During the summer, many people want to gather with friends and family, but they’re not sure where to get together. Here in California, that can even extend into the early fall, which often is just as hot if not hotter. But you don’t need an event planner to figure it out. If you have a back yard, use that. It just takes a bit of preparation and a focus on comfort.

Minimize your time fiddling with setup so you can maximize your time with friends and family. Prepare food ahead of time and make it something self-serve. Food-wise, that could be finger foods, tacos, do-it-yourself burgers, or a salad bar. Use buckets filled with ice for drinks so guests can help themselves while you enjoy the party. Have a music playlist ready that lasts the duration of the event so you aren’t hovering over your phone. Keep the volume high enough to provide energy but low enough that people can still chat and neighbors aren’t annoyed.

Be aware of the time and weather. If it’s extremely hot and sunny, have sunscreen on hand and perhaps a few strategically placed electric fans both to keep guests cool and deter pests. Remember that even in summer, the temperatures might drop towards the evening, so have a few lightweight blankets on hand. Also keep in mind that while most people think of sunny days in the summer, summer can also bring rain in some areas, so you should have a contingency plan in place. When it starts to get dark, avoid harsh overhead lights and instead make it cozy, comforting and ambient. String lights across the fence, solar lanterns along pathways or candles on the tables will all help to create a warm, intimate glow that transitions perfectly into the evening.

A proof of funds (POF) letter proves that the buyer has the cash needed to close the sale. This may be required in addition to providing a seller a loan preapproval letter. Having stable enough income and credit to be able to get a loan doesn’t necessarily mean the buyer has ready cash.

Once you get preapproved for a loan, get your POF letter as soon as possible. Presenting a POF usually occurs early in contract negotiations so it can provide additional strength to your purchase offer. Proof of funds can be evidenced with a simple letter from your bank, bank statements or proof of an open line of credit. A letter from your bank needs to have the name and address of the bank and a signature from an authorized employee.

This is also the case for an all-cash transaction. Having the ready cash to buy doesn’t imply that you have the additional cash saved up to pay closing costs. In fact, a POF letter is often required for short-term investors such as house flippers, who often pay cash so they aren’t saddled with loans after the property is sold.

If you’re preparing to view houses in search of your new home, don’t forget the importance of looking beyond simple first impressions. You’ll need to pinpoint any issues that could affect the property in the long run earlier rather than later, saving you time, money, and a potentially wrong decision.

Keep in mind that what you’re looking for is issues that can’t be changed or are costly to change. You may not like how the current owners have decorated, but that can be changed easily. In many cases, that furniture and those decorations won’t be there when you move in anyway. Instead, look at the home’s layout, lighting, and structure.

Pay attention to damage. Past water damage, even if the issue has supposedly been resolved, isn’t necessarily just an isolated event. It could signify recurring plumbing issues. The owners might not even be aware of difficult to notice signs such as paint peeling or small damp spots. A bad smell is also a big indicator that there might be issues with drainage or mold. In addition, make sure to look out for cracks in the walls. Tiny cracks might not mean much right now, but they could grow, and large cracks signal structural issues that could be nearly impossible to fix later.

While it’s possible to repair windows, it’s quite expensive to do so. Make sure windows open and close properly to keep the house free of drafts and properly insulated. This also helps to regulate humidity, as well as energy efficiency and lowering bills. Damaged windows aren’t necessarily a dealbreaker, but it’s a cost that needs to be factored in.

August is here already, and it’s been a hot summer of crazy good music! Thanks to everyone who continues to go to live shows and support musicians who work so hard to bring their extraordinary talents to stages all over southern California!

Speaking of amazing shows, last months show at Project Barley was off the charts fantastic! A standing room only crowd of dedicated blues/roots lovers were in the house to listen to Teresa James and the Rhythm Tramps and the Brophy Dale Band! Plus it was great to see blues DJ Gary Wagner come on out to the show to cheer on these two bands! “Thank you,” to Teresa and the Tramps, Brophy and his band who gave 200%! Also big thanks to everybody who generously donated to the musicians, Corrine behind the bar and the always cool, Woodrow dialing in the sound! For pictures of the night scroll down see jodisiegel.com.

This month will be another show not to be missed! Bernie Pearl is a legendary traditional blues guitar artist who has shared stages with Lightnin’ Hopkins, Fred McDowell, Big Mama Thorton and Freddie King to name only a few. He is a master slide player, musicologist and teacher and we are honored that he is playing an intimate set on this hot August night!

