This winter is probably going to be hotter than usual — and I’m not talking about climate change. According to a survey conducted in September and October of this year, 65% of sellers who planned to list between then and the end of 2022 are targeting either this year or the first quarter of next year. The holiday season tends to be slower, but sellers aren’t predicting that it will be.

Compared to the spring, many more sellers are expecting things to go their way. 38% are banking on heavy competition, which will also lead to higher-priced offers either at or above asking price, more all-cash offers, and more concessions by the buyer. They also think they’ll be getting offers quickly; 42% expect an offer within the first week. Only 1% of respondents don’t expect any of these things to happen.

Winter is always a slow season for real estate. Most people are too busy with the holidays to think about buying or selling. But it does happen. Buyers willing to look during winter are already a captive audience, since they clearly have a reason to buy, but you can still do your part as the seller to seal the deal. In addition to improving your curb appeal, which is an excellent motivator at any time of the year, you can use the season to your advantage in winter.

Make your home inviting. Add more lighting, especially outdoors. It gets dark earlier in winter, and prospective buyers want to be able to actually see your home. If you have a fireplace, turn it on, or turn up your heater. Winter is colder even in places that don’t get snow, especially after work hours. Staging your home for the holidays can also help. Even if you don’t celebrate or aren’t feeling particularly festive, a plate of cookies or season-appropriate decorations will let people know someone does call this place home.

One indicator that the real estate market is showing signs of recovery is the levels of mortgage fraud. Unfortunately, that’s not a good thing, because mortgage fraud dropped dramatically during the Great Recession. Fewer mortgages does mean fewer opportunities for fraud, but the numbers are expressed as percentages, so it’s not a directly proportional relationship. Fraud indications increased by 37% between Q2 2020 and Q2 2021. Even with such a large jump, it’s actually not much higher than the average across the past decade.

Mortgage fraud can originate from either the lender or the borrower. Borrower fraud is relatively simple to look out for, but it’s something the lender would need to do. Lenders can look at recent job changes, especially to a higher-paying job, claims that the property is a primary residence, inconsistences in data about the property, failure to disclose debt or past foreclosures, or possible attempts to disguise parts of the transaction. These indicators aren’t a surefire guarantee of fraud, but they’re important areas to begin the search. A borrower who has had a Suspicious Activity Report (SAR) filed against them may be blocked from future mortgage loans or be required to pay off their mortgage immediately or go into foreclosure. Fraud by lenders could result in fines, loss of license, or possibly jail time.

October is the turning point where the heat and excitement of summer cools, the children are back to school–in person this year–and the real estate market starts to button up for the winter. Being SoCal as we are, we don’t button up as much as most of the nation, but things do slow considerably between Thanksgiving and New Year’s Day.

We’re seeing normalcy appear more and more often, now that the pandemic is winding down. During the first quarter of 2021 we watched month-over-month volume changes ranging from a 33% decline to a 69% increase. Seeing some of the monthly statistics moving back into the single digits is highly encouraging.

Throughout this year we have essentially ignored the comparison of 2021 to 2020. The “Lost Year” of 2020, compounded as it was with the pandemic and what was anticipated to be a minor recession, has been a nightmare in terms of short term business projections. Trying to understand where the real estate market is headed, we have resorted to comparing two or three month trends, which is more or less like playing the slots.

Now in the fall of the year, looking at slower winter months ahead, rationality seems to be returning in the statistics we’re seeing–not all– but, most.

