When a buyer and an agent enter into an agreement for the agent to represent the buyer in the purchase of a home, that agreement is called a buyer agency agreement. A buyer agency agreement usually spells out the duties the agent has towards the buyer in finding and closing on a home.

It is important for the buyer to make sure the right conditions are outlined in the agreement. The buyer can participate in negotiating the terms of the agreement, and the buyer has no obligation to continue working with the agent if the agent is not performing per the agreement.

Buyer agency agreements have typical term lengths of 90 days but can be negotiated for any length. A buyer can specify the kind of property being sought so the agent keeps on track during their search. The terms of the agent responsibilities should also include negotiating on behalf of the buyer and making sure the sales transaction successfully closes.

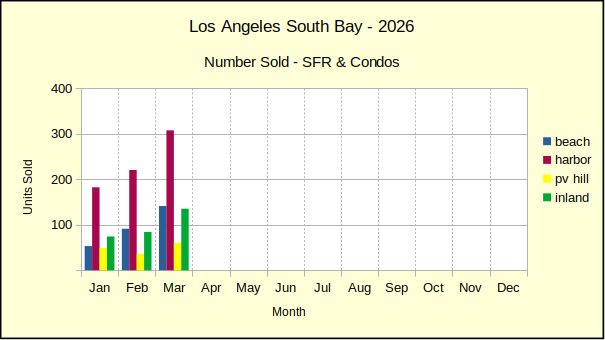

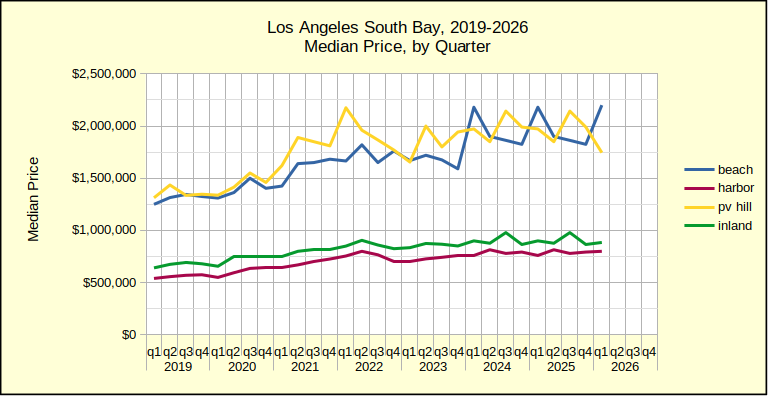

The first quarter of 2026 is complete now and it’s time to take a look at how sales volume and median prices compare month to month and year over year. Typically the number of homes closing escrow picks up as the holiday season passes and spring arrives. The median price, on the other hand, seems to depend on ever more factors with each following year.

Month to Month

As usual, January was even slower than December with a 35% drop in the number of sales recorded. This year February, with 20% more sales than January, was a little slower than usual. In an unexpected showing of strength, March has made up for some of the decline during the weak winter months, posting a 49% increase over February.

Sales volume was up across the South Bay, with the PV Hill and the Inland area posting the highest monthly increases at 67% and 61%, respectively. The Beach area came in third with a 55% growth in sales, followed by the Harbor area at a 40% increase in sales

Monthly median prices stumbled again in March, becoming increasing flat. On the negative, there was a 4% drop in median price for the Inland area. Closing prices on the Palos Verdes Peninsula barely made the mark posting a 1% increase over the February median. The other two areas were positive, though the increases were so small they registered as zero in the charts. The wars in West Asia may be having a short term effect. On the other hand, the slowdown in median prices may be the beginning of price corrections.

Year to Year

The year over year perspective came with a more nuanced set of numbers and some surprises. As a whole, sales volume in the South Bay ranged from a 16% decline in home sales for January to a 19% decline in sales for February, before reversing course with a 20% jump up in March. Those March increases ranged from 17% in the Beach Cities to 21% at the Harbor. All good, solid increases in the number of homes sold.

The most dramatic shifting came in comparing median prices this year to last year. The Beach area has suffered the greatest swings. After struggling in January with a 29% decline in median price, followed by a mere 1% increase in February, the Beach area claimed a 10% increase in the March median.

The Beach was the only growth area for median price. The Harbor area fell from a solid 5% increase for both January and February to a 0% negative in March. At the same time, the PV Hill showed a 12% drop in pricing and the Inland area fell by 3%.

The statistics tend to support the price correction theory. As the quarter has progressed, median sales prices have slipped below the highs of last year at least once in all the areas.

Year to Date

In summary, the first quarter of 2026 has been markedly less positive for real estate in the South Bay than in 2025.

Overall sales volume has dropped 4%. Declines ranged from 3% at the Beach to an 8% drop at the Harbor. The PV Hill was the only area trending positive, with a 13% increase in the number of homes sold. As always, one must consider the caveat of sample size. Because the volume of business on the Hill is comparatively tiny, small moves can look dramatic.

Median prices for the first quarter are also significantly down from 2025. The Inland area dropped 2% while the Hill fell by 12%. The Beach cities eked out a 1% increase and the Harbor area showed a solid 5% increase in the median. This is a distinct shift from what has been happening in recent years. The Beach cities have been the predominant leaders in median price apprectiation, leaving the Harbor and Inland areas behind.

Stats for Nerds

Beach:

M-m, vol: 141, 55%, med: 2,200,000, 0% y-y, vol: 17%, med: 10% ytd, vol: -3%, -10% from 2019, med: -1%, up 76% from 2019

Harbor:

M-m, vol: 307, 40%, med: 800,000, 0% y-y, vol: 21%, med: -0% ytd, vol: -8%, -20% from 2019, med: 5%, up 33% from 2019

Hill:

M-m, vol: 60, 67%, med: 1,744,932, 1% y-y, vol: 20%, med: -12% ytd, vol: 13%, 1% from 2019, med: -12%, up 33% from 2019

Inland:

M-m, vol: 135, 61%, med: 885,000, -4% y-y, vol: 18%, med: -3% ytd, vol: -4, -10% from 2019, med: -2%, up 38% from 2019

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

A recorder performance by local fifth graders – for the community!

Grand Vision Foundation’s Meet the Music students from local partner schools will show off what they have been learning all semester. Grand Vision’s Recorders in Schools program provides trained teaching artists to classrooms to lead weekly music classes during the school day. Students learn to play an instrument, read music and perform. This program also incorporates music into history, culture and math!

This performance is free and open to all, no tickets or RSVP required.

ARTS OPEN Grand Annex Art Saloon

Sat, Apr 25, 2026

3:00 PM – 8:00 PM

On Arts Open Weekend, Grand Vision with Findings Art Gallery invite you to the Grand Annex Art Saloon: An Art & Music Open House. Listen to live music as you explore the works of artist and instructor Betsy Lohrer Hall showcased alongside the unique installations of her Cal State Fullerton art students. Whether you’re an art aficionado, a music lover, or simply looking for an inspiring afternoon, the Saloon doors are open! No-host bar. Outside food is welcome.

Saturday Music

Adriana Nicole & Neo / 3:15 PM – 4:30 PM Jazz/bossa nova vocalist with bass accompaniment. Influenced by Billie Holiday and Ella Fitzgerald, Adriana recently released her first single, “In the World.” Neo is a seasoned bass player with over two decades of experience in global music tours.