Harmonica/guitar player Gary Allegretto has had a storied life as a blues/roots player as well as a folk/country storyteller musician. He is also a local legend here in the south bay and his solo sets are rocking, entertaining and always soulful! For more info on him go to https://www.garyallegretto.com/

Blues/jazz you name it guitar player and San Pedro icon, Chuck Alvarez, has played with a who’s who of a variety of musicians-including Michael McDonald, The Emotions, Tim Weisberg to name only a few…he is bringing his blues band to the party! For more info on Chuck go to https://chuckalvarez.com/

Project barley and pizza kraft serves excellent food (gourmet pizza, wings & salads), wine, and award winning beer and cocktails too! Food served till 8:30pm. No reservationshttps://projectbarley.com/ 2308 Pacific Coast Hwy, Lomita, CA 90717

Fri, Aug 21, 2026 8:30 PM DJ & Doors 8:30 PM Tickets

Formed in 2008, Betty’s Mustache blends hip hop, rock and cumbia with a dark, edgy twist. Their traditional Latin grooves and punk rock attitude are inspired by their lost loved ones and incorporate hints of ’80s funk band Zapp and Roger. Cousins Jon and Martin are joined by Alex (conga) and David (bass). They regularly play at restaurants and bars around Los Angeles, including Las Perlas DTLA and Hello Stranger.

DJ 8:30 PM, Betty’s Mustache 9:30 PM.

All ages event.

LA Waterfront Pizza Pop-up at the Annex

They will be selling wood-fired pizza during Cumbia Night! Starting at 8:30 PM until sold out!

Come early to the show! You will be met at the door by Shag actors and welcomed into their tiki cocktail party.

Let’s Shag!

The one and only SHAG himself will be at every show of this murder mystery musical set at a Tupperware party! “Shag with a Twist” serves up an evocative cocktail of vibrant music and performers that brings to life the art of Shag when pupu platters and bouffants were all the rage. Guests are encouraged to come dressed in their finest tiki, pin-up girl style or 60s Mod attire and join the party.

This event is produced by Shag with a Twist Productions.

“The Blues is a Story” by Bluesman Bernie Pearl assembles another all-star blues showdown with guest Boogie Woogie Hall of Famer, pianist Carl Sonny Leyland, Tracey Hart (vocals), Kee Eso Pitchford (vocalist/guitar) and RJ Mischo (harmonica) with band members Ray Bailey (guitar), Elizabeth Hangan (bass) and Albert Trepagnier Jr (drums, vocals). Presented with support from Creative West & The National Endowment for the Arts.

The Doors Tribute by Peace Frog – Based out of Venice, California, this highly acclaimed act recreates the magic, intensity, and rock theater of Jim Morrison and The Doors. Mystical and hypnotic, the band transforms any room into an actual Doors concert experience. Lead singer Tony Fernandez lives out every move of Jim Morrison on stage and delivers a powerful recreation of true likeness in his presence, vocals, and spirit.

The four-piece band also includes James Sinigalliono on keyboard and bass, Tyler Thigpen on guitar and Tom Gold on drums. Hear intoxicating renditions of “Hello, I Love You,” “Light My Fire,” “L.A. Woman,” “The End” and many more Doors classics.

Alice Howe & Freebo – Rock Bass Legend Freebo (CSNY, Ringo Starr, Bonnie Raitt, SNL, The Muppet Show) and International Acoustic Music Awards Winner, Alice Howe deliver sparkling and soulful Americana.

Come early to the show! You will be met at the door by Shag actors and welcomed into their tiki cocktail party.

Let’s Shag!

The one and only SHAG himself will be at every show of this murder mystery musical set at a Tupperware party! “Shag with a Twist” serves up an evocative cocktail of vibrant music and performers that brings to life the art of Shag when pupu platters and bouffants were all the rage. Guests are encouraged to come dressed in their finest tiki, pin-up girl style or 60s Mod attire and join the party.

This event is produced by Shag with a Twist Productions.

Honey Whiskey Trio invites you to experience a spellbinding blend of a cappella vocals, classic folk ballads and Americana tunes backed by body percussion, guitar, banjo and mandolin.