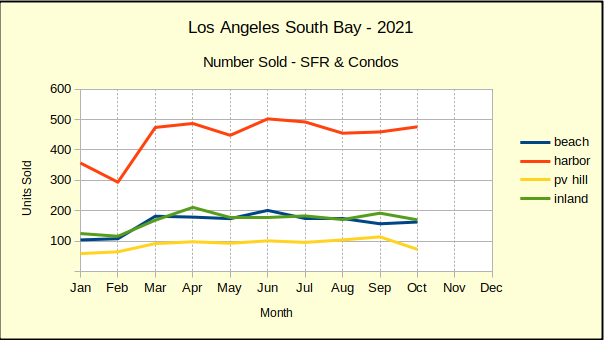

Sales Volume – Some Down, Some Up

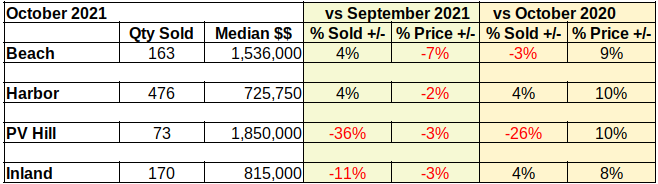

As we can see by the yellow line in the chart below, Palos Verdes sales volume took a big dive this month. The Harbor was up, the Beach was up, but the inland was down and sales on the PV Hill was way down.

We’re not able to see any outstanding reason for the 36% drop in the number of homes sold in PV for October versus September. Similarly, the Inland area loss of 11% in the number of units sold during October, is inexplicable. But then, much of what we’ve experienced in the time of Covid has been lacking in explanation. For good or bad, we’re adapting to dramatic shifts in the world.

By comparison to Palos Verdes, the Beach which has been losing sales volume since mid year, turned up for the month, increasing the number of homes sold by 4%.

The chart shows the Harbor area having the greatest variance in month-to-month sales numbers during the first half of the year. Since June the shifts have been more gentle.

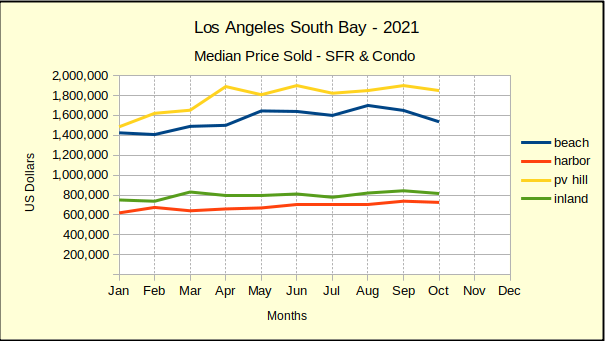

Median Price – Down Everywhere

October brought a decline in the median price of sold homes in all four segments of the market. The Beach Cities dropped another 7% this month, after having fallen 3% last month.

From a broad perspective, two things are happening. The mundane answer is the time of year. It’s fall and it’s often possible to get a better deal in fall or winter because there are fewer buyers competing in the market. The size of these percentages imply there are more than seasonal reasons.

A more exotic explanation involves the underlying motivation for the steep increases in price from May of 2020 to June of this year. Those prices were reactions to the low interest rates combined with a persistent shortage of available homes. Bidding wars drove prices up at rates that aren’t sustainable. Forecasts call for as much as a 15% overall increase in median prices at the end of the year. A typical year will be closer to 4% inflation, so as mortgage interest rates increase (they’re over 3% as I write this) we’ll have downward pressure on prices.

At the same time, Federal loan forebearance related to Covid ended September 30. Nationwide projections indicate approximately 17% of owners who were in forebearance are currently unable to make payments and don’t have a plan. Another 7% have a plan. They plan to sell. Nationally, we could see 20% of a million homes added to the inventory in coming months.

Locally, we’ve seen a handful of pre-foreclosure and foreclosure properties come on the market. Currently there are 4 Active, and 8 In Escrow, with 13 Sold in the past six months.

All of which is to say we forecast a correction in prices.