Sean Lane / 4:45 PM – 6:00 PM Delta-style blues singer-songwriter, harmonica player and master slide guitarist.

Sunday Music

Bella & Rudy / 3:00 PM – 4:30 PM Dynamic acoustic duo known for their versatile pop-to-rock repertoire.

Chris Huff / 5:00PM – 6:00 PM Known for his Texas-tinged Americana covers and originals, Chris can often be found at local coffeeshops and festivals. With his daughter Emily, Chris emcees the monthly 1st Thursday Art Saloon at the Grand Annex.

Art Show Activation: Findings Art Center presents art activations by Betsy Lohrer Hall’s students from California State University, Fullerton.

Betsy Lohrer Hall makes process-oriented works on paper and installations. She earned her MFA from California State University, Fullerton and her BA from Colorado College. She studied art history, literature, architecture and theatre in London and Florence, and painting, briefly, at Parsons, New York City. Betsy has exhibited numerous times in San Pedro galleries, along the west coast of the US, in Thailand and Taiwan.

Henry Krusoe is serving as fINdings Gallery curator. He is an Otis College graduate and has been an Angels Gate Cultural Center resident artist since 2019, creating multimedia artwork spanning analog and digital formats.

Details

Date Saturday, April 25, 2026Time 3:00 PM – 8:00 PM

On Arts Open Weekend, Grand Vision with Findings Art Gallery invite you to the Grand Annex Art Saloon: An Art & Music Open House. Listen to live music as you explore the works of artist and instructor Betsy Lohrer Hall showcased alongside the unique installations of her Cal State Fullerton art students. Whether you’re an art aficionado, a music lover, or simply looking for an inspiring afternoon, the Saloon doors are open! No-host bar. Outside food is welcome.

Sunday Music

Bella & Rudy / 3:00 PM – 4:30 PM Dynamic acoustic duo known for their versatile pop-to-rock repertoire.

Chris Huff / 5:00PM – 6:00 PM Known for his Texas-tinged Americana covers and originals, Chris can often be found at local coffeeshops and festivals. With his daughter Emily, Chris emcees the monthly 1st Thursday Art Saloon at the Grand Annex.

Art Show Activation: Findings Art Center presents art activations by Betsy Lohrer Hall’s students from California State University, Fullerton.

Betsy Lohrer Hall makes process-oriented works on paper and installations. She earned her MFA from California State University, Fullerton and her BA from Colorado College. She studied art history, literature, architecture and theatre in London and Florence, and painting, briefly, at Parsons, New York City. Betsy has exhibited numerous times in San Pedro galleries, along the west coast of the US, in Thailand and Taiwan.

Henry Krusoe is serving as fINdings Gallery curator. He is an Otis College graduate and has been an Angels Gate Cultural Center resident artist since 2019, creating multimedia artwork spanning analog and digital formats.

Broadway’s Syndee Winters honors the legendary Lena Horne through a high-spirited one-woman theatrical performance. With her live band, Winters takes us on an electrifying theatrical journey from Horne’s Great American Songbook classics to hits from her own starring roles in The Lion King and Hamilton.

Inspired by the album Syndee Winters Sings Lena Horne, the evening unfolds through a series of musical performances, character portrayals, and imaginative storytelling. Syndee Winters embodies a cast of special guests – all portrayed by herself – who gather to honor Lena Horne and reflect on the many facets of womanhood, artistry, and resilience that Horne represented.

The musical program features beloved selections from The Great American Songbook, including signature songs associated with Lena Horne such as “Stormy Weather” and “The Lady Is a Tramp.” The evening also expands beyond the classics, weaving in contemporary musical selections that highlight both Syndee’s career on Broadway and how Horne’s influence continues to echo through today.

The show moves seamlessly between jazz standards, theatrical monologues, and playful backstage moments. The result is a sparkling homage to an icon whose elegance, courage, and artistic excellence helped shape American entertainment.

🍷 Pre-Concert Wine Tastings Led by JP Molinari: Free to Grand Vision members at the Friend, Champion, VIP Circle, Arts Advocate, and Performing Arts Patron level – up to two per household, $16 per person for all others. Concert tickets are required to participate. Members’ tasting tickets must be redeemed in advance. Tastings begin one hour before the show, please arrive no later than 30 minutes into the tasting to participate.

Whether you’re a longtime fan or just love live music, this is the perfect chance to kick back and enjoy The Villagers up close. With special solo supporting act Nicholas Miller! Don’t miss out on what’s sure to be a memorable night!

This event is produced by the Villagers. Please contact them with all event related questions.

SOLD OUT Bernie Pearl & Friends “My Kind of Blues”

Sun, May 03, 2026 4:00 PM Doors 3:00 PM This show is SOLD OUT! If you would like to be put on the waitlist, please call the Annex at 310-833-4813, placement on the waitlist does not guarantee a ticket.

LA-based blues legend Bernie Pearl and his guests: Dave Melton, RJ Mischo, Lester Lands, Jeffrey Paul Ross and Shy but Flyy, perform with an all-star backing band featuring Ray Bailey on guitar, Mo Beeks on piano, Elizabeth Hangan on bass, Albert Trepagnier on drums, and dancing master Chester Whitmore will also be joining the show.

Pearl is a foundational figure in the SoCal blues scene, launching his career during the Folk Music revival of the 1950s. His deep connection to the blues was forged at his brother’s legendary LA music-coffee house, The Ash Grove (opened in 1958), where he learned from and performed with masters like Lightnin’ Hopkins, Big Mama Thornton and Freddie King. In the late ’60s, Pearl started and hosted the LA’s first all-blues radio show “Nothin’ but the Blues” and founded the Long Beach Blues Festival.

SPECIAL GUEST DANCER: Chester Whitmore, a protege of Fayard Nicholas (Nicholas Brothers), has danced his way around the world. His choreography can be seen in music videos for Boys II Men, Sugar Ray, Teena Marie and he has worked with MC Hammer and Prince. He has performed with his dance company Black Ballet Jazz, the Duke Ellington Orchestra and the great Miles Davis.

GUEST MUSICIANS: Dave Melton is an absolutely stellar player of the blues on slide guitar. He was greatly influenced by Bernie Pearl’s radio show when he was starting out in the East LA Blues scene in the 80s. Melton’s slide guitar can be heard on the albums of Robert Lucas, the Delgado Brothers and Johnny Mastro.

RJ Mischo earned his chops with legends Percy Strother, Mojo Buford and Lazy Bill Lucas. RJ’s discography features chart-topping “King of a Mighty Good Time” and “Two Hours From Tulsa” and his albums Knowledge You Can’t Get in College and Make It Good, made the Top 50 in Living Blues albums of the year listings.

Lester Lands, a maestro of the blues, who grew up in the Mississippi Delta, has graced the stages across the globe. From high-energy performances with his band, The Delta Revelators, to a discography that boasts critically acclaimed albums, Lester’s dynamic presence leaves a lasting impression.

Jeffrey Paul Ross is an extraordinary, inventive, and astounding guitar player. He has recorded with the Hellecasters and the Asylum Street Spankers, as well as working with Candye Kane, Rosie Flores and Kelly Willis. He is also know for his work with Rank and File, James Harman and William Clarke.

