There are four different types of commercial leases that each place different responsibilities on the tenant and landlord. These are known as net lease, double net lease, triple net lease, and absolute triple net lease. They can be abbreviated as N, NN, NNN, and Absolute NNN respectively. In general, N places the fewest responsibilities on the tenant and Absolute NNN places the most. However, in certain cases a tenant may prefer an NN lease over an N lease, if the tenant is adamant about not paying maintenance costs.

For each of these lease types, the tenant is responsible for their base rent plus some additional property expenses. The landlord in turn is responsible for structural issues, for all except an Absolute NNN lease, and may be responsible for some other costs. In an N lease, the additional property expenses tenant is responsible for include a portion of the property taxes, insurance, and maintenance costs. The landlord is responsible for major repairs. With an NN lease, the tenant is responsible for the entirety of the property taxes and insurance, but unlike an N lease, it’s the landlord who is responsible for maintenance costs. With an NNN lease, the landlord’s only responsibility is major structural repairs. The landlord’s only role for an Absolute NNN lease is collecting rent.

The high mortgage interest rates we’ve been experiencing have been the result of benchmark rate increases by the Federal Reserve. The benchmark rate isn’t directly tied to mortgage interest rates, but the benchmark rate does have a strong effect on interest rates. Now, though, no more rate hikes are expected, which should cause interest rates to level off, and then start to decline.

This levelling off followed by a decline is exactly what the Fed was aiming for with the rate hikes. It’s impossible for mortgage rates to drop without the real estate market, and in turn the economy as a whole, taking a hit. By raising rates above what they should be during a period of high prices, what the Fed has done is soften the blow by allowing the decline to be more gradual. Of course, this comes at the cost of significantly decreased affordability for the period of the rate hikes. Once interest rates fall below 6%, which should happen before the end of the year, the market should pick back up again. However, the effect may not be noticed until next year, as the end of the year is not generally a time of heavy market activity.

Some parents want to help their kids any way they can, including by helping them pay their mortgage. Or perhaps they’ve suggested that their inheritance be used for this purpose. Others want to instill the importance of financial responsibility or independence. Some simply can’t afford to help. But if you do want to help your kids with their mortgage, there is some important tax information you should be aware of.

One very common way for parents to assist their kids is with a financial gift. This isn’t just as simple as giving them money. Financial gifts above a certain amount per year do need to be recorded, and may be subject to a gift tax. In 2023, this amount is anything over $17,000 annually, but this value could change each year. Income tax could come into play if instead of gifting your child money, you provide them with a loan. The interest you receive on the loan must be reported as income and may be subject to income tax, and may also be deductible for your child. Capital gains tax is relevant if your kid inherits a property from you or you gift them a property. In the case of a gift, when your kid sells the home, they will need to pay capital gains tax if the home appreciated in value. In the case of inheritance, the capital gains tax amount is based only on the amount of appreciation and not the total value of the home.

Builders have had it rough the past few years. The pandemic resulted in skyrocketing lumber prices as well as many job losses for construction workers. In order to get the most bang for their buck, builders started building luxury homes, which generally have a higher profit to cost ratio. But this couldn’t last long, as both market demand and legislation pressured them towards construction of affordable living homes, while at the same time, zoning restrictions made even this rather difficult.

Pressures on construction companies have started to ease up in most of the country, but not everywhere. Particularly in the West and Northwest, available land is an issue. Fortunately, builders may have figured it out and now have a new plan: Make smaller homes. It’s predicted that more affordable starter homes will become available within the next year or two, as 42% of builders are reducing the square footage of their homes. It doesn’t even require a big change — the nation’s largest homebuilder, D.R. Horton, is only reducing home sizes by an average of 2%. Builders are also planning to build more townhomes and duplexes, which take up significantly less space per unit than single-family residences.