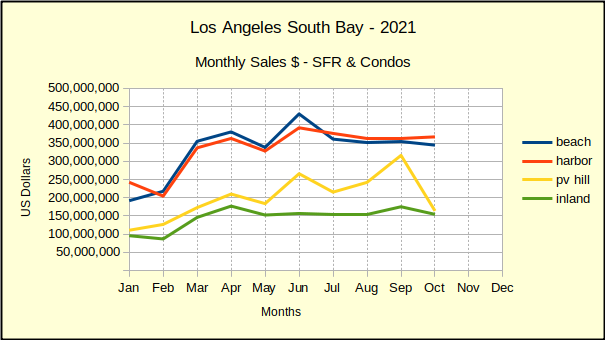

Total Sales Dollars – A Big Dive for PV

Look at the yellow line in the chart below! October saw a noticeable drop in Palos Verdes volume. Here, we see that convert to a sharp decline in cumulative sales dollars. A drop in median prices from September to October multiplied by a decline in the number of hones sold resulted in a $150M drop in total sales for the month. By comparison, the other areas showed mixed results, with moderate numbers.

This is a good time to remind readers that these four broad categories we use for this analysis are defined by the type of housing predominantly found in the area. As a matter of geological necessity, there are fewer homes at the Beach and on the Hill than there are Inland, or in a Harbor city. Probability dictates that we occasionally have statistical results that look dramatic, but are simply an anomaly resulting from the small number of homes we’re dealing with in any given month.

The Summary

We expect 2021 to leave us with a solid real estate market, albeit with some correction to inflated median prices, The October vs. September numbers clearly show some price resistance. Sales volume is mixed, showing some hesitance to buy on the Hill or Inland. The Beach Cities and Harbor areas both still show ready, willing and able buyers.

We wish everyone a Happy Thanksgiving and a wonderful Holiday Season!

While Millennials make up the largest contingent of potential homebuyers, they’re not without competition. Baby boomers have been buying at an accelerating rate as well, perhaps looking for retirement homes, or potentially buying for their children, who are probably Millennials. Average age of home buyers has been trending upward for years, but the Great Recession intensified the trend greatly.

This is because heavy competition favors the older generations. Millennials are generally first-time homebuyers without any equity, many are saddled with college debt from ever-increasing tuitions, and wage growth hasn’t even begun to keep up with inflation. What low supply existed was easily snatched up by those who could afford to pay above asking price, in all likelihood, those who had already owned a home for decades.

Most couples that don’t have children yet begin with a starter home, that’s a bit smaller but has everything the couple needs for now. That’s fine, but many of them don’t know how best to handle upsizing once they decide to have children. Many families don’t want to deal with the stress of a home purchase while experiencing the stress of a pregnancy. It’s an understandable thought process, but the stress of moving with a small child is actually much greater than the stress of moving while pregnant. It’s always best to move before the child is born.

You might think that puts a tight deadline on your home search. That’s where a real estate agent comes in. A professional agent only needs to know what you want done, and they’ll get it done. You don’t need to fuss over every detail throughout the process. Though, you can still help the agent, and yourself, out a bit by working on decluttering your home before it’s sold. This ensures a faster sale while also doing some of the packing work early.

If you’re interested in a custom-built new construction home, you’re going to need to talk to an architect, unless you are one, of course. That means you’re going to need to know what to ask them. Many people are only interested in whether or not the architect is available and has time for a new project. While that is certainly important, since the project won’t happen if the architect isn’t available, there’s a lot more that goes into picking an architect.

Interview multiple architects before picking the right one for your project. Take a look at their portfolio. Even highly versatile architects will have some recurrent themes or design quirks. You might even ask them directly what they consider their specific aesthetic to be. And if a particular architect is a specialist in the type of design you want, you’ll know they have plenty of experience with it. Ask about their fees in detail. Cost comparison is important, and not even just the bottom line. Not all architects provide the same list of services or calculate costs in the same way. A low cost may just mean that this architect isn’t providing services like obtaining waivers or communicating with the construction crew to make adjustments or verifications. Most of the time, fees are a percentage of the overall cost of the home, generally ranging from 5-20%. If you’re planning to build a luxury home, you may be able to save money by looking for an architect that charges a flat rate, who are less common.

The pandemic and work-from-home sparked a trend of moving out of dense urban areas into rural, cheaper areas. Leaving congested cities meant social distancing would be easier, and people were still able to work while paying less for housing. But it turns out that the trend didn’t really change anyone’s opinion of rural living — it’s starting to decline as pandemic fear is lessening and more people are moving back into the city, as well as back into offices.