Shy But Flyy is a rising blues, jazz, and spoken-word artist. Shy started out releasing mixtapes and writing hooks for artists. After an internship at a major record label and hosting “Flyy Radio,” she found the blues scene. Shy has headlined The Uptown Jazz festival, The New Blues Festival and Temecula So Cal Blues Fest.

THE ALL-STAR BAND Ray Bailey was taught by the groundbreaking reed player John Carter. Under his tutelage, Bailey learned Charles Mingus, Don Cherry, Stravinsky, and Mozart. He was inspired by the (then) youngster Jimi Hendrix, Larry Davis, and Chaka Khan. He regularly performed at the famous LA blues club Babe’s & Ricky’s Inn.

Mo Beeks is one of LA’s favorite pianists, singers, songwriters and musical directors. A Grammy nominee, He plays a variety of styles and is a carrier of the blues tradition. He has performed with Leroy Hudson, Chaka Khan, Tyrone Davis, Otis Clay, Mahalia Jackson and more

Elizabeth Hangan is a singer, songwriter, bassist and educator. She fronts The Elizabeth Hangan Band, performs with Marguaret Love’s Lovettes and toured with Bobby Warren, Mickey Champion, and Deacon Jones. She performed in the Women in Blues ’21 showcase and was presented with a Living Legend Award in 2018.

Albert Trepagnier, Jr., AKA “the Beat-Man,” is a New Orleans-born drummer and vocalist. He’s played with Bernie Pearl for over 40 years. He has also played for Eric Clapton, BB King, John Mayall and Stevie Ray Vaughn. He is a recipient of the Living Legend Blues Award.

SPECIAL BOOK SIGNING:

After the concert, head over to PM Sounds (across the street from the Annex at 421 W 6th Street) for a special book signing event with Bernie Pearl. Bernie Pearl will be signing copies of his autobiography Sittin’ on the Right Side of the Blues. In this biography, Bernie describes his experiences working to promote the Blues in Los Angeles. His anecdotes provide insight into the personal side of the Blues musicians involved in his story. This book includes mini-biographies of important blues figures, photographs and other historical documents, many of which have never been previously published.

The Grand Annex Art Saloon

Thu, May 07, 2026 5:00 PM – 8:30 PM Doors 5:00 PM

Enjoy a laid-back evening of music and art at this new First Thursday event, featuring art by fINdings Art Center.

fINdings Art Center, in collaboration with Grand Vision’s Annex Arts Saloon, presents artworks curated by Henry Krusoe.

Henry Krusoe is an Otis College graduate and has been an Angels Gate Cultural Center resident artist since 2019, creating multimedia artwork spanning analog and digital formats.

Often compared to Old Crow Medicine Show and The Avett Brothers, this trio is gaining national attention for their foot-stomping mix of rock, folk, bluegrass, vintage swing and witty songwriting. Singer-songwriter sibling duo, Sunflower Academy opens the show with their original blend of catchy melodies and powerful vocals.

Max Capistran, Sasha Dubyk, and Avery Ballotta are Damn Tall Buildings. The trio that has spent over a decade creating their signature floor-stomping mix.

Honoring Former LA City Councilmember Joe Buscaino

The 17th Annual Gathering for the Grand Gala will be on May 16, 2026 at the Palos Verdes Golf Club. Together, we’ll toast to the next exciting phase of renovations at the historic Warner Grand Theatre and celebrate sixteen incredible years of concerts at the Grand Annex Music Hall. The theme is: Fly Me to the Moon. At the gala, we will be honoring former LA City Councilman Joe Buscaino, a native of San Pedro, who has been a champion of Grand Vision and the Warner Grand Theatre for many years. He was instrumental in launching the Warner Grand Theatre’s current major renovation during his time in office.

Dress: Mid-century Vegas, with a Sinatra twist

Proceeds benefit live music at the Grand Annex Music Hall; Meet the Music, our music education program serving 2,500+ Harbor area students annually; and restoration of the historic Warner Grand Theatre.

POLAHS Senior Showcase Visual & Performing Arts

Sat, May 23, 2026 5:00 PM

The senior class of Port of Los Angeles High School Visual and Performing Arts Curriculum return to the Grand Annex with an exciting and eclectic mix of music, dance, drama, and video.

This coming Tuesday is gonna be an extraordinary show with two outstanding duos who are new to the Rock Rhythm and Rhyme stage, but seasoned veterans in the los angeles and beyond music community! We are proud to present the fun and eclectic southwestern gypsy soul folk sounds of Nathan & Jesse and the hauntingly captivating indi folk music of Petty Chavez. I’m a huge fan of them both! I’ll be doing some new tunes and looking forward to sharing those with you all too!

As usual, get there early to reserve your seat! $20 donation suggested! Please bring cash and or i’ll have a qr code that you can venmo the musicians!

Project barley and pizza kraft serves excellent food (gourmet pizza, wings, sandwiches, salads), wine, and award winning beer and cocktails too! Food Served till 8:30pm. No reservationshttps://projectbarley.com/ 2308 Pacific Coast Hwy, Lomita, CA 90717

TUESDAYS@5:30PM — 7:30PM The Lighthouse Cafe, 30 Pier Avenue Hermosa Beach, CA 90254 310 376-9833

Andy & Renee-Banana Leaf

THURSDAYS @6:30PM — 9:00PM Banana Leaf & Beach Cities Social, 1408 S Pacific Coast Hwy, Redondo Beach, CA

Andy & Renee-Brews Hall Del Amo

FRI, MAY 1 & JUN 5@ 7:00PM — 10:00PM Brews Hall Del Amo, 21770 Del Amo Circle East, Torrance, CA 90503

Andy & Renee-King Harbor Yacht Club

(members & their guests only) FRI, MAY 8 @ 6:00PM — 9:00PM King Harbor Yacht Club, 280 Yacht Club Way, Redondo Beach, CA 90277

Andy & Renee & Hard Rain & Friends – 36th Annual Dylanfest

SUN, MAY 24, 2026 @ 12:00PM — 8:00PM Torino Plaza, Torrance Cultural Arts Center, 3330 Civic Center Drive, Torrance, CA 90503

Hosted by Andy & Renee & Hard Rain, Dylanfest is the South Bay’s longest-running music festival—a heartfelt celebration of the songs and spirit of Bob Dylan, one of America’s greatest and most influential songwriters. Tickets available NOW!

Andy & Renee – House Concert, Sunnyvale, CA

SAT, JUN 13 @ 4:00PM Hosted by Gretchen & Rich Parenteau & Jane & Paul Ramirez. 22000 Regnart Rd. Cupertino, CA 95014. RSVP to reneesafier@hotmail.com. BYOB

Andy & Renee & Hard Rain-The Music of Bruce Springsteen-SOLD OUT!

SAT, JUN 27 @ 8:00PM The Grand Annex, 434 W. 6th St., San Pedro, CA 90731

Andy & Renee & Hard Rain-Malaga Cove Library Park Concerts

WED, JUL 8 @ 6:30PM — 7:45PM Malaga Cove Library Park, 2400 Via Campesina, Palos Verdes Estates, CA

Andy & Renee & Hard Rain-Torrance Hot Summer Nights Concert In The Park

SAT, JUL 25 @ 5:00PM Wilson Park, 2200 Crenshaw Blvd., Torrance, CA 90501

A small backyard doesn’t necessarily mean you’re limited with what to do with the space. You may not have the luxury that a larger garden has in terms of creating multiple zones, but there are still many ways to make the most of your yard, turning it into another inviting part of your home.

