably aiming for the same thing. They will also want to make sure the home has a layout suitable to their needs.

For those Millennials that aren’t first-time buyers, it’s likely they’ll want to upsize. Even though they’re likely rather cash-poor due to the economic circumstances both in their early adulthood and now, some of them may have good equity in their homes because home prices are so high right now. That could help them to purchase something larger by selling their current home.

Under California’s Regional Housing Needs Allocation (RHNA) laws, each local government is required to work with the state government to establish what is called a housing element. The housing element identifies sites that can be redeveloped to meet regional housing needs, within an eight year timeframe. If the city can’t find a usable site under their current zoning laws, the zoning laws need to be modified. In Southern California, the housing element deadline was October 15, 2021. The deadline for Northern California is later this year.

Five cities — Bradbury, La Habra Heights, Laguna Hills, South Pasadena, and Vernon — failed to submit a housing element altogether prior to the deadline, and a sixth, Manhattan Beach, submitted a plan that indicated a site that could not be redeveloped in a reasonable timeframe. The site indicated was the Manhattan Country Club, which was purchased in 2017 and the City of Manhattan Beach cannot guarantee its availability by 2029. Without the 149 units provided by this redevelopment, Manhattan Beach fails to meet its regional housing needs. In response, the nonprofit organization Californians for Homeownership has sued all six of these cities.

A California law allowing duplexes to be built on lots zoned for single-family residences, SB 9, passed in 2021. However, the law doesn’t have much in the way of enforcement. Cities are finding it relatively easy to avoid this with local ordinances that make it effectively impossible, since they can’t legally ban it. The same sort of thing happened with the struggles with building ADUs, which actually became legal nationwide in 1982, but weren’t feasible in most states prior to 2016.

One example is the town of Woodside claiming that the entire town is a mountain lion habitat, and is therefore excluded from the requirement because it’s a habitat for a protected species. Once this reached the news, Attorney General Rob Bonta got on their case and forced them to reverse the decision. All the AG’s office needs is proof that municipalities are attempting to skirt the requirement, and then they can take action. Without an enforcement agency, though, they’re reliant on the spread of information through media, including social media.

Conventional wisdom says you should eat three meals per day, one when you wake up, one at midday, and one in the evening. This convention, though, is actually rather new. And not at all backed by science — it’s based around standard work schedules more than anything. You eat before work, you have a meal during your lunch break, and you come home and eat with your family. However, your meal times should be limited to a smaller window.

Fasting is actually a very necessary process to help repair damage to the body. Of course, this can include the normal eight hours of sleep. But for a healthy body, eight hours should actually be the time that you’re eating, and you should fast the rest of the day, or at least twelve hours. It is possible to do this while still eating three meals, but the standard work schedule makes this difficult. You don’t need as much food as you’re probably eating, though, and you could even just eat one meal per day if you really wanted to. Breakfast in the morning used to be reserved for wealthy people who could afford to eat that often. Skipping breakfast and waiting until your lunch break to eat is actually not a bad idea, even if many people nowadays only do so because they lack the time. For a while, you’re going to be hungry in the mornings, but this is a psychological effect because your body is used to eating at that time, and is temporary. The same thing would happen if you shifted to a new work schedule and had different meal times. It doesn’t actually mean your body needs food.

Over approximately the past decade, the average length of time homeowners have stayed in their home has steadily increased, from 10.1 years in 2012 to the peak of 13.5 years in 2020. Until last year. The figure actually dipped in 2021, decreasing to 13.2 years, even slightly below the 2019 average of 13.3 years.

Much of this can be attributed to the economic aftermath of the pandemic, as relocations increased dramatically in 2021 as a result of work-from-home opportunities and low mortgage rates. It’s unclear whether this is a temporary decline, or 2020 was the peak of homeowner tenure and it’s going to continue to decrease. Analyzing the reasons for the decrease and why it’s been increasing in the first place suggests it’s probably going to go back up. Work-from-home is still happening; however, mortgage rates are no longer low and are still going up. Meanwhile, the initial reasons for the increase over the past decade include increased propensity for aging in place and a desire to keep one’s property tax base low. Neither of these are changing much, even with the ability to transfer your property tax base in some cases.

Property management is a practical field to enter if you are worried about economic stability. It’s incredibly recession proof, as housing is a necessity and therefore people will be renting properties regardless of the economic conditions. But you can’t just decide on a whim to be a property manager — it has legal requirements and best practices.

In the vast majority of cases, being a property manager requires a broker’s license. There are certain cases in which it doesn’t, but they would not apply for rental properties, which are the bulk of managed properties. If you don’t want to get a broker’s license, though, you can consider managing commercial properties, but there would still be many restrictions.

