The primary purpose of refinancing is in order to spend less money in the long term. It may seem like this is a good idea whenever rates drop even the slightest amount. However, it’s important to remember that you are technically originating a loan when you refinance, and doing so incurs the same fees. The upfront costs are what deter repeated refinancing.

Most of the fees are a few hundred dollars — unless otherwise specified, you can estimate they will be about that much. Since you are applying for a mortgage loan when you refinance, this requires both a mortgage application fee and a loan origination fee. The numbers vary, but typically, the the loan origination fee is 1% of the loan’s value. You will also need your home to be re-appraised, as lenders want to know the value of your home before approving a loan, which will require an appraisal fee. It’s also possible that your lender will require a title search, and you may need new title insurance, both of which incur fees. Title insurance, if required, could be $1000 or more.

With home prices as high as they are, qualifying for a loan becomes more difficult. This is especially true if your household is single-income. But that doesn’t mean it’s impossible. There are options available for low-income households.

As always, it’s important to check your credit score before attempting to get a loan. You can check it for free once per year from any major credit bureau. If your credit looks good enough to qualify for a loan, you can advance to searching for loans. For low-income households, the best place to look is government loans, since these usually have lower thresholds for down payments. Some FHA loans require only 3.5% down. Your specific region may also have government loan programs. If your credit score is low, however, consider looking for a co-signer for your loans. The co-signer doesn’t necessarily need to be the one paying, but if their credit score is better than yours, it will help improve your chances of loan approval and possibly even get you a lower interest rate on the loan.

There are two main reasons to refinance your home. One is to reduce your monthly payments in order to free up cash, and the other is to pay off the loan more quickly. But refinancing doesn’t just simply do this automatically; you have to choose a new mortgage with terms that work for you. Figure out what your goal is and pick the right mortgage.

Reducing your interest rate is the surest way to free up cash, but it can also simply be used to pay off the loan faster. With a lower interest rate, a greater percentage of the principal is reduced each time you make a payment. However, this only works if you can qualify for a lower interest rate. If you don’t qualify normally, consider reducing the length of the mortgage. This will probably result in higher monthly payments, but will also likely allow you to qualify for a lower rate, and almost certainly allow you to pay off the mortgage faster as long as you make the payments. If you have plenty of cash on hand and just want to save money in the long run, consider replacing your mortgage with one that allows you to make larger payments on your principal. This is more costly in the short term, but would allow you to pay off the loan early and thus spend less on interest, reducing the overall cost.

Many people are blindsided by rising mortgage rates after getting a preapproval, thinking that the preapproval has locked their rate. It hasn’t. The first opportunity to lock your mortgage rate happens when your final loan application is approved, though you don’t even have to lock it until shortly before closing on a purchase, if you think rates will go down. In addition, the lock period is not indefinite. It usually lasts anywhere from 15 to 60 days, and it could definitely take longer than that to find a home.

There are ways to mitigate the issues presented by shifting mortgage rates. Rates don’t tend to change much during a typical closing period, but you want to lock early when rates are rising and late when rates are falling. Consider budgeting for a loan lower than your preapproved amount in order to account for fluctuations in mortgage rates. Different lenders also have different locking policies. Make sure to shop around and ask about lock periods, renewing options for locked rates, and the possibility of locking out rising rates but not falling rates.

January 2022 showed a different face than we were seeing all last year. Of course, in many respects that’s a good thing. Depending on whether you’re buying or selling, the real estate market for 2022 could be wonderful or horrible. As always, the location will make an even bigger difference.

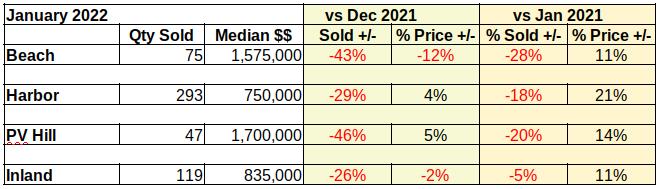

Sales Volume Dropping

Check out all the red ink in the table below. Compared to December, sales volume is down by nearly 50% at the Beach and on the Hill. November and December of 2021 were heavy with transactions spurred on by the fear of increasing interest rates. The number of homes sold in comparison to January of last year also dropped, though not to as great an extent.