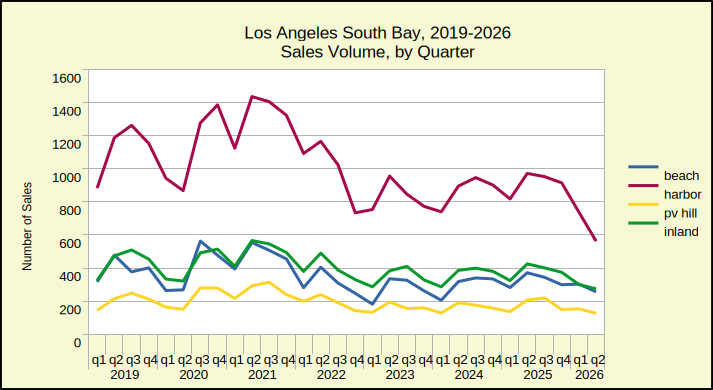

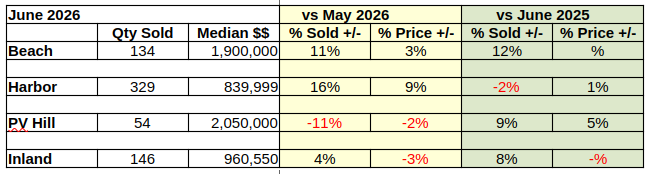

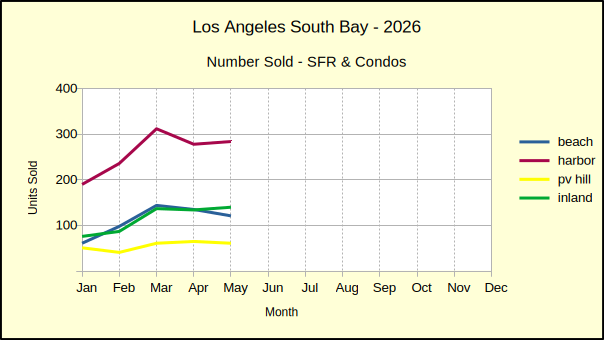

Half way through the year, June brought a 5% drop in year-to-date sales for the Los Angeles South Bay residential market. Only in the Beach area did sales exceed the first six months of 2025. With 693 homes sold at the Beach in the first half of 2026, compared to 653 for the same period in 2025, sales were up 6%, in comparison to the South Bay as a whole.

While the Beach was enjoying a year-to-date improvement, Harbor area sales volume dropped 10%, falling from 1790 homes last year to 1629 this year. In the same time frame, sales volume on the PV Peninsula declined from 342 properties sold in 2025 to 333 in 2026, for a 3% fall. Running a very similar decline of 4%, the Inland area fell from 749 to 720 sales.

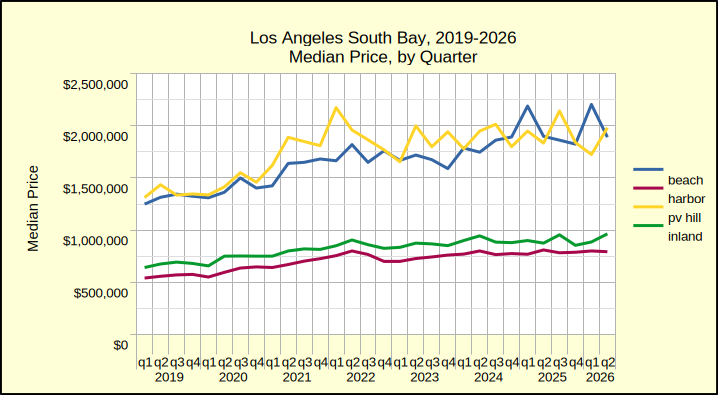

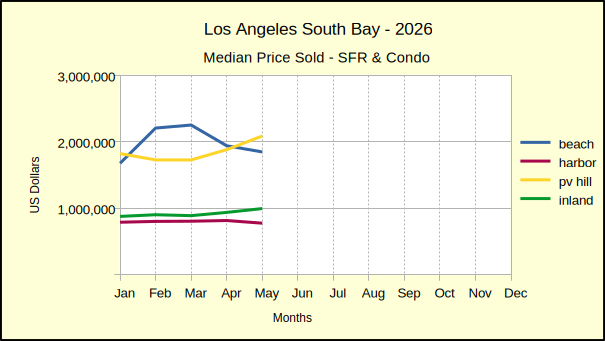

Comparing median prices from the first half of 2025 to the first half of 2026 the Beach came in with a 5% drop. It was closely followed by the Hill which fell by 3%. Both the Harbor and the Inland areas continued to show growth in the median price, with the Harbor at 1% and the Inland area at 3%.

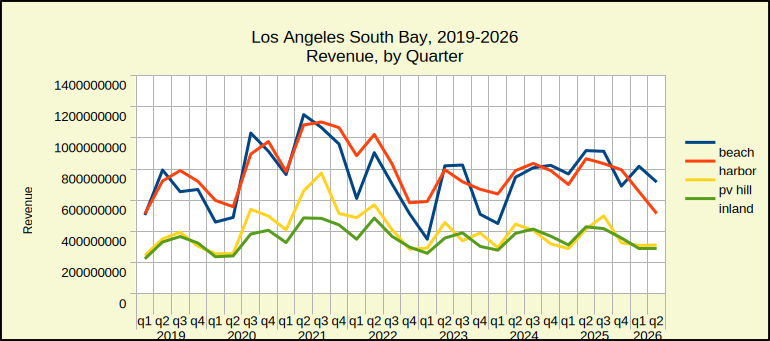

The Harbor and Inland areas are the largest market areas, easily surpassing the sales volume of the Beach and Hill. At the same time they sell for prices that average significantly less than their counterparts.

The Outlook

Anecdotally, sales volume and median price have an inverse relationship. When the number of home sales in an area falls repeatedly, it’s an indication the median prices will soon be falling. With the exception of the Beach cities, year-to-date, the region showed declining sales volume.

For the same six months, the median price has continued to fall at the Beach and on the Hill. The Harbor area has managed to stay on a growth path. The Inland area has, as well, but has seen a lot of negative price movement with three of the six months at or below zero.

The first half the year already shows declining sales and declining median prices, It seems safe to assume the second half will continue along the path. However, inflation is pushing interest rates, even while war is driving more inflation. Buyers are challenged to qualify at new rates causing inventory to continue growing. More and more often, sellers find it necessary to lower prices as life changes force them to move.