The initial estimate of the median home price in California in the first quarter of 2023 was $760,260, for single-family residences (SFRs) only. Using this estimate, about 20% of California households could afford to purchase a median-priced home. This demonstrates a rebound from the last quarter of 2022, where it had dropped to 17% of households, down from 24% in the first quarter of 2022.

Affordability is weakest in Mono County, which experienced no change from its very low 7% affordability. The most affordable county has remained Lassen County, despise a slight drop from 54% at the end of 2022 to 53% now. Mendocino County had the largest increase in affordability, an increase of 12% from 14% at the end of 2022 to 26% now. No decreases in affordability exceeded 3% during the same time frame.

Though the US as a whole is significantly more affordable that the rather expensive California, the numbers show a similar trend. Affordability was higher in the first quarter of 2022, at 47%. It had dropped to 38% in the last quarter of 2022 before inching back up to 40% in 2023. Only three California counties — Siskiyou, Plumas, and Lassen — have a higher affordability rating than the national average.

Come together for the Gathering for the Grand 2023! This year the grand event will be a live concert held at the Warner Grand Theatre, featuring premier Rolling Stones tribute band, JUMPING JACK FLASH! Jumping Jack Flash delivers that same raw, high-energy, larger-than-life rock show that you remember from the Rolling Stones. The honoree this year is the Warner Grand “herself”, right before the Theatre closes for its big renovation. Dress as your favorite rock star and celebrate the Theatre’s past, present and future!

Proceeds benefit Grand Vision Foundation’s performing arts & music education programs.

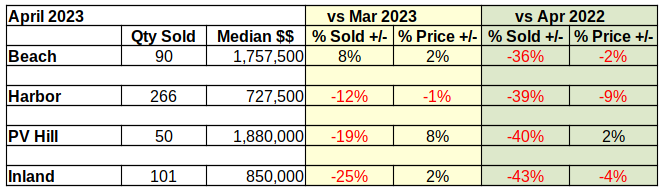

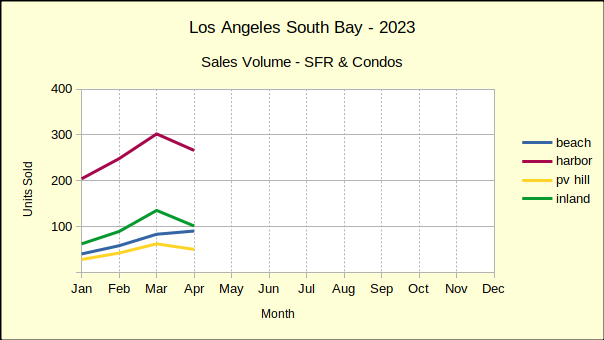

April of 2023 ended with a 40% drop in the number of homes sold across the South Bay compared to 2022. The median price was down 20% from last year in Palos Verdes and is up by a mere 1% at the Beach. Year to year median prices across the South Bay are down approximately 5%. Cumulative sales revenue for the first four months across the South Bay has dropped 39% from 2022 numbers.

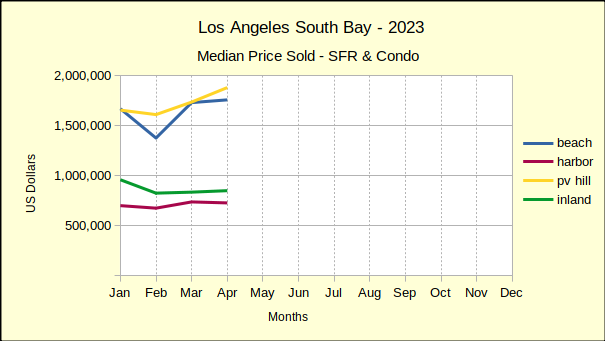

Year to date, 2023 has been one of the slowest markets we’ve seen in recent years. Sales are off by 43% in the Beach Cities and are down by 22% across the South Bay compared to last year. Median prices escalated dramatically in 2021-2022, and are still above those of 2019 by 30-35%. However, the median has fallen in all four areas since late last year. We anticipate the median price continuing to drop until interest rates seriously decline again.