Searches outside the prospective buyer’s current metro area are still above the pre-pandemic levels, at 30.1% compared to 25%. But they’ve dropped off consistently since the peak in Q1 of 2021, which was 31.5%. The pattern is likely to return to normal levels in 2022 or 2023. While more people are moving back to the big cities, they’re still paying attention to their wallets in where they look. Cheaper metro areas, such as Sacramento, are becoming far more popular destinations than expensive coastal metros like San Francisco.

Homeownership costs are not a simple matter of paying the purchase price. For one thing, most people don’t pay full cash. Even a 20% down payment is going to be the bulk of your first year’s costs, but it’s not all of it. Closing costs are an additional up-front cost, and you’re also going to pay the first installments of recurring costs, which include mortgage payments, homeowner’s insurance, and property taxes. Because of these costs, there’s a slight difference between ranking median home prices and ranking average total first-year costs, though they’re not too far off.

Among 20 of the largest US cities, Indianapolis has the lowest first-year costs, while San Francisco has the highest. These also happen to have the lowest and highest median home prices, respectively, of the cities on the list. But take a look at New York City. Property taxes are fairly low in NYC, but that’s eclipsed by the incredibly high closing costs and homeowner’s insurance cost. This makes the first year in NYC a bit more expensive than San Diego, despite lower median home prices. Similarly, Philadelphia having the lowest property taxes on the list makes it the fourth cheapest city in the first year, despite relatively high closing costs and a slightly higher median price than the next cheapest, Houston, which also has more expensive homeowner’s insurance.

Plenty of people own pets, and no one thinks buying a pet is odd, even if they aren’t pet owners themselves. So the recent increase in pet purchases may have flown under the radar, but it’s there and it’s significant. The percent of households with at least one pet jumped from 64% in 2020 to 73% in 2021. The increase is being attributed to pandemic lockdowns — it’s likely that many people unable to meet with their friends wanted a pet to keep them company.

This means that homes that can accommodate pets are in higher demand. Pet-friendly HOAs or landlords are a plus for condo or rental seekers. For SFRs, a few factors are important for pet owners. They want fenced-in outdoor space so their pets can be outside without fear of them going missing. Having a doghouse is also a bonus. They usually want an extra bedroom for indoor pets, or at least more living space. This is also a general trend among recent homebuyers, but the decision to move seems to coincide with pet purchases.

Curb appeal is important for anyone trying to sell their home, since it’s the first impression prospective buyers have. Often, just cleaning up and taking care of your lawn is a big help, but it’s not enough if you’re competing with other sellers in the same area. Here are some hints to help you get ahead of the game.

For most people, the garage serves a practical purpose, holding your vehicles — or possibly just storage. But chances are the garage door takes up quite a bit of the outer facade of your home, and making it look nice could give a big boost to curb appeal. Repaint the trim or the garage door itself, or even fully replace the door if it’s showing signs of wear. Another functional-yet-aesthetic addition is lawn or patio furniture. Outdoor seating makes your home feel welcoming. On the more artistic side, yet still serving some purpose, are fixtures such as wind chimes or bird baths. Purely artistic sculptures also boost curb appeal. Whatever type of art features you use, it’s a good idea to position them symmetrically. There are some people for whom asymmetry as a certain appeal, but for most, symmetry is preferable. Once you have some ideas, it’s best to get a second opinion from friends or neighbors. Most homeowners have trouble assessing their own home with a critical viewpoint.

Many people dream of owning a beachfront property. The biggest thing holding people back is that they can’t afford it, since beachfront properties are particularly expensive. But there are other considerations to make before diving into a purchase, even if you think you can afford it.