At least in the short term one can expect further slippage in sales volume, including the premium neighborhoods which often escape slow markets. That slowdown in sales would normally feed a lagging decline in median price. This year that decline seems to be sputtering. The two largest markets, the Harbor and Inland areas, respectively saw 10% and 4% declines in sales year over year. In the same half year they both maintained a 1% and 3% increase in median price.

If the inflation rate, currently at 3.5% goes up to 4.25% as predicted for July, and ends the year at 4% per predictions, one can readily assume a smaller number of qualified buyers for local area homes. The natural consequence is a further decrease in sales volume. The median price will be impacted. When sellers must sell, the prices will drop, or the owner will convert it to a lease and it will leave the market.

At this point, about the best one can do is wish the Fed good luck with controlling interest rates.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

Dance night with SoCal’s blazing 4-piece punk-cumbia band.

DJ set at 8:30 PM, Cara Borracho at 9:30 PM.

All Ages event.

The Original Las Brisas Pop-Up

Our local family-owned Mexican restaurant, Las Brisas, will be selling tacos, burritos and quesadillas during Cumbia Night! Starting at 8:30 PM until sold out!

Cumbia Night ft. Betty’s Mustache

Fri, Aug 21, 2026 8:30 PM DJ & Doors 8:30 PM Tickets

Formed in 2008, Betty’s Mustache blends hip hop, rock and cumbia with a dark, edgy twist. Their traditional Latin grooves and punk rock attitude are inspired by their lost loved ones and incorporate hints of ’80s funk band Zapp and Roger. Cousins Jon and Martin are joined by Alex (conga) and David (bass). They regularly play at restaurants and bars around Los Angeles, including Las Perlas DTLA and Hello Stranger.

DJ 8:30 PM, Betty’s Mustache 9:30 PM.

All ages event.

LA Waterfront Pizza Pop-up at the Annex

They will be selling wood-fired pizza during Cumbia Night! Starting at 8:30 PM until sold out!

Come early to the show! You will be met at the door by Shag actors and welcomed into their tiki cocktail party.

Let’s Shag!

The one and only SHAG himself will be at every show of this murder mystery musical set at a Tupperware party! “Shag with a Twist” serves up an evocative cocktail of vibrant music and performers that brings to life the art of Shag when pupu platters and bouffants were all the rage. Guests are encouraged to come dressed in their finest tiki, pin-up girl style or 60s Mod attire and join the party.

This event is produced by Shag with a Twist Productions.

“The Blues is a Story” by Bluesman Bernie Pearl assembles another all-star blues showdown with guest Boogie Woogie Hall of Famer, pianist Carl Sonny Leyland, Tracey Hart (vocals), Kee Eso Pitchford (vocalist/guitar) and RJ Mischo (harmonica) with band members Ray Bailey (guitar), Elizabeth Hangan (bass) and Albert Trepagnier Jr (drums, vocals). Presented with support from Creative West & The National Endowment for the Arts.

The Doors Tribute by Peace Frog – Based out of Venice, California, this highly acclaimed act recreates the magic, intensity, and rock theater of Jim Morrison and The Doors. Mystical and hypnotic, the band transforms any room into an actual Doors concert experience. Lead singer Tony Fernandez lives out every move of Jim Morrison on stage and delivers a powerful recreation of true likeness in his presence, vocals, and spirit.

The four-piece band also includes James Sinigalliono on keyboard and bass, Tyler Thigpen on guitar and Tom Gold on drums. Hear intoxicating renditions of “Hello, I Love You,” “Light My Fire,” “L.A. Woman,” “The End” and many more Doors classics.

July is bringing the heat and the fireworks too! So much great music is coming to Rock, Rhythm & Rhyme this month and through the summer into the rest of the year!

Starting with two of my favorite Texas blues artists; Grammy nominated Teresa James and the Rhythm Tramps with the Brophy Dale Band and yours truly!

But first big hallelujah thanks to the wonderful Joey Delgado and his band: Herman Mathews, David B. Kelley and Jacob Marquette! They blew the roof off and everybody left with a smile last month! Big love and thanks to all who continue to come to these shows! We are so grateful for you all!

This Tuesday is gonna be epic!

Teresa James is a powerhouse of a singer and keyboard player! She has worked with everyone from Randy Newman to Walter Trout and Delbert Clintonia and too many to mention in-between! She’s a first call session singer and her band is made up of some of the finest players in Los Angeles; Terry Wilson (bass/songwriter/producer), Billy Watts (guitar) and Richard Milsap (John Fogerty)!! Just some real deal rocking roots blues music that cannot be denied! To learn more about Teresa and her music go to:

Brophy Dale – has worked with rockabilly legends like Lee Rocker (Stray Cats), Scotty Moore and countless other blues bands throughout Los Angeles and beyond. He’s a world class guitar player with a magnetic stage presence! Cool songs with grooves that make ya wanna dance and sing! His band will feature the great Dave Gore on bass and TC Markle on drums.