Sales volume down, prices up

As of right now interest rates are expected to hover in the 3.5% to 4% range for the balance of the year. The increase from under 3% to roughly 3.5% has served to lock a substantial portion of entry level buyers into the rental pool. Those who found a place and could afford to buy last year did. The first part of this year is expected to continue to show declining sales volume as many first time buyers drop out of the purchasing market.

Prices Starting to Reverse Direction

Prices meanwhile are faltering in the unsustainable march upward. As the table above shows, the Beach and the Inland areas have already begun declines in the median price. Simultaneously buyers in the Harbor and Palos Verdes communities have continued pushing purchase prices higher, though not nearly as fast as last year.

We expect price corrections in all four areas as the year rolls out. Initially, we anticipate buyers in the Inland and Harbor areas to balk at the combination of higher interest rates and historically higher prices. Lower priced homes are traditionally impacted sooner and to a greater degree by changes in mortgage interest.

Homes on the Palos Verdes Peninsula and in the Beach communities of the South Bay are expected to also experience price declines as the market adjusts to the new reality of higher prices, steeper interest rates and the shrinking impact of Covid.

The Covid Connection

Covid wreaked havoc with social lives, business practices and just about every other aspect of society. When the pandemic struck in 2020 the real estate world was already heated because of low interest rates. Unfortunately, protecting society from Covid meant slowing down much of the business world, including real estate transactions. For months agents were dealing with masks, alcohol gel and the task of wiping every surface touched by potential buyers. And the buyers kept coming because the interest rates made buying a home affordable for many.

By the time 2021 started, the industry had found ways to show property and ways to consummate paperwork with relative safety from Covid. Keeping one eye on the mortgage interest rate, the buying public responded promptly. It was one of the busiest years ever for brokers and agents. As the year ended and lenders continued raising the cost of purchase loans, buyers started showing signs of stress.

January appears to have been the fulcrum point for a shift in market dynamics. The people involved are more than ready for relief from Covid. Bidding wars have all but ended. Price reductions are coming after only a few weeks on the market. The State has declared Covid “endemic.” Essentially we’re ready for normal business.

The first month of the year has pointed in the direction of a slowing market, with some pricing shifts to compensate for over-exuberant purchases in the close out of 2021. We anticipate February to show more of the same. We’ll be back soon with charts comparing the monthly progress. (You’ll find the beginning charts for 2022 at the bottom. Not real exciting without data to compare.)

The High Sale and the Low Sale

We’ve had requests for a little “human interest” added to the dry statistics we throw out here every month. We’re going to try to do that while still maintaining privacy for the people involved. Let us know how we’re doing.

For example, an observation we made this past month was the highest sale versus the lowest sale as reported by TheMLS for January. Those of you who follow us know the Beach areas are invariably at the top of the chart, so you won’t be surprised to find that the highest sale in January was in the Manhattan Beach hill section. New in 2021, this expansive 6 bed, 6.5 bath home sold for $6.5M. At nearly 6500 square feet, that’s over $1,000 per sq ft.

It’s far from the highest price we’ve seen there, but that piqued our curiousity. So we looked to the other end and found the lowest January sale in our part of the South Bay. Down from 6500 sq ft to 400 sq ft, and from $6.5M to $255K, this studio condo in Long Beach calculates out to a hair over $600 per sq ft. In other words, about 60% of the cost to build new construction in Manhattan Beach.

2022 Charts – The Beginning Point

The first chart of the year is less than exciting. We’ve included them here for reference. In March, when we can compare January to February and we can be confident we are past the bulk of the pandemic, these should be much more interesting and informative.

The most commonly used benchmark rate to determine mortgage rates has long been the LIBOR, or London Inter-Bank Offered Rate. However, this has some issues. The LIBOR is not tied to actual transactions. Because of this, bankers that have influence on the LIBOR can simply manipulate the rate to their benefit. This occurred in the 2008 recession, where the LIBOR was kept artificially low to encourage people to borrow money. The financial world has finally decided LIBOR won’t cut it as a benchmark, and it’s being phased out.

Financial institutions won’t be forced to stop using the LIBOR, but if they do use it, they will be required to include at least one rate that isn’t LIBOR-based as a backup. They will have until the end of 2021 to comply. The front runner for a backup rate in the US is the SOFR, or Secured Overnight Financing Rate. This rate is administered by the New York Fed. It’s not subject to the same manipulation that LIBOR is because it does take into account actual completed transactions. Fannie Mae and Freddie Mac already swapped from LIBOR to SOFR in 2020.