First of all, you need to know why you want to own a beachfront property. And no, just being able to say you own it is not a good reason. Do you love the beach or the ocean and want to live right on the sand? Do you want a vacation property? Are you just looking for a lucrative investment? Renting out beachfront property is actually not easy. Being expensive to buy means it’s also expensive to rent, so most renters are going to be short-term vacationers. Your home isn’t going to be consistently occupied unless you’re the one living there, in which case you aren’t earning rent. But if you can afford to keep it, the return on investment when you eventually sell is going to be quite high.

Another concern is the weather risks of beaches. These areas are often significantly more prone to heavy winds and flooding than inland areas. Check out the area, be aware of the risks, and make sure to purchase insurance that protects against wind and water damage. And even if the building itself isn’t damaged, shoreline erosion over time can reduce your property values.

Almost 30 bills affecting real estate law either are being considered or have passed over the the past year. Among them, a few important ones passed just in the last couple months. We’ve mentioned SB 10 before; that’s the one that allows some areas to be rezoned for up to 10 units. Other important bills passed in September and October are AB 948, SB 263, and AB 345.

AB 948 and SB 263 are similar, but aimed at different groups. Both require anti-bias training for real estate professionals. The difference is that AB 948 applies to appraisers, while SB 263 applies to agents and agent applicants. AB 948 also makes discrimination by appraisers by protected groups illegal, and SB 263 establishes 45-hour long renewal courses. SB 263 goes into effect January 2023. AB 345 makes accessory dwelling units (ADUs) more similar to individual properties. It allows them to be sold separately from the primary residence.

The commercial sector, especially with regard to office buildings, is still recovering from the 2020 recession. Fortunately, the stats are showing a positive trend. The industrial market bounced back most readily, since warehouse space was still necessary even without storefront purchasing. Vacancy rates in the retail sector are still above pre-2020 levels, but it’s slowly dropping. Work-from-home has hampered recovery in the office sector, but the numbers are stabilizing.

The most significant changes over the year occurred in net absorption. Net absorption is the total amount of space that is occupied — regardless of how many separate properties that includes. For the industrial sector, net absorption is now in the millions of square feet across SoCal. It was already 3.9 million in the Inland Empire last year, but now it’s up to 6.9 million. Other areas were previously below 1 million. The largest increase, both in raw numbers and by percentage, was in Los Angeles county, which increased nearly ninefold from 417,900 to 3.7 million.

The most common mortgage loan length is 30 years, which offers the lowest monthly mortgage payments. But that isn’t the only option. Shorter-term loans require larger monthly payments, but they have other benefits.

Shorter loan lengths, such as 15- and 20-year loans, ultimately result in less money spent over the course of the loan. The reason is twofold: Not only are you paying interest for a shorter period of time, but shorter loans actually also have lower interest rates. The monthly payments will still be higher since it needs to be paid off faster, but you’re saving money in the long run. So, shorter-term loans are a good idea if you’re not worried about being able to make monthly payments. If you have concerns about making payments, consider talking to an accountant about your taxes. Mortgage interest and property taxes are both deductible, as long as you are itemizing. If you weren’t itemizing before, doing so may mean the extra monthly payment really isn’t all that much more.

Refinancing also doesn’t necessarily mean you have to start your payments all over again. It’s possible to switch to shorter-term loan as part of a refi. This is especially beneficial if your loan doesn’t actually have all that much time left. If at all possible, when refinancing for a lower interest rate, try to take a loan with the same length as the remaining life of your current loan. This will ensure that you’re definitely saving money in the long run. You may even be able to find even shorter loan lengths, such as 10 years.

The most surefire way to enlarge a space is, of course, to expand it. But what if you don’t have the lot size or the money to expand? There are still things you can do within the square footage you have to make our home seem bigger than it is.

A couple of these methods still involve renovation, but don’t require any additional space, since it’s all within the existing structure. If your kitchen has an island, consider removing it. Island kitchens can be fashionable, and offer more storage and counter space, but can make it harder to maneuver or make the kitchen feel cramped. Open floor plans also increased the perceived size of the property. Look for interior walls that don’t need to be there, such as between the kitchen and dining room, and think about cutting them out. Your space will look much bigger, and not only by the thickness of the wall.