First Tuesday, a real estate journal, has assembled a Property Management 101 infographic, complete with links to articles and PDFs for additional explication. This contains more specific details about the legal requirements, other applicable laws, and market information. You can find the infographic here: https://journal.firsttuesday.us/property-management-101/82682/

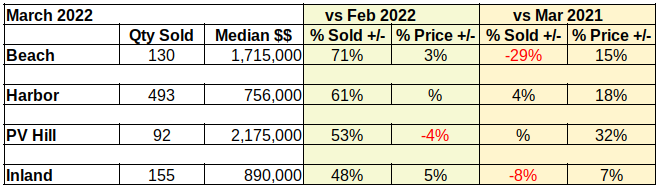

The Federal Reserve Bank tries to keep annual inflation at around 2%. Over the past 12 months the median price increase of a home in the South Bay ranged from 7% (Inland area) to 32% (PV Hill). Clearly housing in the LA area is exceeding the desired inflation rate.

The recent Fed report to Congress stated, “Mortgage rates for households remain low despite recent increases.” In other words, the Fed considers 5% mortgage rates to be “low.” As part of the battle to control runaway inflation, the Fed is expected to implement rate increases. Estimates for how much higher we can expect mortgage rates to rise in the coming year range from approximately 1% to 2% more.

Rates currently at about 5%, we can already see an impact on sales volume and prices in our local monthly data. Real estate industry pundits are projecting an imminent recession. Some say “mild, in 2023.” Some are comparing the current market environment to the 2007 lead-up to the Great Recession. Keeping a probable recession in mind, let’s look at the March sales data.

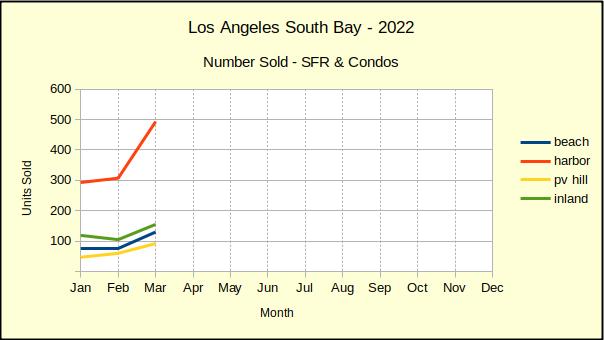

Sales Volume

March is the month when South Bay denizens shake off the winter doldrums and get serious about real estate. The chart last year looked very similar to this. This year the Hill and the Beach were up slightly from last year. The Inland and Harbor areas increased at the same rate as in 2021. Compared to last year’s market, 2022 is distinctly more normal.

The chart makes it look like the Harbor area took an especially large leap in March. That’s just because the Harbor area is so much larger and so many more homes are sold there than the other three areas.. On a percentile basis, sales of Beach homes actually increased at a steeper rate. Sales at the Beach were up from the prior month by 71%, while Harbor area sales increased by 61%.

Normally, we would expect the sales volume to level off now and remain roughly a even line until winter when sales taper off again. If, in the battle to contain inflation, mortgage interest rates climb as fast as the Fed has indicated, we can expect to see the number of homes selling decline. We expect buyers who must buy will adjust the size of the purchase to meet their financing capability. Buyers who aren’t compelled to buy will probably delay and wait for better circumstances.

Median Price

Today, the best measure of home prices is comparing to last month. The market in 2021 was recovering, so some statistics are comparable, while others are still showing signs of impact from the pandemic.

March gave us a month-to-month downturn of -4% on the Hill. Of course, if you remember from last month, February saw escrow close on several new construction homes. Those units pushed the median price exceptionally high, so what we’re seeing now is a return to normal.

While median prices on the Hill were dipping, the Harbor area was flat. Prices there were +4% in January, slowed to +1% in February and had no change in March. This is the largest market area in the South Bay and is often a precursor for change.

The Beach and the Inland areas show continuing price increases of 3% and 5% respectively. Looking back to the first of the year, the Beach has been varied. The March price shift at the Beach is down from the February increase of 6%, but is up from the January decrease of -12%. The Inland numbers show steady growth from -2% in January to +5% in March.

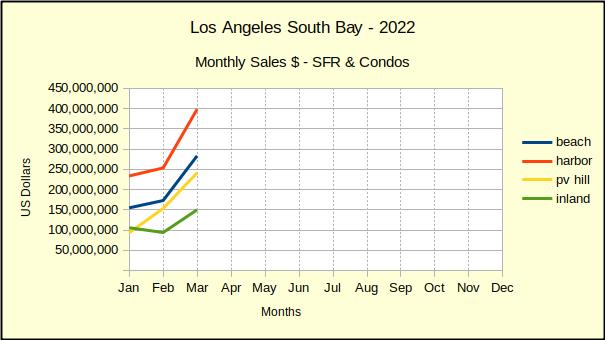

Monthly Sales Dollars

The dollar value of March sales in the South Bay showed positive increases for all areas for the first time this year. This is important because normal growth in our capitalist system will almost always show the sold value from the current year to be larger than that of the preceeding year. The negative numbers from January and February are reflections of the troubled economics of 2021.