A quitclaim deed is one type of legal document used for transferring property from one owner to another. But unlike most property transfer deeds, it doesn’t make the grantor liable for any future actions against the title to the property. It transfers all the assumed ownership rights from the grantor to the grantee but with no assurances as to what the transferred property rights are. A quitclaim deed action takes very little time because a title search is not required, but this also means it comes with no guarantees that a property is free of liens or encumbrances.

Quitclaim deeds are most commonly used in family matters. A common use of a quitclaim deed would be to move property from one family member to another or into a trust. They’re also effective for simply removing a spouse from the title or a homeowner giving up the title in order to add a new spouse to the title. Alternatively, quitclaim deeds can be a simple way to clean up title errors by removing names that show up in title searches in error.

Investing in home security cameras is a good way to protect your peace of mind, but a camera is only as good as its vantage point. For a home security system to be effective, you don’t need to record every square inch, but you should be sure to cover the strategic choke points. Here are the high-priority zones to maximize your home protection.

The main entrances. A surprising number of intruders simply walk right through the front, back or side doors. Position cameras above these entryways, angled downward to capture clear facial features.

Ground-floor windows. Ground-level windows are vulnerable weak spots. Placing cameras with a wide field of view near these windows deters break-ins before they start.

The driveway. Vehicles are prime targets for nighttime theft. A sturdy outdoor camera equipped with strong night vision ensures your cars remain protected under a watchful eye.

Transitional spaces. Intruders must move through your home to find valuables. Placing indoor cameras in main hallways or stairwells guarantees you track their movement even if they snuck past an exterior lens.

Common living hubs. Central areas like the living room often house your most expensive tech, from televisions to laptops. Monitoring these high-traffic spaces keeps your highest-value assets covered.

Remember to keep personal privacy in mind. Keep cameras out of private spaces like bedrooms and bathrooms, and ensure your outdoor lenses do not point directly into a neighbor’s house or yard. Also, to get the best results, mount outdoor cameras at least eight feet high to prevent tampering, and angle them just below any exterior lighting fixtures to avoid blinding the lens.

Kelley Blue Book is a brand well-known for valuations of new and used cars. In partnership with True Footage, a home appraisal technology company, Kelley Blue Book will start providing valuations for homes as well. The public launch is expected in August in ten states: Arizona, California, Colorado, Florida, Nevada, North Carolina, Oregon, Texas, Utah and Washington. The plan is for Kelley Blue Book Homes to be available nationally in 2027.

Contrary to many other lead generation platforms, Kelley Blue Book Homes will charge agents a variable subscription fee based on market conditions and number of ZIP codes serviced, rather than a flat percentage of commissions. The expectation is that the agents using the service are more likely to be experts within their geographical area. For consumers, Kelley Blue Book Homes will be completely free to use.

It seems paradoxical to think stability and adaptability can both be important simultaneously — perhaps they’re two different strategies, but how can they come together? The reality is that sticking to what you’re used to doesn’t work in a constantly shifting industry, and adapting to changes doesn’t get you ahead unless there’s some baseline of predictability. Neither strategy works on its own, so the industry needs both.

For a long time, the multiple listing service has been the rock that agents rely on for cold, hard data. While this is still true, buyers and sellers also increasingly have access to this data. This shifts the narrative — buyers and sellers now rely less on agents for data, and more for the things that the MLS doesn’t tell you. This includes regulations, local trends, and insights drawn from experience.

This doesn’t mean the MLS isn’t important anymore. It’s still the source of all that data, and without it, agents, buyers, and sellers would all be lost. What it does mean is that success in the real estate industry — for both agents and their clients — relies more than ever on a deep understanding of local expertise. In also means communication between agent and client is both more important and also easier. A smaller gap in knowledge means the process is less of a black box for clients.

Last year, Google began partnering with HouseCanary — an AI driven real estate brokerage — for a pilot program to deliver real estate listings directly to viewers via simple Google searches. The pilot program was initially only available in eight major markets, but this summer, will be expanding to all fifty states.

Unlike standard Google searches, which take data from wherever they can be found, this data will be sourced directly from a multiple listing services to ensure as much accuracy as possible and comply with regulations. Not all MLSes are participating, though, so only data from participating MLSes will be available. Currently, these are My State MLS, California Regional MLS, and San Diego MLS, but Google and HouseCanary are hoping to get more on board.

The goal of this program is to increase discoverability. Right now, potential clients looking to buy or sell can find information about homes for sale via sites such as Zillow or Trulia, but these sites don’t direct them to an agent — or if they do, it’s an agent that paid these companies to promote them, not necessarily the agent with the relevant listing. With this program, there will a button allowing searchers to directly contact the listing agents.