The most common mortgage loan length is 30 years, which offers the lowest monthly mortgage payments. But that isn’t the only option. Shorter-term loans require larger monthly payments, but they have other benefits.

Shorter loan lengths, such as 15- and 20-year loans, ultimately result in less money spent over the course of the loan. The reason is twofold: Not only are you paying interest for a shorter period of time, but shorter loans actually also have lower interest rates. The monthly payments will still be higher since it needs to be paid off faster, but you’re saving money in the long run. So, shorter-term loans are a good idea if you’re not worried about being able to make monthly payments. If you have concerns about making payments, consider talking to an accountant about your taxes. Mortgage interest and property taxes are both deductible, as long as you are itemizing. If you weren’t itemizing before, doing so may mean the extra monthly payment really isn’t all that much more.

Refinancing also doesn’t necessarily mean you have to start your payments all over again. It’s possible to switch to shorter-term loan as part of a refi. This is especially beneficial if your loan doesn’t actually have all that much time left. If at all possible, when refinancing for a lower interest rate, try to take a loan with the same length as the remaining life of your current loan. This will ensure that you’re definitely saving money in the long run. You may even be able to find even shorter loan lengths, such as 10 years.

While mortgage rates are certainly not high, we can no longer safely call them low. The average rate for a 30-year fixed conforming loan is considered low when it’s below 3%. They’ve been slowly increasing. In the first half of August, it barely qualified at 2.99%. Now, the number sits at 3.06%.

As a result of increasing mortgage rates, demand for refinances has also decreased, dropping by 5% as soon as the rate passed 3%. Applications for purchase loans are less sensitive than refinance applications, and dropped only 1%. Despite the decreases in number of mortgage applications, the total dollar volume is still high, as a result of high prices fueled by heavy competition.

Most people want to buy a home that’s move-in ready, but if you don’t mind buying fixers, there are a couple of finance options for you. This doesn’t mean just anyone can renovate a fixer — there’s a lot that goes into it, and you need to make sure you have the know-how or the money to pay someone who does. It can be expensive, and the payout is in the return on investment. If that’s much later down the line because you also plan to live there, that’s okay if you have the money, but it’s important to keep that in mind.

If you don’t have the money, you still need at least a decent credit score. There are two kinds of mortgages designed with home renovation in mind. The 203k Mortgage, one type of FHA loan, is meant for a vast array of different construction projects. In order to secure one, though, you’ll need a credit score of at least 580. Fannie Mae has a loan type specific to renovations, called the HomeStyle Renovation Loan. The max borrow amount is 50% of the total value of the home, and it’s possible to borrow against projected equity. It requires that the renovation be completed within 12 months, and necessitates a credit score of 680 or higher.

2020 saw a large increase in mortgage originations, particularly refinances, as a result of low interest rates. It was expected that this would start to fall off in 2021, since interest rates are starting to go back up. However, they’re still low enough that refinances continue to be common. The statistics are a bit misleading for purchases, though. Low inventory is boosting home prices, accounting for a significant part of the increase in loan origination dollar amount even beyond increasing the number of loans originated.

Something is still missing, though. Even though much fewer loans are delinquent now than in 2020, the share of them that are over 90 days delinquent is increasing. This is because people continue to tread water through moratoriums, but aren’t earning any money. Jobs still haven’t recovered from 2020. Foreclosure moratoriums and forbearance programs are going to end eventually, and that’s going to be a problem for some people who have lost their jobs during the pandemic and haven’t been able to find work yet. If home prices continue to rise without an actual jobs solution, these stopgap measures are going to be the proverbial dam that causes the market to crash when it breaks.

Buying a home can be a stressful process, especially if it’s your first time. But there are several things you should consider beforehand to make sure you know what you’re getting into. If you come up with a solid plan, you won’t be as nervous when it comes time to make an offer.

The first thing you should do is check your credit score. If your credit score is below 620, private loans may be more difficult to acquire or come with high interest rates. Having poor credit may not be a good thing, but at least by knowing your credit score, you know you’ll be looking at a government-backed loan. If your credit score is good, you’ll have more options.