Business in the years between 2019 and 2023 was seriously impacted by the pandemic, and the massive government funds released to counter the effect of the pandemic. Looking back at 2019 and comparing it to 2023 offers a perspective on where the market is and where we can expect it to go during the balance of the year. Today we see a huge decline in the number of homes being sold. That has yet to translate into a significant decline in median prices, although 75% of year over year sales show prices falling.

At the same time the Average Days On Market (ADOM) has increased from about 7 days during the sales boom of 2021-2022 to about 30 days now. That’s a four-fold increase in the amount of time it takes to sell a home. For a seller who needs to move, that will feel like an eternity. It’s that sense of urgency that drives prices down and ultimately results in a shift of the market.

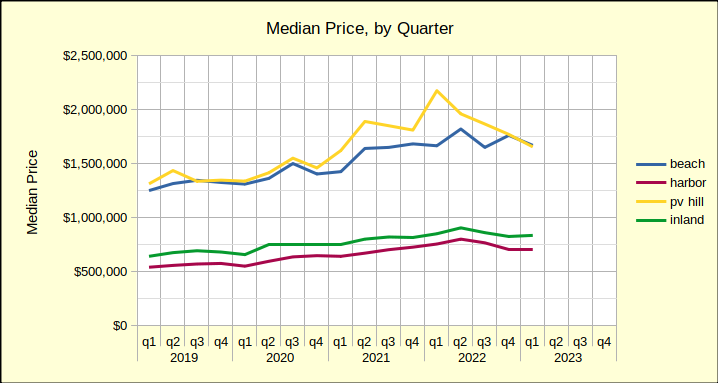

At the Beach “Sticky Prices”

Sellers in the Beach Cities had a good month in April—at least compared to March of this year. Compared to April of last year, the picture is far worse.

The number of homes sold in April was up 8% compared to March. That sounds positive, until the realization that sales volume was down 36% compared to April of 2022. At the same time, the median price was up 2% versus last month, and down 2% compared to the same month last year.

There’s a lot of talk among brokers these days about “sticky prices.” Recent sales at the Beach offer a good example of what that means. The statistics show that sales are down 36% from last year, however prices have only dropped 2%. Sales are falling because the number of viable buyers is down.

Interest rate increases have pushed the most tenuous group of prospective buyers out of the market. At the same time, sellers are still revelling in the boost to median prices that came with record low interest rates during the pandemic. Beach area sellers have yet to adjust to the reality of a re-trenching economy. That adjustment is “sticky prices.”

Harbor Sales and Prices Off

The neighborhood can affect how long it takes the median price to respond to changes in the economic environment. While sales volume and pricing has remained strong at the Beach, sellers and buyers in entry level communities are impacted more immediately by shifts in the economy.

Thus we see the give and take of the market bring median prices into a stable range early in the year in the Harbor area. The red line in the median price chart below shows four months of reasonably steady prices. While month over month prices have shown only a 1% drop, the monthly sales volume has taken a 12% dive from March, as shown in the Sales Volume chart, above.

The monthly decline in sales was multiplied in the year over year statistics. April sales volume was down 39% from April of 2022. For the same period, the declining sales volume was coupled with a 9% drop in median price. So the entry level communities demonstrate a much quicker and deeper response to changes in the financial picture.

Part of that response is the time on market, which has risen from 15 ADOM in mid-2021 to 26 ADOM in April of this year. The increasing time required to sell homes contributes to the number of homes available on the market. Both factors contribute to falling purchase prices.

Palos Verdes In Extremes

Through 2021 and 2022 home prices on the Palos Verdes peninsula benefitted from the Covid pandemic more than any area in the South Bay. In the median price by quarter chart, shown below, the yellow line is seen jumping up and away from the blue line of the Beach Cities. Unfortunately for home owners on the Hill, that price boost has already pulled back into line with prices of Beach area homes.