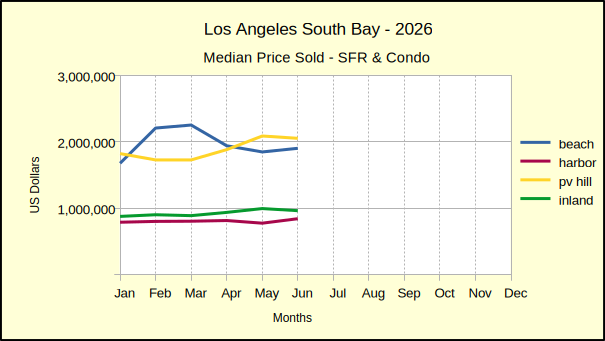

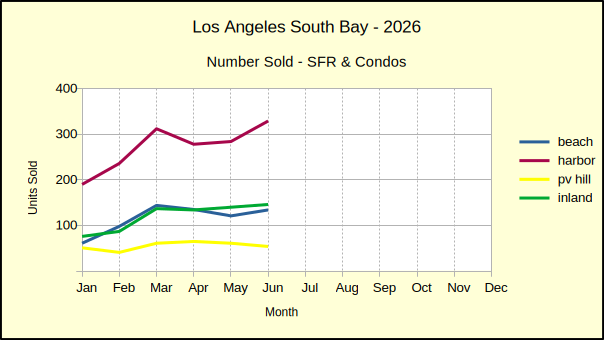

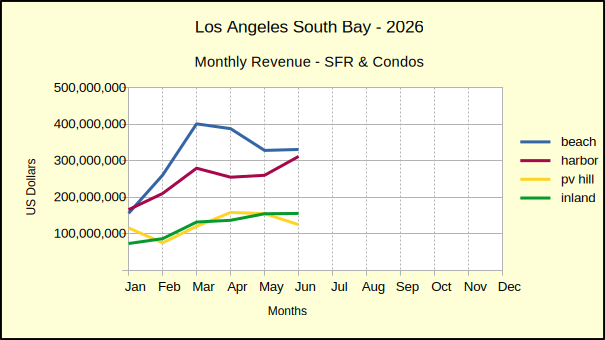

May brought slight improvement to the real estate market in the Los Angeles South Bay. Activity in the number of homes sold compared to April was off 1% across the region, after being down 6% the prior month. After a disappointing 32% drop in January, February and March had rebounded with steep monthly increases in sales. Since then, the war drums sounded in west Asia and sales volume across the South Bay has experienced a significant decline.

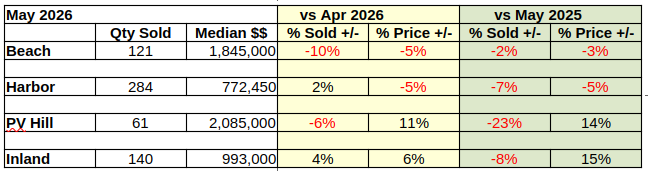

Monthly median prices have continued last month’s negative cast. For example, April and May at the Beach were down 14% and 5% respectively. The Harbor area showed mixed results, ending with a 5% decline in the median price for May. The Inland area is showing solid 5%-6% median price increases in month to month calculations. Prices on the Hill have been positive for the past three months and came in at 11% this month. (As always, one should remember transaction volume on the Hill is low, so a couple of sales can have an out-size impact on the statistics.)

May 2026 vs May 2025

Annually, the number of homes sold dropped in every area of the South Bay. Declines ranged from 2% off at the Beach to 30% off on the Hill. Across the region, year over year sales volume fell 9%. This pattern of decline roughly mirrors the month to month sales activity so far in the second quarter of the year.

Median prices continued to be volatile in May by comparison to the same month last year. The Beach cities once again fell by 3%, just as it did in April. The Harbor area fell 5%, flipping from a 4% gain the prior month. Values in the Inland and Hill areas increased for the second month in succession, this time by 13% and 12%, respectively.

2026 Year to Date vs 2025

Residential sales volume has been on the decline most of this year, in most areas of the South Bay. During the first five months of the year, 2712 homes have sold compared to 2895 for the same period in 2025. As it was last month, this measures out to a 6% decline for the year to date.

The Beach was the only area to show positive growth in May sales with a 4% increase in volume. The largest decline came in the Harbor area with an 11% drop in sales. The Palos Verdes and Inland areas dropped 5% and 7% respectively.

While there have been many instances of decline in median price, the cumulative year to date statistics are still relatively positive. The Beach and Harbor areas both show a 2% increase in the median. At the same time, the median price on the Hill dropped 5%, while the Inland area increased 1%.

The Outlook for June

Home sales for June are projected to continue dropping. Expect month over month declines to be 1% to 2% lower than in May. Annually, sales are anticipated to drop by about 10% compared to last June. Year to date sales are also expected to drop by about 10%.

Continued decline in the number of homes sold will almost certainly impact the median price. Despite historically low inventory, the volatile economic situation has dampened buyers’ enthusiasm. Rather than the “bidding war” environment often seen with low inventory, the current market is watching widespread seller price reductions.

Anecdotal evidence shows some homeowners selling and shifting to a rental in anticipation of recession. These sellers are hoping a market collapse will create an opportunity to profit by buying back into the real estate market after prices collapse. While quite risky, this method started several investment careers during “the great recession.”