Some excellent yard features don’t take up much space. Flower gardens can simply border fences or sit in raised beds. You can also use climbing plants or wall-mounted planters. L-shaped seating is a natural fit for corner spaces, maximizing the space efficiency of your seating. Water features also don’t need to take up much space — even a small container pond will attract wildlife, making your backyard feel closer to nature.

Rather than make your yard feel larger than life, an alternative is to lean into the small size of your space to create a more intimate feel. You can dedicate a small yard to comfort with the right arrangement of items. A compact chair, a small table and some soft planting can create a retreat that feels intentional, regardless of whether or not you actually use it. Low walls, trellises or hedging can help define your backyard without closing it in. By framing the space, you can create structure, making a small garden feel purposeful.

The day of the month that you close on the purchase of your home is important and should be part of your contract negotiations. Whether you want to close early or late in the month depends whether you want to save money or ensure the process goes smoothly.

Mortgage interest is paid in arrears. The amount of prorated interest that you will pay at closing will be determined by the day of the month you close. A later date in the month means less interest paid as part of your closing costs. For example, if you were to close on May 30, then you would only pay two days of interest plus the interest due for June. Your first payment wouldn’t be due until July 1.

Because of these savings, 95% of closings occur at the end of the month. What this also means is that title and escrow companies are not as busy near the beginning of the month, and the closing process tends to go a bit more smoothly.

Selling your home isn’t just about highlighting its best features. It’s also about removing the things that turn buyers off. Even small details can make a big difference in whether your property feels move-in ready or neglected.

The biggest thing to avoid is out of date, worn, or unmaintained home features. Maintaining your yard is a big boost to curb appeal, and ignoring it is a big downgrade. Worn out carpets signal a lack of maintenance, so your floors should be recarpeted or replaced with wood or tile. Buyers may even notice out of fashion styles for doorknobs, faucets, or cabinets.

You should also avoid making your home look too personalized. You want your buyer to be able to imagine themselves living in the space, not glimpse how you are living there. Keep personal effects out of view and remove clutter. Some staging is useful, but it should be neutral, not overly personal or polarizing. The same goes for paint colors — many buyers will repaint anyway, but you want them to be able to focus on the home itself, not your design choices.

We’re not going to spend a lot of effort talking about month to month real estate activity in this issue. February invariably has more closed sales than January, because the escrows that close in January are for deals that were negotiated in December, when most people were partying instead of buying a home.

The one monthly anomaly screaming for clarity is the 72% increase in monthly sales in the Beach area, while the total increase in sales for the South Bay is only 20%. That’s a real outlier, and we didn’t have an explanation last year when the numbers were nearly the same. In February of 2025 the Beach came in with a 70% increase in the number of sales closed while the total South Bay monthly increase was 24%. The other three areas are normal and the raw totals are normal, except for sales skyrocketing at the Beach for one month. Perhaps there’s a new tax “loophole” happening?

Overall, home sales are still off about 20% from pre-pandemic years. Activity has been gradually catching up, but the projection is for several years of improvement before sales volume is back to what used to be normal. The big surprise in sales volume comes in comparing last month to February of 2025, Last year had shown a solid growth of 19% over February of 2024, with positive numbers in all four areas. This year shows plummetting sales in all four areas, with a drop of 19% across the South Bay.

With that thought in mind, and looking at the year to date, for just January and February, 2024 showed 2% sales growth, and 2025 4% growth. In what appears a total reversal, 2026 is dropping by 18%. It’s still early in the year, so the direction may change. At this point it looks as though economic and war worries may be slowing the number of transactions closing. There was evidence of increased buyer risistance over the last half of 2025. The first quarter figures next month will give a more thorough picture of what to anticipate for the year.

Median Price:

Shifting gear and looking at the median price, shows a similar theme. Once again, the Beach area is showing a super-charged increase in comparison to the balance of the South Bay. The Harbor area was up 1%, the Inland area up 5%, PV down 5%, and the Beach was up 31%!

On one hand, it could be said “Money is migrating to the Beach at an increasing rate.” Or perhaps, “Owners are dumping the Beach for huge profits.” It’s conceivable both are correct. In any event it’s an interesting phenomenon.

Year over year, where the chance to look ahead comes alive, things look much more restrained. The Beach is up 1% in median price, which is significant change from being down 29% in January. At the same time, the Harbor is up 5% and the Inland area is up 2% — all very tame.

Median prices on the Hill dropped by 16%. One needs to remember there is a comparatively small number of homes selling in the PV area on a monthly basis, so one or two unique transactions show up as huge blips in the charts.

Year to date, median prices are more constrained than last year. The Harbor area, the largest of the markets in the South Bay, is up 5% over the same period for 2025. The Inland area is flat, while the Hill is down 10% and the Beach is up 15%.

Continuing on the vein we started at the beginning, the sales being reported now were negotiated in January, before the crisis in West Asia bloomed. This shows a tempered market with pullback in both the number of homes sold and in the median price of those homes. The day to day feel of the South Bay real estate market seems to be continuing on a roughly similar pace, but it will be another month before we can really see the statistical impact. Let’s look again next month.

Beach:

M-m, vol: 91, 72%, med: 2,200,000, 31%

y-y, vol: -17%, med: 1%

ytd, vol: -17%, -13% from 2019, med: -15%, up 63% from 2019

Harbor:

M-m, vol: 220, 21%, med: 800,000, 1%

y-y, vol: -19%, med: 5%

ytd, vol: -22%, -27% from 2019, med: 5%, up 49% from 2019

Hill:

M-m, vol: 36, -27%, med: 1,722,500, -5%

y-y, vol: -22%, med: -16%

ytd, vol: 9%, 10% from 2019, med: -10%, up 36% from 2019

Inland:

M-m, vol: 84, 14%, med: 920,000, 5%

y-y, vol: -18%, med: 2%

ytd, vol: -17, -21% from 2019, med: -0%, up 40% from 2019

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

An Earthship home is a home built around sustainability. These types of homes are built to work with nature rather than against it. The concept dates back to the 1970s, born during the early environmental movement. They’re often made using recycled and natural materials, be it old tires, glass bottles or reclaimed wood, combined in clever ways to create a strong insulating house.

Anyone can pile up tires and wood in a vague house shape, but what sets Earthships apart is how they function day to day. They’re designed to collect their own energy using solar or wind power, harvest rainwater and naturally regulate indoor temperatures through smart design rather than relying on heating or air conditioning. Many even include indoor growing spaces, allowing homeowners to grow herbs, fruit or vegetables year-round.

Sustainability sounds great, but Earthship homes aren’t for everyone. You can’t build an Earthship home just anywhere — they work best in moderate climates. Tropical or arctic conditions can just be too much of a strain on the house. Also, they can take a lot of work to keep them functioning, so you’d need to be able to expend the time and energy to keep them running.

Buying your first home can feel overwhelming without the right preparation. It doesn’t need to be, though. If you do your research and manage your expectations, you’ll be able to make better choices. All you need is a good plan.