Comparing the first four months of the 2023 to 2022 median prices on the Hill have dropped 16%. It’s a steep decline in view of decreases at 3% and 6% in the Inland and Harbor areas, respectively. Even more so when looking at the 1% increase at the Beach.

The statistics look much better when comparing Palos Verdes sales from 2023 to statistics from 2019, the last “normal” year of real estate business. Sales volume on the Hill is down a modest 13%–modest by comparison to the Beach, which is down 43%. In contrast, median prices in 2023, compared to 2019, are still showing positive growth of 30%.

So, if one were to take the Federal Reserve System position that 2% annual growth is a desirable target, where would prices be today? The median price in Palos Verdes in May of 2019 was $1.5M. Jump forward to 2023 and that becomes about $1.6M. The median on the Hill last month was $1.9M, which suggests further price reductions.

Inland – The Steepest Fall

From an investment perspective, homes in the Inland area of the Los Angeles South Bay are “bread and butter.” These are the homes, much like those in the Harbor area, which reliably increase in value over long periods of time at a slow and steady rate. Most importantly, they house the bulk of our community.

In the short term, Inland home sales volume is down 25% from March to April of this year. Median prices are up 2% for the same period. This is the steepest fall in number of homes sold in the four areas charted.

Year over year, sales volume is off even more at 43% below April of 2022, and prices similarly down by 4%. We expect a seasonal boost to sales for the second quarter, when families most frequently schedule moves. Beyond that, most predictions are for continued softening in the real estate market as the Fed struggles with inflation. (The April Consumer Price Index, [CPI-U] for Los Angeles metro was 5.2% for Housing.)

If you’re planning to hire a contractor, chances are it’s because you don’t know how to do the work yourself. Because of this, it’s common to believe that the contractor knows what they’re doing and you don’t need to get involved or ask questions. But that couldn’t be further from the truth. Communication is very important when dealing with contractors to make sure the job that’s being done is the job you wanted. It may require a bit of research, but you should learn how to ask the right questions to get the right contractor for your job.

The specifics will depend on the particular job you want done, but there are some things you should be doing prior to choosing a contractor regardless of the job. When looking for a contractor, get quotes from multiple people and verify all of their credentials, licenses, and certifications, as well as experience. Make sure the contractor you pick has liability insurance and worker’s compensation insurance. The next part is what may require some additional research, and that is defining the scope of the job and setting a timeline. If you don’t know exactly what you’re looking to be done, the contractor won’t either, even if they know how to do it. When you get the contract, make sure it contains all the necessary elements before signing. A proper contract contains all the terms and conditions, payment information, warranties, and dispute resolution procedures.

In the US in general, the market has been slowing down. This is leading to a higher inventory — in March 2023, the number of homes for sale was 9% higher than in March 2022. But this isn’t the case in California. In fact, for-sale inventory in California’s largest metro areas was actually down 14% between the same two months. The difference is most stark in San Jose, where inventory dropped 32%.

However, this does have a couple of explanations. Available inventory is a raw number. It doesn’t take into account the number of buyers. Home sales volume is more indicative of the number of buyers, and that dropped significantly more than 14% between March 2022 and March 2023, by 33%. Thus, the ratio of homes available per buyer is actually higher than it was last year. In addition, California is still being affected by lower construction rates, while it has recovered in many other states. The major reason is pushback from local homeowners who don’t want additional construction in their neighborhood.

Are you planning to have kids soon and need ideas for names? The Social Security Administration (SSA) just released the list of the most popular baby names last year. If you want to be trendy, you can pick something from this list. Alternatively, you can take it as a list of names to avoid. Either way, it could be useful information, or could simply spark your creativity.

Liam and Olivia are the top choices for boys and girls respectively, and have been for several years now. Liam has been #1 for six years, and Olivia for four. The rest of the top ten list for boys are Noah, Oliver, James, Elijah, William, Henry, Lucas, Benjamin, and Theodore. For girls, they’re Emma, Charlotte, Amelia, Sophia, Isabella, Ava, Mia, Evelyn, and Luna. Of all twenty of these names, Luna is the only one that has never been in the top 10 before now.