Examine your long-term budget closely. Keep records of income and expenses, and gather together your financial documents, such as pay stubs and tax returns. Not only will this help you personally understand your budget, some of these documents are used by lenders for prequalification or preapproval. Prequalifications estimate your ability to pay to give a solid idea of what range of prices you can probably afford. Preapproval is the next step, after you’re more sure of an area and timeframe in which you want to buy. Once you know what your options are, you need to research all of them. If you can, go to multiple lenders and shop around for the best interest rates. Be sure to ask questions.

Even if you get a preapproval, that doesn’t mean you can immediately breathe a sigh of relief. Preapproval is based on your current levels of income and expenditure. Lenders will be consistently re-checking these until the loan closes. If you make any sudden financial moves, they will know, and your credit score will suffer. Not to mention you may not actually be able to afford the house you plan to buy if you suddenly lose your income due to quitting your job, or drop a bunch of money on new furniture. If you are considering something major, call your lender and discuss it with them, before you decide to do it.

If you’re looking to buy a house, unless you intend to pay cash, you’re going to need to get a loan. One obstacle to getting a loan is having a low credit score — if lenders don’t trust that you’ll be able to pay them back, they won’t want to give you a loan. Even if they are willing to lend you money, they will do so at a higher interest rate. Your credit score ranges from 300 to 850, with 800 or above being considered excellent credit, though most people have a credit score between 600 and 750. If you want to know your credit score, or check for errors or fraud, you are entitled to one free annual credit report on AnnualCreditReport.com from each of Equifax, Experian, and TransUnion.

The easiest way to ensure that your credit score doesn’t drop is to make bill payments on time. You may think that as long as the payment gets made, it doesn’t matter if it took a bit longer to get the money to them. That’s not the case, as payments made 30 days late or more can stay on your credit report for up to 7 years. If you are allowed a minimum payment, such as on credit card bills, even making the minimum payment on time is better than waiting until you have the full amount. If you do find yourself in debt, paying down existing debt will also increase your credit score. One thing that you may not realize affects your credit score is the timing of applying for cards. If you apply for several credit cards in a short time period, it looks like you’re wanting a large amount of cash very soon, and may not have the money to pay back loans.

The FHA has its origins in the Great Depression, as a method for people down on their luck to secure a loan without much upfront cost. Given the current recession’s similar circumstances, it may be expected that FHA loans would increase in popularity around this time. That isn’t the case at all, because now there’s competition. FHFA loans — those backed by Fannie Mae or Freddie Mac — are currently a better deal.

The normally low upfront cost of FHA loans is countered by the fact that they have mortgage insurance premiums (MIPs), part of which is an upfront cost. This means that you are spending more over the life of the loan than with a conventional loan even with an equal interest rate. This MIP can be cancelled after 11 years if the down payment was at least 10%. However, the appeal of an FHA loan was the minimum down payment of only 3.5%, so this circumstance rarely came up.

But now, 3.5% isn’t even the lowest minimum down payment. FHFA loans have adopted a 3% minimum. What’s more, their upfront costs are actually lower, with no upfront mortgage premium. The MIP cancellation criteria are also different: The down payment amount and loan length don’t matter, and it can instead be cancelled whenever the home equity reaches 80%. Given that it’s rare for a house to be owned for 11 years, especially for first-time buyers who benefit the most from low down payment minimums, this flexibility is highly attractive.

I’m sure you all know that when you take out a mortgage loan, you pay back the principal plus interest over the life of the loan, in monthly payments. But it’s important to understand that monthly payments are not simply the principal plus interest divided by the total length in months. Because the amortization schedule ensures that each monthly payment is the same amount, it may appear as though each payment is identical. However, this is not the case.

Amortization schedules determine what percentage of each monthly payment is principal and what percentage is interest. When you first get a loan, nearly the entirety of your monthly payments are used to pay off interest, with scarcely any reduction in the principal. As you pay off more of your interest over the life of the loan, a greater percentage goes towards the principal. When you sell a home that still has a mortgage, the amount of money you receive due to equity depends on how much of the principal amount is paid off. If it’s still very early in the loan’s lifetime, you haven’t paid much of the principal, so your equity will be quite low.