Start by figuring out what you need and what you can afford. Consider what you really need not just in a home, but in a neighborhood, and plan ahead for the future. For example, good schools might be more important if you’re planning to have kids soon, even if you don’t have any right now. Look at your income, savings and ongoing expenses to determine a comfortable budget. This includes not just the purchase but also life after moving in. Homeownership comes with regular costs such as utilities, maintenance and repairs, so it’s wise to leave room for the unexpected.

A professional support network can help you every step of the way. They’re not just here to sign the legal documents and be done with it. Your real estate agent can guide you through viewings, offers and negotiations, while professionals such as inspectors and appraisers can help uncover potential issues before you commit. Ask about local housing markets, typical prices and how competitive things are. You can also visit neighborhoods yourself to reveal details you won’t see in listings alone.

It’s also important to stay grounded. Yes, you should be excited about the home you’re about to buy, but you need to temper your expectations as well. Your first home doesn’t need to be perfect; it needs to work for your life right now while setting you up well for the future.

Many sellers skip staging their home, either because they think it’s not worth the time or money, or because they want their home to feel lived in. This might be sound logic if the staging is bad, but if you get your staging done well, it’s definitely worth it.

A competitively priced home that has also been staged to appear move-in ready will help justify its listing price. A positive first impression will motivate agents, who will put your home at the top of their list when showing properties to their clients. Successful staging will give your home an edge over the competition without having to compromise on price. It can sometimes feel like it’s just an added cost, but it’s actually an advertising investment.

It’s true that when you stage your home, it’s marketed in a more neutral way. This can feel like it’s lost its personality. But a properly staged home should actually help buyers more easily visualize themselves living in your home. It does this by helping define spaces and room sizes and giving every room a purpose. Remember that the buyer isn’t you — they want to imagine themselves living there, not you living there.

Captain John and the band breathe new life into vintage sea shanties and nautical tunes with Celtic-punk and pirate-rocker swagger.

Kraus leads this merry crew of powerhouse musicians after years spent as a sea captain and growing up in a musical household. His pioneering band perfectly combines his love for music, the sea and the legacy of the seafaring storytelling.

And, just so we’re all clear, in addition to being a multi-instrumentalist and lead guitar player, John Kraus really is a captain – for many years at the helm of one of the LA Maritime Institute’s stunning Tall Ships!

The Goers are: Tim Weed on violin, David Dutton on the drums and jazz legend Bob Aul on fiddle and tuba. Paul Givant of Rose’s Pawn Shop shows up frequently to play guitar and banjo.

Jose Antonio Rodriguez is an award-winning Spanish guitar virtuoso at the forefront of his generation. Known for his powerful contemporary style that spans film scores, dance, and orchestral works, he’s performed around the world with legends like Chick Corea, Al Di Meola and George Benson, and has countless recording credits on international award-winning albums including the pop hit “Macarena.”

🍷 Pre-Concert Wine Tastings Led by JP Molinari: Free to Grand Vision members at the Friend, Champion, VIP Circle, Arts Advocate, and Performing Arts Patron level – up to two per household, $16 per person for all others. Concert tickets are required to participate. Members’ tasting tickets must be redeemed in advance. Tastings begin one hour before the show, please arrive no later than 30 minutes into the tasting to participate.

A night of irresistibly fun live music and dancing featuring DJ Serg and SoCal’s soul-ska cumbia dance band, Maria Blues. All ages event.

South LA-based musician Maria Blues brings a dynamic fusion of ska, reggae and Latin with a hint of soul. Her wide range of musical influences speak for themselves. From Amy Winehouse and Etta James to Selena and Lauryn Hill, Maria creates a unique sound that will capture your heart and get your feet moving!

DJ set starts at 8:30 PM. The band will go on at 9:30 PM.

Seating:

General admission is standing room only. While a limited number of chairs will be available in the general admission section, you are not guaranteed a seat.

Tables will be marked with the name of your party and have 4 seats.

Full Circle

Sun, Mar 22, 2026 4:00 PM Doors 3:00 PM

This show is SOLD OUT! If you would like to be put on the waitlist, please call the Annex at 310-833-4813, placement on the waitlist does not guarantee a ticket.

Country rock trio known for their soaring vocal harmonies and unique renditions of covers and original songs. Going back as far as high school, Patti Orbeck, Debra Bain and Sylvia Owens have had decades to perfect their chemistry. Combine the harmonies of Crosby, Stills, Nash & Young with the music of the Judds, and you get Full Circle.

Whether they’re playing a song of their own or a recognizable classic, they create unique arrangements with impressive vocals and sincere dynamics that will feel like a warm hug. Having performed at Andy & Renee’s annual Dylanfest and Fleet Week here at the harbor, they’ve become a local favorite around the Annex. Hear a mix of songs, including “Angel from Montgomery,” “Chain of Fools” and “Jolene.”

Fortunate Son CCR & John Fogerty Tribute

Fri, Mar 27, 2026 8:00 PM Doors 7:00 PM

This show is SOLD OUT! If you would like to be put on the waitlist, please call the Annex at 310-833-4813, placement on the waitlist does not guarantee a ticket.

Fortunate Son celebrates Creedence Clearwater Revival and John Fogerty’s legacy as the longest-running tribute to the iconic band. Since 1994, frontman Brad Ford has honored John Fogerty with all-around authenticity. Hear the swampy blues of “Born on the Bayou,” the country sounds of “Bad Moon Rising” and rock anthems like “Proud Mary” and “Have You Ever Seen the Rain.” Mike Franceschini joins on guitar, with Ron “The Deacon” Ota on bass and vocals and Daniel Murdy on drums.

Stomping, shuffling & hollering like a modern-day Howlin’ Wolf, Chris Pierce as the Reverend Tall Tree stands at the crossroads of Blues, Soul, and American Roots music. From there, he channels the raw spirit and emotional gravity of the genre’s golden era into a modern, electrifying live experience.

Whether delivering sermons in a smoke-filled club, a tent revival atmosphere, a classic theater, or from the main stage of a festival, Reverend Tall Tree reaches straight for the core—where rhythm meets testimony and the music still tells the truth. His performances recall the power, urgency, and communion of mid-century Blues and Soul masters, where every note carries weight and every song feels lived in.

Chris Pierce has spent years honing his craft on stages around the world, headlining his own tours while also sharing the road with an extraordinary range of artists, including Neil Young, B.B. King and Allison Russell, among others. His music and unmistakable voice have also found their way into numerous films and television shows, further cementing his reputation as a singular American storyteller.

Palos Verdes’ own community theater company, the Pennyroyal Players, are hitting the stage with a musical tribute to 28 “Radical Women”—the trailblazers who weren’t afraid to fight for their rights, their freedom and their vote!

This incredible journey kicks off in England in 1591 and races right up to Tennessee in 1920 when the 19th Amendment finally paved the way for women to a cast a ballot.

Get ready for a fast-paced musical romp through the battles fought for equality. Hear about the struggles, the heartbreaks, and the triumphant victories these heroic women earned every single day. The show tells their story with a healthy dose of humor, featuring historically accurate songs set to familiar tunes—guaranteed to entertain everyone!