The SSA also provided data on which names are growing fastest in popularity. None of these names are anywhere near the top 10, but they’re gaining the fastest. For boys, they’re Dutton, Kayce, Chosen, Khaza, and Eithan. For girls, they’re Wrenlee, Neriah, Arlet, Georgina, and Amiri.

Private Mortgage Insurance, or PMI, is a type of insurance that many lenders require for any mortgage with a down payment less than 20%. This is the main reason a minimum 20% down payment is so widely suggested. But if you aren’t able to put 20% down and are forced to take PMI, you needn’t worry too much. It’s also possible to get rid of existing PMI in certain circumstances.

One method that doesn’t require any specific action on your part is to simply wait until automatic termination of PMI, which occurs when you reach 22% equity and are current on your mortgage payments. However, it’s possible to request to terminate it earlier as long as your equity is at least 20%. There are a few ways to do this faster. The simplest option is to pay more than the required mortgage payment. This allows you to reach 20% equity faster while also reducing your PMI costs along the way. Another way you could potentially reduce payments to speed up equity gain is to refinance to a lower interest rate. Depending on your circumstances, this may or may not increase your total mortgage cost excluding PMI, but could eliminate PMI faster. There’s one more possibility: Reappraising your home. It’s possible that your home has accrued enough value that determining the new value of your home reveals that you actually do have at least 20% equity. If you do, you can request to remove PMI.

At the start of May, the Federal Housing Finance Agency (FHFA) modified the fee structure for loans guaranteed by Fannie Mae or Freddie Mac. The goal of the change was to increase the accessibility of homeownership to disadvantaged groups. In order to achieve this, fees were reduced for low-income borrowers, first-time homebuyers, and those with credit scores below 680.

However, reducing some fees meant needing to increase fees elsewhere. Fees increased significantly for middle income earners, those making larger down payments, cash-out refinance applicants, and second-home buyers. Critics argue this is a bad idea, since middle-income earners are more ready to buy and less risky to lend to. But despite the fee increases for middle-income earners, fees are still lower the higher your credit score — that hasn’t changed. If the changes push middle-income earners away, the effect is probably psychological, not necessarily financial.

Real estate is almost always a solid investment. The two major barriers are the high initial investment required and the necessity to manage the property. The former can’t really be fixed, but there are things you can do about the latter. While there is always the option to hire a property manager, this increases the investment required and can make the profits less attractive. Fortunately, there are some other options for real estate investment without being involved in management, which is termed passive real estate investment.

The other options are real estate investment trusts (REITs), real estate crowdfunding, private real estate funds, and exchange-traded funds (ETFs). In all of these cases, you are investing only a portion of the funds. This also reduces the barrier to entry, but at the cost of lower profits. REITs are trusts that own and manage income properties. Investors can purchase shares of REITs that pay dividends. Similar to REITs, ETFs are publicly traded; however, ETFs are traded on the stock market rather than purchased as shares of a company. Real estate crowdfunding and private real estate funds both involve a group of investors pooling money for an investment project. Crowdfunding gives each investor more choice about which projects they’re interested in, which is better for an investor who knows what they’re doing while still not putting the onus of management on them. Private real estate funds are the option for investors who just want to throw money at an investment and not be involved at all, as they are managed by professionals that choose the projects.

A bridge loan is a type of loan that uses equity in your current home to finance the purchase of a new home. Like nearly any loan, a bridge loan has interest and is paid off in installments. Unlike a traditional loan, though, the balance is paid off when your current home is sold. While you don’t technically need to sell your current home to pay off a bridge loan, it’s most useful in situations in which you want to both buy and sell.