We expect the sales dollars to level out as the median price pulls back to a normal growth pattern. If the Fed is to realize any kind of reasonable slowdown for inflation, the monthly median prices have to stabilize at a rate of increase barely above zero. As of March the cumulative median for each area ranges from +3% to +20%. We’re not going to get to +2% inflation with those results.

The Statistics

Supposedly, charts are easier to read for most people. I like to include this table because it packs all the data from the three charts above, plus background detail, into a fraction of the space. Here we see the specific quanties sold in each area, plus the median price of the area, for the month of March.

% symbol indicates no change from prior period.

More importantly, the table shows at a glance how March 2022 compared to February of this year, and March of last year. All four areas currently have increasing sales, in part because the inventory is growing. In addition, there’s a bit of panic from the rapid interest rate increase.

At the same time, the table quickly shows that the median price has moderated in all four areas from what was happening in 2021.

Notable Sales

The South Bay in Los Angeles is a highly diverse area. In the distance of a few minutes it’s possible to drive from the lowest priced property sold in March to the highest priced property sold in March.

This studio condo in Long Beach sold for $249,900. It offers 441 sqft of airspace, no assigned parking, has an HOA fee of $149, and was originally built in 1913.

This 7 bedroom, 15 bathroom house in Palos Verdes Estates sold for $17,150,000. It offers 13,000 sqft on a 3 acre lot, has 5 garage spaces and was built in 2006.

Among the California State bills that the Assembly is voting on this week are four bills related to real estate. These are AB 2050, AB 2469, AB 2710, and AB 2053. Most of these bills are aimed at protecting tenant rights, while AB 2053 is designed to create revenue-neutral affordable housing. The voting will take place on April 19th and 20th.

AB 2050 modifies the Ellis Act, which allows landlords to evict tenants in order to stop renting the property altogether. AB 2050 would require a landlord to rent out their property for at least 5 years before invoking the Ellis Act. AB 2469 establishes a mandatory statewide rental registry, which prohibits landlords from raising rents or evicting tenants without submitting information to the registry each time the lease is initiated, altered, or terminated. AB 2710 establishes Right of First Offer legislation, requiring owners of currently tenant-occupied property to offer sale to certain qualified entities, including the tenants, before accepting an offer. The seller does not need to accept an offer from qualified entities, but must give them ten days to match any accepted offer. AB 2053 establishes the California Housing Authority, which is designed to build and acquire mixed-use affordable rental housing, which would be publicly owned.

You’ve heard of first-time homebuyers. You don’t hear as much about first-time homesellers, even though of course they must exist. But now there’s reason for them to make the news. It turns out a significant number of homeowners in the younger generations — Gen Z and Millennials — are already looking to sell, despite also being the predominant first-time homebuyer generations. This includes 44% of Gen Z homeowners and 35% of Millennial homeowners.

With both first-time homebuyers and first-time homesellers being mainly between the ages of 18 and 41, agents really need to focus their marketing efforts if they want to do business with them. That requires knowing what people in this age category are looking at in terms of marketing. 59% of Gen Zers and 65% of Millennials consider social media marketing to be important for a real estate agent. Fortunately, this isn’t likely to ostracize other cohorts, since 58% of Gen Xers and 60% of Baby Boomers are in agreement. Agents that don’t have social media presence and are struggling to find deals may want to rethink their strategy.

Many older people think of Millennials as being young kids who have no life experience and no financial know-how. The reality is Millennials are in the normal age range for first-time homebuyers, and some are even older. Their financial problems are not due to lack of knowledge. It’s due to a series of economic struggles that were completely out of their control.

Most Millennials came to age during the Great Recession, and so employment simply wasn’t available during the years when they were expected to find a job. That has made it more difficult to find one even after the Great Recession ended, as employers are expecting someone their age to have more experience. The 2020 recession, during a time when society expects their age group to be looking for a house, hit Millennials yet again.

In addition, inflation has far outpaced wage growth. Even those Millennials who have a job are not earning nearly as much adjusted for inflation as older generations were at the same age. Only about half of Millennials are employed full-time, and less than two-thirds are employed at all. Even though wages are increasing, they are still stagnant because of how quickly prices are increasing. Between 2012, when the market was finally recovering from the Great Recession, and 2020, when the most recent recession started, wage growth was at 24%. Home prices, however, went up over 3.5 times as much, by 86%.