The Grand Annex Art Saloon

Thu, Apr 02, 2026 5:00 PM – 8:30 PM Doors 5:00 PM

Enjoy a laid-back evening of music and art at this new First Thursday event, featuring art by fINdings Art Center.

fINdings Art Center, in collaboration with Grand Vision’s Annex Arts Saloon, presents artworks curated by Henry Krusoe.

Henry Krusoe is an Otis College graduate and has been an Angels Gate Cultural Center resident artist since 2019, creating multimedia artwork spanning analog and digital formats.

Hear the thunderous rhythms of the drums that affirm our beautiful, resilient existence. Come feel the energy and celebrate the power of being truly seen. Mujō Dream Flight’s first full-length concert, VISIBLE, celebrates Trans Day of Visibility and explores how we resist social erasure when our race, gender, class and disability are all under attack.

Mujō Dream Flight (MDF) is the artistic vehicle of founding taiko artists Sasen Cain, Yeeman “ManMan” Mui, and Maxyn Rose Leitner. Based in Los Angeles, they collaborate locally and globally with other predominantly trans/non-binary taiko artists, creating both original works and traditional adaptations. MDF’s art centers dance and personal storytelling informed by their specific cultural backgrounds.

In 2023, MDF organized Blurring the Color Line with Taiko, a well-attended and deeply engaging afternoon arts experience connecting important questions about race, immigration, culture, and American-ness. The event allowed us all to hear from filmmakers, performing artists, community leaders, educators, and ethnomusicologists, as they share their experiences and ideas.

The same year, MDF embarked on its first national tour, called “Haimweh” (Bavarian for homesickness), with the dual aims of highlighting trans/non-binary peoples’ often-fraught connections with their hometowns & families, and a journey of retrieving the belongings of one of our members whose parents don’t accept faer transness, and reclaiming identity, belonging & inter-dependence. This tour was funded, in part, by a Taiko Community Alliance Tier 1 grant.

MDF gave voice to Queer Asian community in LA with our performance at:

The inaugural Okaeri’s Queer Obon (2023).

Transforming Community Care: AANHPI LGBTQIA2-S Mental Health and Wellness by LA Department of Mental Health

Cross cultural solidarity movement, the importance of being with community – FandangObon (2024)

Fusion, genre – the North American Taiko Conference in Phoenix, AZ (2025).

Guest artist Aki Oshiro (they/them) is a queer, trans, and non-binary, fourth-generation Japanese Okinawan-American professional taiko artist based in Sacramento and the San Francisco Bay Area. Aki began their taiko journey at age 9 with Kona Daifukuji Taiko in Kona, Hawai’i. From 2001 to 2007, they served as an instructor and touring ensemble member with Portland Taiko while earning a Bachelor’s degree in Music Performance (Percussion) from Portland State University.

From 2007 to 2014, Aki was an instructor and youth programs director at Sacramento Taiko Dan. Currently, they are the founder and Artistic Director of Tsubaki Ensemble, SOKO Taiko, and Queer Taiko, as well as the Creative Director of Placer Ume Taiko. Aki also teaches at San Mateo Buddhist Temple Taiko and is a touring member of Taikoza and Unit Souzou.

Aki has performed and conducted taiko workshops across the U.S. and internationally, including in Canada, Japan, Switzerland, Italy, Russia, Australia, New Zealand, and Colombia.

Team Taiko is Grand Vision’s community drumming program taught by ManMan Mui.

This concert is sponsored in part by TaikoVentures and Creative West Tour West Grant.

Come early to the show! You will be met at the door by Shag actors and welcomed into their tiki cocktail party.

Let’s Shag!

The one and only SHAG himself will be at every show of this murder mystery musical set at a Tupperware party! “Shag with a Twist” serves up an evocative cocktail of vibrant music and performers that brings to life the art of Shag when pupu platters and bouffants were all the rage. Guests are encouraged to come dressed in their finest tiki, pin-up girl style or 60s Mod attire and join the party.

This event is produced by Shag with a Twist Productions.

TUESDAYS 5:30PM — 7:30PM The Lighthouse Cafe, 30 Pier Avenue Hermosa Beach, CA 90254 310 376-9833

Andy & Renee – Banana Leaf

THURSDAYS 6:30PM — 9:00PM Banana Leaf & Beach Cities Social, 1408 S Pacific Coast Hwy, Redondo Beach, CA

Andy & Renee & Friends – Neil Young Tribute Show – SOLD OUT!

SAT, MAR 14 @ 6:00PM Studio32, 17411 Delia Ave., Torrance, CA 90504

Neil Young Tribute show with Andy & Renee, Steve Whalen, John Hoke, Marty Rifkin, Jamie Daniels, Brax Cutchin, & Joe Caccavo. Doors at 6p, Show at 7pm. SOLD OUT! BYOB

Andy & Renee – Terranea Lobby Bar

FRI, MAR 20, APR 13 & 17 7:00PM — 11:00PM Terranea Lobby Bar, 100 Terranea Way, Rancho Palos Verdes, CA 90275

Andy & Renee – Brews Hall

FRI, APR 3 7:00PM — 10:00PM Brews Hall Del Amo, 21770 Del Amo Circle East, Torrance, CA 90503

Andy & Renee & Hard Rain – Las Candelistas Fundraiser

SAT, APR 18 5:00PM — 9:30PM Empty Saddle Club, 39 Empty Saddle Road, Rolling Hills Estates, CA 90274

Get tickets and info at https://lascandalistas.org/event/spring2026/

Andy & Renee – King Harbor Yacht Club

Members and guests only.

FRI, MAY 8 6:00PM — 9:00PM King Harbor Yacht Club, 280 Yacht Club Way, Redondo Beach, CA 90277

Andy & Renee & Hard Rain & Friends- 36th Annual Dylanfest

SUN, MAY 24, 2026 12:00PM — 8:00PM Torino Plaza, Torrance Cultural Arts Center, 3330 Civic Center Drive, Torrance, CA 90503

Hosted by Andy & Renee & Hard Rain, Dylanfest is the South Bay’s longest-running music festival—a heartfelt celebration of the songs and spirit of Bob Dylan, one of America’s greatest and most influential songwriters. Tickets available NOW!

Andy & Renee & Hard Rain – The Music of Bruce Springsteen

SAT, JUN 27 @ 8:00PM The Grand Annex, 434 W. 6th St., San Pedro, CA 90731

ALMOST SOLD OUT! Get tickets and info at https://grandvision.org/event/andy-renee-hard-rain-the-music-of-bruce-springsteen/

Andy & Renee & Hard Rain – Malaga Cove Library Park Concerts

WED, JUL 8 6:30PM — 7:45PM Malaga Cove Library Park, 2400 Via Campesina, Palos Verdes Estates, CA

Andy & Renee & Hard Rain – Torrance Hot Summer Nights Concert In The Park

SAT, JUL 25 @ 5:00PM Wilson Park, 2200 Crenshaw Blvd., Torrance, CA 90501

This is a once a month (every third Tuesday) show that is designed as a listening room for world class songwriters, many with hit songs, long touring/recording associations with music legends ETC… to play their original music in an intimate setting. NO COVER BUT DONATIONS ARE STRONGLY ENCOURAGED AND GO TO THE SONGWRITERS. Project Barley serves excellent Food (Gourmet Pizza, wings, sandwiches, salads), wine, and award winning beer. Food served till 8:30pm. No reservations so arrive early to get a table. This month we are proud to present: THE JOLENES, JUNE CLIVAS, JODI SIEGEL

THE JOLENES

Smile! It’s the Jolenes!