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

Many people look to their friends and social media for inspiration for home decor, as well as personal style. Then they take bits and pieces of what they find, try to redecorate or reinvent, but find that it still doesn’t look right. The problem is that other people aren’t you.

That doesn’t mean you should ignore your inspirations. But it does mean that you need to figure out why they appeal to you. What do the styles that interest you have in common? Once you figure this out, don’t just borrow the interesting bits. That’s not a coherent style. Build your own. Try creating a moodboard that represents you.

Also remember that this is only one step in the process. You’re not going to find the perfect fit immediately, and may need to swap things out multiple times. This is especially true if you’re looking to redecorate your home as well as reinvent yourself. You’ll need to keep in mind wall colors, accents, and decor type, as these can all affect your home’s value down the line.

The theme of this year’s event is “Roots and Family”. Flamenco is a folk art form that originated in the Andalusia region of southern Spain, and the Romani, a migratory people, played a major role in its history and development. Family traditions still form the core of the Roma culture.

As an art form created by wandering peoples through a fusion of various music and rhythms, it resonates with a diverse range of people, bringing familiarity, nostalgia, and melancholy; in 2010, it was included in UNESCO’s list of Spain’s Intangible Cultural Heritage.

We are honored to be able to present this wonderful culture to you on stage through the art of flamenco, an art we feel passionately about. You will be able to enjoy a wide range of flamenco performances, from brilliant dances with castanets, fans, and mantons, which are typical flamenco accessories, to cante and guitar performances! Through this recital, you will enjoy a dreamy moment to immerse yourself in the passion of flamenco and free your spirit.

Artistic Director: Mikaela Kai Special Guest Artists: Paco Arroyo, Yolanda Arroyo Guest Artists: Maribel Aja Villaseñor, Ron Wagner (Percussion) MFK Dancers: Yoko Shibata, Yumi Fujimoto, Yoshikuni Okita, Laura Gonzales, Reiko Taira, Hitomi Watanabe MFK Musicians: Klee Ando

Like the Gipsy Kings, Grammy-nominated guitar virtuosos deliver a night of world guitar influenced by Latin music and Flamenco with vocals and band.

Ardeshir Farah of Grammy-nominated guitar duo Strunz & Farah returns to the Annex. Putting a dynamic spin on classical guitar music, Farah integrates Afro-Caribbean, Latin American folk, flamenco and Middle Eastern rhythms.

Having shared the stage with musicians including Miles Davis, Bela Fleck and Bonnie Raitt, his versatility as an artist speaks for itself.

Luis Villegas is a Mexican American guitarist best known for his album Cafe Olé, which mixes new-age music, flamenco, and jazz and garnered a spot on the Grammy ballot for Best New Age Album of the Year in 1999. He plays a rapid-fire, finger picking style that adds spark to the duos’ energetic performance.

LA’s Premier 1960’s Music Revue! Led by Mark Kopitzke of The Nightcaps, this smooth, swinging ensemble takes you on a thrilling escapade through the swanky pop of the 1960s. Hear Mad Men era hits by Bobby Darin, Henry Mancini, The Association and more!

The Secret Agents were formed in 2018 with one mission: to bring the sounds of the ’60s back into the mainstream by celebrating the music of Bobby Darin, Mel Tormé, Henry Mancini, Lalo Schifrin,

Johnny Rivers, Chet Baker, Matt Monro, Horace Silver, Georgie Fame & The Flames, The Buckinghams, Mickey & Sylvia, Del Shannon, The Association, and so many more!

So put on that dinner jacket, pour yourself a drink, and let’s twist again like we did so very long ago.

Please contact the event producer for all questions.

SOLD OUT Andy & Renee & Hard Rain

Sat, Jun 27, 2026 8:00 PM Doors 7:00 PM

This show is SOLD OUT! If you would like to be put on the waitlist, please call the Annex at 310-833-4813. Placement on the waitlist does not guarantee a ticket.

MONDAYS in JUN (except 6/22) @ 6:00PM — 8:00PM (PDT, UTC-07) The Lighthouse Huntington Beach, 21022 Pacific Coast Hwy Ste B 230, Huntington Beach, CA 92648

Andy & Renee-The Lighthouse

TUESDAYS@5:30PM — 7:30PM (except 6/16) The Lighthouse Cafe, 30 Pier Avenue Hermosa Beach, CA 90254 310 376-9833

Andy & Renee-Banana Leaf

THURSDAYS @6:30PM — 9:00PM Banana Leaf & Beach Cities Social, 1408 S Pacific Coast Hwy, Redondo Beach, CA

Andy & Renee-Brews Hall Del Amo

FRI, JUN 5@ 8:00PM — 10:00PM Brews Hall Del Amo, 21770 Del Amo Circle East, Torrance, CA 90503

Andy & Renee- House Concert, Sunnyvale, CA

SAT, JUN 13 @ 4:00PM

Hosted by Gretchen & Rich Parenteau & Jane & Paul Ramirez. 22000 Regnart Rd. Cupertino, CA 95014. RSVP to reneesafier@hotmail.com. BYOB

Andy & Renee & Hard Rain-The Music of Bruce Springsteen-SOLD OUT!