Some seller-buyers will sell first, then use the sale proceeds to purchase a new home. However, this comes with potential uncertainties about how long you will be left without a home, especially if you make offers and aren’t successful. You may be staying in hotels or renting for longer than anticipated. Another option is to buy a home first using a traditional loan, then sell. If bridge loans weren’t a thing, there wouldn’t be anything inherently wrong with this. But they are a thing, and this is exactly the situation they’re designed for. While bridge loans do come with a higher interest rate than traditional loans, the length of the loan is typically much shorter. After all, most traditional loans are 15 or 30 years, and no one is going to be waiting that long for a sale to finalize. One caveat of bridge loans is that since they are based on the equity in your current home, if your equity is low, the loan amount will also be low.

This year has not been a good year for banks. City National Bank settled for millions early this year. In March, two major banks — Silicon Valley Bank (SVB) and Signature Bank — went bankrupt. These weren’t the only banks to fail, but they were the most well known. Now, First Republic, the largest bank to fail since Washington Mutual in 2008, has been added to list of failed banks. After First Republic failed, it was briefly taken under government control before being auctioned off. JPMorgan Chase, who had also purchased Washington Mutual when it failed, is the new owner of First Republic. The entire situation with First Republic has cost the Federal Deposit Insurance Corporation (FDIC) about $13 billion.

However, analysts and federal regulators emphasize that the banking crisis has calmed down, now. When SVB and Signature Bank failed, fears were warranted. But those failures sparked an inquiry into which banks were likely to fail, and First Republic was identified as a likely candidate early on. So, this wasn’t entirely unexpected, and regulators were able to act quickly. Additionally, the FDIC admits that SVB’s failure was partially their fault, as they had not been meticulous in their supervision. Analysts aren’t expecting any additional major bank failures in the near future.

If you want to make the most of a partial remodel, look no further than the kitchen. Unless no one in the family knows how to cook, people will spend quite a bit of time there. Kitchen remodels are a great investment if you know what’s trending. Right now, that means terrazzo floors, soapstone, and quartz. Marble and granite are old standbys that won’t generate additional interest. Additionally, more avid chefs are definitely looking for less common kitchen amenities. These include steam ovens, pizza ovens, and professional-grade appliances.

Getting all new furniture may not seem like a solid investment, but it certainly can be. You probably do want to if your current furniture is noticeably old or beaten up. And while you’re at it, you should choose the leading trend, which remains the modern farmhouse style. This style is typified by comfort, neutral color schemes, reclaimed materials, and vintage accessories, while at the same time using modern clean lines. Nearly all modern farmhouse style homes use reclaimed wood and have large, comfortable furniture. Many display rustic-looking, but still modern, wrought iron accents as well as antiques.

Having a shed somewhere on the property will also bring in more money. In addition, accessory dwelling units (ADUs) are still popular. Combining the two also works great. Buyers are paying more for properties with sheds converted into living space. Notably, this actually doesn’t translate to a quicker sale – for one reason or another, homes with sheds stay on the market longer, despite selling for more. If you do want to sell quickly, some inexpensive upgrades that will accomplish just that are doorbell cameras, heat pumps, and fenced backyards.

While construction rates have been low overall since the pandemic, construction rates can potentially vary significantly depending on the type of building you’re looking at. This can be the result of different levels of demand or zoning regulations. Recent zoning reforms have tried to push construction more towards multi-family residences, believing that zoning is the primary obstacle.

However, if recent numbers are any indicator, there simply isn’t much demand for multi-family residences. Construction starts on buildings with five or more units dropped by 6.7% in March. Permits for such buildings also fell sharply, by 24.3%. At the same time, construction of single-family residences (SFRs) increased by 2.7%, and SFR construction permits increased by 4.1%. Overall, construction starts dipped down 0.8% and permits decreased by 8.8%.

Even though this wasn’t the goal of the zoning reforms, not everyone sees this as a bad thing. SFRs being in higher demand could signal that more people are ready to buy as opposed to rent. However, since it’s not renters but potential landlords that would create demand for multi-family residences, it’s also possible that homeowners simply aren’t seeing the value in renting the units out, leaving potential tenants in the dust.