The Jolenes is a mega volt supercluster quartet of roots rock rascals who hail from Los Angeles, California by way of Auburn; Outer Space; stone cold Kansas City; the Miracle Mile; the Earth’s nickel plated nuclear rated chewy nougat core; the West of Adams; the East of Eden; the LBC, an as of yet to be discovered fifth dimension commonly referred to by leading scientists and religious philosophers as Jomagnalene…and all parts in between.

Constructed of popsicle sticks, painter’s tape, chicken wire and Dan Janisch (Dan Janisch and The Sallys), Grant Langston (Grant Langstons and The Grill Masters), David Serby (David Serby and The Hillbilly Fringe), and Dale Daniel (The Hacienda Brothers, Rick Shea and The Losin’ End, etc, etc., etc.), they are a fully insured and bonded, AAA graded, golden throated, songwriting, crime solving, guitar bashing and drum busting investment collective who will happily help you cheat on your taxes. Together and separately they have played on, penned, recorded, and registered thousands of carols, poems, rockers, mockers, oldies, hymns, canticles, chants, rants, lullabies, ballads, three sea shanties, and five-eights of an Italian opera based on the classic Burt Reynold western from 1973, The Man Who Loved Cat Dancing.

The Jolenes are deadly serious song and dance men, handsome in their own way, shameless, blameless, and they are dying to give you a good time. You can find them struggling not to drown in all of your favorite social media streams. In their spare time they like to crochet cowboy booties for abandoned beagles, lead book groups for retired snake charmers, and study the text of ancient Chinese fortune cookies.

Don’t forget to smile! It’s the Jolenes!

JUNE CLIVAS

June Clivas is a cow-punk firecracker of a singer, performer and songwriter! Many know her from her years playing with her band; June Clivas and the Ditty Boys. Formed in 2018, June Clivas and The Ditty Boys is a group of five talented musicians who came together with a shared passion for creating original music that resonates with people. Drawing inspiration from a wide range of genres including country, rock, and western, we have created a unique sound that blends catchy melodies with heartfelt lyrics.

From intimate acoustic sets to high-energy shows, we strive to connect with our audience and create an unforgettable experience.

Whether you’re a longtime fan or hearing June Clivas and The Ditty Boys for the first time, we invite you to “Ditty Up” and join us on this wild ride. As stated by the infamous Slim Jim Phantom of The Stray Cats, “They’re onto something.”

JODI SIEGEL

Jodi Siegel, originally from Chicago, IL, is a singer, songwriter and guitarist. Over the years Jodi has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and countless others. Her songs have been recorded by Maria Muldaur, Marcia Ball, Tommy Ridgley and Teresa James.

She has recorded two CD’S; Stepping Stone and her latest CD, “Wild Hearts,” produced by Steve Postell (Immediate Family, David Crosby, Eric Johnson, Robben Ford, Iain Matthews), is filled with great songs, cool grooves, intimate, smart lyrics and some of the best of the best musicians in Los Angeles today including; Mike Finnigan (organ, piano), Hutch Hutchinson, Abe Laborial Sr., Alphonso Johnson (bass), Russ Kunkel, Michael Jerome Moore, John Ferraro, Arno Lucas (drums, percussion), Joe Sublett (Saxophone) and Maxayne Lewis and Clydene Jackson (background vocals). Each song has a soulful delivery with an undeniable down-home elegance. It has received great reviews by Patrick Simmons (Doobie Brothers), Maria Muldaur, Walter Trout, David Mansfield (T Bone Burnett), Leland Sklar, Mike Finnigan and Doug Macleod to name a few.

Jodi is in the pre-production stage of recording a new record with Grammy winning producer/drummer (Taj Mahal) Tony Braunagel.

Before we start, let’s be clear about the time frame of the business we’re discussing. I say that because it’s easy to forget the sales closures we are discussing for January are for deals cut in December, or possibly late November. The average escrow time is still 30-45 days. That helps to explain the timing of some shifts in the raw numbers. Because fewer deals are cut in the time frame from Thansgiving to the New Year, traditionally the holiday season, it takes only a few more deals, or a few less dollars, to shift the percentages dramatically in January. Given those qualifications, let’s look at the statistics for January in the South Bay.

It’s not unusual for January real estate sales to be fewer than December, though the numbers have been stabilizing since the end of the pandemic. January of 2025 was only down 17% across the South Bay from January 2024. The year before, January of 2024, sales were off 24% from 2023, and the year before was down 28% from the 2022 sales. The surprise is in 2026 starting the year with an out-size 35% decline from December of 2025. (See the area break down below for details.)

The jump from a years long trail of improving numbers to a 35% drop in month to month sales volume, especially when spread relatively equally across the four areas, draws attention. R emember the Hill is the smallest of the areas and just because of the nature of mathematics it has wide percentile swings.

As you see, our month to month sales volume has dropped significantly across the South Bay, and has made a significant drop from the historical upward trend, as noted above.

Monthly median prices have also dropped in the Beach and PV Hill areas, both typically more volatile in response to economic markets. The Harbor and Inland areas, on the other hand have shown modest growth in median value from December into January. Could it be we are seeing a shift in valuation, from the flashy high end properties to bread and butter properties?

Year over year prices seem to be down across the South Bay with the exception of the Harbor area, a surprise for the largest market area of the South Bay. A 5% increase in the median price the for largest volume area in the south Bay is a huge stop sign on the path to market.

Sales are down everywhere except the Hill which represents a mere 14% of the month’s sales. It’s easy to say three out of four markers indicate slower business for the coming year.

In the past the format of the newsletter would go on to discuss details of each of the market areas. We’re going to change that a bit starting this month. Rather than a textual description, we’re including just the statistics for each area. If you, as the reader, have additional questions, just give us a call and we’ll walk through the numbers with you.

In addition, we’ll be including charts, showing the shifting business as the months go by. Please let us know if you like the transition to less words and more pictures.

Beach:

M-m, vol: 53, -41%, med: 1,675,000, -8%

y-y, vol: -17%, med: -29%

ytd, vol: -17%,, med: -29%, ytd vs 2019: vol -97%; med 23%

Harbor:

M-m, vol: 182, -39%, med: 795,000, 2%

y-y, vol: -25%, med: 5% Is the Harbor shifting? Or just a shortage of inventory?

ytd, vol: -25%,, med: 5%, ytd vs 2019: vol -96%; med 31%

Hill:

M-m, vol: 49, 9%, med: 1,820,000, -9%

y-y, vol: 53%, med: -4%

ytd, vol: 53%,, med: -4%, ytd vs 2019: vol -94%; med 25%

Inland:

M-m, vol: 74, -36%, med: 875,000, 4%

y-y, vol: -15%, med: -3%

ytd, vol: -15%,, med: -3%, ytd vs 2019: vol -96%; med 18%

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates Inland=Torrance, Lomita, Gardena

Spring is a busy time for real estate, and is a busy time for many other people as well. For years, we’ve been taught to manage our time better to improve our mental health and well-being. But time is fixed, making it difficult to manage completely. You should instead focus on managing your energy, since how you feel physically, mentally and emotionally determines how well you use the hours you have.