After a period of low mortgage rates, they’re going back up quickly. That is the expected effect of current Fed policy, but we may hit 5% faster than expected, possibly as early as next month. As of the beginning of April, the average 30-year fixed rate was 4.59%. If they do hit 5%, it would be highest rate in the past decade, though they did get close in November of 2018 at 4.94%.

The increasing rates are definitely going to slow down the real estate market. That may be a good thing for the market, given how hot it’s been, but it’s definitely not good for buyers. Demand isn’t going to disappear completely, though. And the effect is probably mostly psychological. Historically speaking, 5% isn’t a particularly high rate. It’s just that rates have been trending downward for quite some time, so it isn’t going to be familiar territory for the new generations of buyers.

It’s true that some people have taken work-from-home as an opportunity to travel far and wide, but it could be that most buyers still want to be relatively near where they already are. They also aren’t looking for major changes in community type, whether urban, suburban, or rural. Nor are their motivations primarily financial, except in cases in which they changed jobs.

In a small survey of 514 respondents who were actively searching for a home, just over 40% of them were looking between 6 and 50 miles away, and over a quarter were searching between 2-5 miles away. However, it is important to note that of those looking more than 50 miles away, most were looking over 500 miles away. Between 63% and 77% of respondents wanted to stay in the same community type, and if they wanted a switchup, it would probably be to a suburban area. The primary reasons for moving were either lifestyle fit or major life events, not a growing wanderlust prompted by the possibility of a work-from-home model.

Attempting to sell your home yourself, without paying an agent, may seem tempting. Especially if this isn’t your first sale, you may think you know everything. The fact of the matter is, you probably don’t; moreover, FSBO presents problems even if you understand the process.

In order to sell your home, you’ll need to take time out of your day to show your home to prospective buyers. This could be a colossal waste of time if the buyers aren’t actually interested and just want to look. There’s also a large amount of paperwork involved. That also takes time, and it’s easy to make mistakes. Maybe you think you’ve done all the paperwork before and know how it works, but the laws could have changed or this sale could involve paperwork the previous sale didn’t require. Even professional agents make mistakes sometimes — but they have errors and omissions insurance. You probably don’t. That can lead to lawsuits. In the unlikely situation that you’ve done all your research and know exactly what to do, it’s still likely that you’ll receive fewer or lower offers. Agents tend to be wary of FBSO sales because of all the issues they can present, and so are unlikely to show them to their clients.

Many people are still delinquent on rent payments as a result of the recent recession. Some relief came in the form of emergency rental assistance (ERA), which also required landlords take additional steps before being able to evict for nonpayment. The additional protections were set to expire on March 31st, but there was a last minute change to the law.

Under the new regulations, while the protection will still only apply to delinquencies on rent payments owed before March 31st, it will now continue to apply to those delinquencies through July 30th if the ERA application is still being processed. Tenants will still owe rent for April and subsequent months, even if their ERA application for earlier payments is still being processed.

Spring tends to be the hottest season for the real estate market, which means heavy buyer competition, especially while inventory is still recovering. These tips, including some lesser-known ones, can help you stay in the running.

It’s not unusual for homes to be listed low in order to garner interest. While this may not be necessary with higher demand than supply, it’s good to know that you may want to look lower than your expected budget. Even if an offer is accepted near the list price, that just means you have a bit extra for repairs or updates. Alternatively, you could put it towards a higher earnest money deposit, which shows the seller you’re actually serious. Getting an actual approval letter, and not just a pre-approval, will do the same thing.

There are also a few contract terms you can change to appeal more to sellers. A good agent can advise you on matters related to your current situation to see which contract terms are best for you. These include various waivers, particularly an inspection waiver; a lease-back for sellers who are also prospective buyers; and a relatively unknown thing called an escalation clause. An escalation clause, also called an escalator, lets the seller know as soon as they receive your offer that you are willing to increase the offer if outbid, and defines an upper limit. This can prevent a situation in which the seller sees your offer, sees an offer higher than yours, and accepts the higher offer, without realizing that the higher offer is actually lower than what you are willing to pay.

What buyers want and what they’re able to get isn’t always the same thing. Buyers nowadays are frequently settling, due to high prices. However, their search keywords are a decent indicator of what they want, even if it’s just wishful thinking. And what they want right now is outdoor living, except from the comfort of their home.

The number 1 most searched home feature is a swimming pool. In fact, buyers currently seem rather obsessed with water. If they can’t get a pool or hot tub, many are happy with a view of the water, and it doesn’t necessarily need to be an ocean view. The second most searched term is a view of rivers, and beaches, waterfronts, lakes, or really any kind of water is a popular view. Buyers are also looking for other types of outdoor amenities, such as horse facilities, boating facilities, golf, tennis, and basketball. And of course, they search for a large lot or outbuildings to accommodate all these features.