If you don’t want to do anything too drastic, there are psychological effects you can take advantage of. Using see-through materials such as glass enables you to see more of your home’s square footage without necessarily being in the room. These can be glass room dividers, windows in doors, or even something as small as a glass staircase railing. Mirrors have a similar effect, reflecting the square footage behind you into your vision. Your choice of colors also matters. Painting the walls in a lighter color doesn’t change the size of the room at all, yet still makes it feel larger. You can even use lighter shades of wood flooring.

Once a transaction closes, new homebuyers are eager to get to the celebrating. Go ahead and celebrate, but don’t get ahead of yourself. While the real estate agent’s job is done, the homebuyer’s isn’t. Owning a new home also means many of your financial specifics have just changed. Don’t fall behind on your paperwork and payments because of out-of-date information.

Make sure your mortgage payments are properly set up. Verify the date of your first payment and get it in before it’s late. Consider setting up automatic payments to ensure that they’re on time. Your property tax amount also may have changed, and you’ll need to update your homeowner’s insurance.

There are also a couple things that may not need your immediate attention, but that you should be aware of. Loans are one thing that banks and other lenders often sell to each other. It’s entirely possible that who you owe money to will change, and this is especially important to keep track of if you are sending physical checks. The other thing to look out for is scams. They’re going to increase in frequency immediately after a sale, as scammers often try to pose as insurance companies selling home insurance or mortgage insurance.

Home prices are high, which means fewer prospective buyers are able to afford your home. But the buyers don’t necessarily realize that, without a solid grasp on their financing options. That’s certainly not your fault, but there are things you can do to make sure you are avoiding dealing with people who don’t have a chance. Specifically, take hints from the luxury market. Your home may not have been in the luxury market a few years ago, but it could be now. Even if it isn’t, some of these tips may still be useful for you.

Real estate agents can do a lot of the work for you, if you know what you’re looking for. A good real estate agent will encourage any buyer that they represent to get a pre-approval letter from a lender, regardless of their budget. If they don’t have one, you’re probably better off not dealing with them. The type of open house you have is a big factor. While traditional open houses give you the greatest number of options as far as potential buyers, most of them won’t work out or are just looking and aren’t even interested. Worse, they can open up your doors to potential thieves, who often target higher-end homes. Consider a broker’s open instead, which would be attended only by agents who already have a buyer who is more likely to be seriously invested in buying a home. That will also let you know who the agent is that’s working for them, a potentially important piece of information. If the buyer’s agent is a specialty luxury agent, they will have already vetted their client, since they have as little interest in you do in working with a buyer who can’t afford a high-priced home.

Major life decisions are always stressful, and selling your home is certainly no exception. But many sellers stress more than they need to because they haven’t properly prepared for the sale. While a good agent will be there to advise you, most decisions are ultimately yours to make, so you need to do your own homework as well.

Speaking of good agents, that’s the first thing you need to make sure of. Research agents who work in the area and discuss your goals with them. All agents have their own strengths and weaknesses, even if they don’t specialize, which many of them do. The best performing agent may not be the right agent for your particular needs. Ensure your agent knows whether you’re looking for top dollar or just need to sell fast, because that’s going to affect the listing price and timeline.

Your agent will hopefully provide you with an in-depth analysis of comparable properties. Even before you receive it, you should have a decent idea of your home’s value. If it’s drastically different from what your agent thinks, discuss that with the agent and try to reach an understanding. You could even find that you don’t actually want to sell because you’ll be making much less than you expected. Or maybe there are certain repairs that you didn’t feel were urgent, but may have a significant effect on your home’s value.

Once you start to receive offers, be smart and make appropriate adjustments. Read through the offers carefully, and look for a pre-approval letter if the prospective buyer requires a loan. A first offer doesn’t have to be final — don’t reject every offer with minor issues, but also don’t acquiesce to every buyer demand. Some deals simply won’t work out at all, but many can be negotiated through counteroffers.