SAT, JUN 27 @ 8:00PM The Grand Annex, 434 W. 6th St., San Pedro, CA 90731

Andy & Renee & Hard Rain-Malaga Cove Library Park Concerts

WED, JUL 8 @ 6:30PM — 7:45PM Malaga Cove Library Park, 2400 Via Campesina, Palos Verdes Estates, CA

Andy & Renee-Music With a Mission-Midnight Mission

THU, JUL 16 @ 2:30PM — 4:00PM Midnight Mission, 601 S San Pedro St., Los Angeles, CA 90014

Afternoon performance for the clients of the Midnight Mission. YOU are welcome too!

Andy & Renee-Brews Hall Del Amo

FRI, JUL 24 @ 7:00PM — 10:00PM Brews Hall Del Amo, 21770 Del Amo Circle East, Torrance, CA 90503

Andy & Renee & Hard Rain-Torrance Hot Summer Nights Concert In The Park

SAT, JUL 25 @ 5:00PM Wilson Park, 2200 Crenshaw Blvd., Torrance, CA 90501

Andy & Renee-The Moose Knuckle, Coolin, ID

THU, AUG 6 @ 6:00PM — 9:00PM Moose Knuckle, 10 Cavanaugh Bay Road, Coolin, ID 83821

Andy & Renee-House Concert-Priest Lake, ID

SAT, AUG 8 @ 6:00PM

Home of The Songstad’s, 632 Hagman Road, Nordman ID 83848. Hosted by Shannon Foley & Rick Lyman and The Songstad’s. BYOB & a chair/blanket

Andy & Renee-The Hills Resort, Priest Lake, ID

SUN, AUG 9

The Hills Resort, 4777 W Lakeshore Rd., Priest Lake, Idaho 83856

Andy & Renee-House Concert-Denver, CO

SAT, AUG 15

Details TBA

Andy & Renee & Hard Rain-Southbay Sunrise Rotary Club Event

SAT, AUG 22nd, 5-9pm (music 4-7pm) Torino Plaza, Torrance Cultural Arts Center, 3330 Civic Center Drive, Torrance, CA 90503

This is a once a month (every third Tuesday) show that is designed as a listening room for world class songwriters, many with hit songs, long touring/recording associations with music legends ETC… to play their original music in an intimate setting. $20 SUGGESTED DONATIONS AND GO TO MUSICIANS. Project Barley serves excellent Food (Gourmet Pizza, wings, salads), wine, and award winning beer. Food served till 8:30pm. No reservations so arrive early to get a table. This month we are proud to present: THE DELGADO BROTHERS AND JODI SIEGEL

The Delgado Brothers

The East L.A. natives have been performing in their current incarnation since 1984, but the musical roots of three siblings – brothers Steve, Joey and Bobby (abetted by fourth member David Kelley) – stretch back nearly half a century. They have toured all over the world, won numerous awards for their band and Joey Delgado’s guitar playing, have written great songs that infuse Latin, soul and blues with socially relevant lyrics and driving grooves! All four of these brothers are solid soulful musicians who have been playing as a band for over fifty years! They are legends in their own communities, but also legends throughout Southern California and far beyond that.. Joey Delgado is without question one of the best blues guitar players in the world! He has graced the stages with countless other blues/soul performers and when he digs into the blues his energy is contagious!! Steve Delgado is a masterful singer and groove king on the drums…their songs are instant classics of the genre…a mix of Latin/Soul and blues!

Jodi Siegel

Jodi Siegel, originally from Chicago, IL, is a singer, songwriter and guitarist. Over the years Jodi has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and countless others. Her songs have been recorded by Maria Muldaur, Marcia Ball, Tommy Ridgley and Teresa James.

She has recorded two CD’S; Stepping Stone and her latest CD, “Wild Hearts,” produced by Steve Postell (Immediate Family, David Crosby, Eric Johnson, Robben Ford, Iain Matthews), is filled with great songs, cool grooves, intimate, smart lyrics and some of the best of the best musicians in Los Angeles today including; Mike Finnigan (organ, piano), Hutch Hutchinson, Abe Laborial Sr., Alphonso Johnson (bass), Russ Kunkel, Michael Jerome Moore, John Ferraro, Arno Lucas (drums, percussion), Joe Sublett (Saxophone) and Maxayne Lewis and Clydene Jackson (background vocals). Each song has a soulful delivery with an undeniable down-home elegance. It has received great reviews by Patrick Simmons (Doobie Brothers), Maria Muldaur, Walter Trout, David Mansfield (T Bone Burnett), Leland Sklar, Mike Finnigan and Doug Macleod to name a few.

Jodi is in the pre-production stage of recording a new record with Grammy winning producer/drummer (Taj Mahal) Tony Braunagel.