The most important thing to pay attention to is yourself. Notice the patterns in your energy throughout the day and across various different types of tasks. Not everyone has the same amount of energy at all points during the day, and might respond differently to different tasks. Energy isn’t just about avoiding exhaustion; some tasks totally drain you, while others can take the same amount of exertion but make you feel energized. This is the same principle that separates introverts from extroverts — not necessarily enjoyment, as people tend to believe — and can be extrapolated to many categories of activity.

Once you know more about yourself, you can choose activities that match your patterns of energy levels. Find one or two habits that genuinely restore you. Don’t try to force yourself to do more when the task that you’re doing is draining you right now. Instead, take a break from it and do something that’s likely to be energizing for you in this moment. That way, you’ll be able to focus better on the initial task later and likely complete it in a much shorter time. Breaks are intentional investments in your energy levels, not laziness or rewards for hard work, and shouldn’t be caused by burnout.

As we enter spring cleaning season, consider cleaning up not just the inside of your home, but the outdoor space as well. It’s easy to forget that a few smart landscaping updates can go beyond just transforming your outdoor space; it can also add value to your home. Here are some ideas to improve both the look and the value of your home.

Native plants, especially trees, are an excellent addition. Plants that naturally thrive in your local climate will need less nurturing, attract pollinating wildlife and blend seamlessly into the natural landscape, creating a low-maintenance, visually appealing space. Trees in particular have a significant impact on home value for many reasons. It helps to create a sense of privacy, allows for shaded areas in the hot summer months, and can make the outdoor space feel generally more interesting and intriguing to potential buyers.

Think about all the various ways you use your outdoor space, and considerbreaking up large spaces in your garden into defined spaces. A gravel dining area, a paved fire pit corner, or a shady hammock nook are clear examples of usability that help buyers imagine themselves in the space. Installing edging between the lawn and flower beds helps keep the garden looking neat and well cared for.

Consider upgrades that are both functional and visually appealing. If the concrete is starting to crack, replace it with stepping stones, gravel, or reclaimed brick. Artistic arrangement of these features can also serve as a guide for buyers.Outdoor lighting helps to make the space feel usable beyond daylight hours as well as creating a sense of safety and security.

The secret to making sure you are buying the house that is best for you is knowing what your basic needs are before you proceed, and what are simply things that would be nice to have. In order to do this, remember that many wants can be achieved later if basic needs are met. Once you decide what you can live with and without, you can budget accordingly.

Basic needs include health and safety items, which should be your first priority. A solid foundation and floors and walls without defects are important features for safety and are difficult or costly to fix later. The condition of your HVAC is also a health concern, though that can be repaired. Good location is also a priority, despite not necessarily being a safety concern, since that can’t be changed later. Anything else on your list would be want-to-haves rather than need-to-haves. For example, you can later change paint, countertops, and fixtures or do remodeling.

A night of irresistibly fun live music and dancing featuring DJ Nativity and the blazing 4-piece punk-cumbia band, Cara Borracho. Ages 21 and up event.

DJ Nativity’s set starts at 8:30 PM. The band will go on at 9:30 PM.

Seating: General admission is standing room only. While a limited number of chairs will be available in the general admission section, you are not guaranteed a seat. Tables will be marked with the name of your party and have 4 seats.

Strings Chamber Ensemble Series “Valentine’s Concert”

Celebrate the season of romance with a selection of timeless pieces that capture the beauty and emotion of love in all forms. Classical selections include “Andante Cantabile” by Tchaikovsky, “String Quartet No. 2” by Alexander Borodin and “Rosamunde Second Movement” by Franz Schubert. The “pop strings” section will include “Love & Marriage,” “A Whole New World” and “Sweet Child O’ Mine.” Arrangements by Shura Sasaki.

Shawn Jones is a prolific Southern California-based singer, songwriter, and virtuoso guitarist whose three-decade career serves as a soulful bridge between blues, rock, and Americana. Discovered by country legend Waylon Jennings while playing a small Los Angeles club, Jones was eventually recruited to play lead guitar for Jennings’ band on the 1996 Lollapalooza tour and appeared on his album Right for the Time.

Over the years, he has established himself as a respected independent force, sharing stages with icons like B.B. King, Buddy Guy, and Bonnie Raitt, while also spending ten years as the lead guitarist for Deana Carter. With a tireless touring schedule that sees him performing over 200 dates annually across the USA and Europe, Jones continues to release acclaimed work, including his recent album In My Blood (2024).

Shawn Jones: guitar, vocals Herman Matthews: drums Sam Bolle: bass, backing Vocals Marc Hugenberger: keys

The Grand Annex Art Saloon

Thu, Mar 05, 2026 5:00 PM – 8:30 PM Doors 5:00 PM Live Music Starts at 6:30 PM

Enjoy a laid-back evening of music and art at this new First Thursday event, with your hosts, local musicians Chris and Emily Huff. Featuring live music by musicians from the San Pedro Musicians Directory and art by fINdings Art Center.

Local musician Dustin Case brings the best of two musical worlds, known for both his heartfelt acoustic storytelling and raw punk energy. His acoustic sets carry a lyrical and vulnerable essence, while his fierce stage presence and aggressive vocal style embody the spirit of Los Angeles punk.

fINdings Art Center, in collaboration with Grand Vision’s Annex Arts Saloon, presents artworks curated by Henry Krusoe.

Henry Krusoe is an Otis College graduate and has been an Angels Gate Cultural Center resident artist since 2019, creating multimedia artwork spanning analog and digital formats.

L.A.vation astonishes with hit after hit from each of U2’s blockbuster albums. Dance along to songs like “New Year’s Day,” “With Or Without You,” “Beautiful Day,” “One” and “Vertigo.” Frontman Patrick Boudreaux perfectly captures the spirit and essence of Bono, taking this spot-on U2 experience around the world. If you “Still Haven’t Found What You’re Looking For,” you won’t want to miss this legendary tribute!

A “Warner Grand on the Road” Concert

While the Warner Grand Theatre undergoes renovation, Grand Vision Foundation presents Warner Grand on the Road! This intermittent concert series brings the magic of live music to venues across San Pedro. Proceeds from this event support Grand Vision’s Meet the Music youth education program, and continued live music programming at the Grand Annex Music Hall.

VIP Reception 6:00 PM / Meet & Greet 6:30 PM

VIP Ticket holders are invited to attend the pre-concert reception and Meet & Greet with the band.

VIP Tickets include light appetizers, desserts, one complimentary drink and access to a private no-host bar before the concert.

Captain John and the band breathe new life into vintage sea shanties and nautical tunes with Celtic-punk and pirate-rocker swagger.

Kraus leads this merry crew of powerhouse musicians after years spent as a sea captain and growing up in a musical household. His pioneering band perfectly combines his love for music, the sea and the legacy of the seafaring storytelling. And, just so we’re all clear, in addition to being a multi-instrumentalist and lead guitar player, John Kraus really is a captain – for many years at the helm of one of the LA Maritime Institute’s stunning Tall Ships!

The Goers are: Tim Weed on violin, David Dutton on the drums and jazz legend Bob Aul on fiddle and tuba. Paul Givant of Rose’s Pawn Shop shows up frequently to play guitar and banjo.

")

")

")

")