The FHA has increased the loan limits for every category in 2021, a boon to prospective homebuyers who may have been negatively impacted by the recession that came with the COVID-19 pandemic. The two primary categories of loan limits are low-cost area and high-cost area, and each category has separate limits for SFRs, duplexes, triplexes, and quadplexes.

For low-cost areas, your loan limits have gone up approximately between $25,000 and $47,000. The SFR limit went from $331,760 in 2020 to $356,362 in 2021. The duplex limit went from $424,800 to $456,275, triplex $513,450 to $551,500, and quadplex $638,100 to $685,400. High-cost areas saw an increase between about $57,000 and $110,000. For SFRs, it went from $765,600 to $822,375, duplexes from $980,325 to $1,053,000, triplexes $1,184,925 to $1,272,750, and quadplexes $1,472,550 to $1,581,750.

In order to qualify for any FHA loan, the requirements you’ll need to meet include credit score, down payment amount, and debt-to-income ratio. The credit score minimum is 500. If your credit score is below 580, you need a minimum down payment of 10% of the purchase price, otherwise the minimum down payment is 3.5% of purchase price. The maximum debt-to-income ratio for all debt is 43%, and 31% front-end. In addition, you must have an FHA appraisal and home inspection, cannot purchase and resell the home within 90 days, and must use the loan for a primary residence.

With interest rates being low, many people are going to want to refinance or secure a new loan while they’re able to get a rate under 3%. They’re going to need to act quickly, though, since rates are starting to go up and the average is currently hovering around 3% for a 30-year fixed rate loan. But what if you’re in forbearance or were forced to declare bankruptcy as a result of economic pressures? Can you still refinance or get a loan? The answer is, well, maybe. There are different categories of lenders and different requirements.

If you’ve been able to keep up with your payments despite being in forbearance, you shouldn’t have issues qualifying, especially if your new loan is backed by the FHA or FHFA. You can also qualify immediately for an FHFA loan if you’re able to repay any missed payments in a lump sum, though FHA loans have a waiting period for lump sum repayment. If your new loan isn’t backed by a federal agency, the requirements could vary widely, but they’re generally more understanding about losses due to economic situations outside of your control.

If you had to file for bankruptcy, you will probably have a waiting period. If the pandemic was the sole cause of your bankruptcy, you may be able to get a new loan immediately from non-federal lenders, but the interest rate will likely be higher. For FHFA loans, the wait period is generally four years from the discharge or dismissal date for Chapter 7 bankruptcies. For Chapter 13 bankruptcies, it’s still four years from the dismissal date, but two from the discharge date. In either type of bankruptcy, the four years may be reduced to two if a one-time event out of your control is what caused the bankruptcy. The periods are lower for FHA loans — two or one year from a discharge, or zero from a dismissal for Chapter 7. It’s possible to qualify for a loan, with bankruptcy administrator approval, after being in the repayment period for at least one year of a Chapter 13 bankruptcy.

The Consumer Financial Protection Bureau (CFPB) is planning to make some changes aimed at widening the accessibility of mortgage loans by allowing lenders more freedom in determining a borrower’s ability to repay. Currently, one of the requirements for a qualified mortgage (QM), the loan type preferred by both lenders and consumers, is a debt-to-income ratio of no more than 43%. This criterion is designed to be an indicator of the borrower’s ability to repay. However, there are other methods of determining this that can broaden the range of QMs. The CFPB’s solution is to compare the loan’s annual percentage rate (APR) to the average prime offer rate (APOR). Because a borrower with a high DTI would likely also have a high APR compared to APOR, DTI considerations are still indirectly included, but there will also be people with a high DTI but low risk of default that are able to get a good APR to APOR ratio and therefore successfully get a QM loan.

As a result of home sales volume dropping by 30% in Quarter 2 of 2020 from 2019, loan origination has also dropped considerably. The effect was somewhat lessened by low interest rates, which resulted in more refinances. The commercial sector, however, didn’t have that luxury. The Mortgage Bankers Association (MBA) forecasts a 59% decrease from 2019 in total commercial loan amount, from $601 billion to $248 billion. The majority of this will be from the multi-family sector, which was at a record high of $364 billion in 2019 but is only expected to reach $213 billion this year.

Lenders are optimistic, though, as long as governments can continue to keep people housed. Vacancies aren’t great for lenders, as they reduce the prospects of landlords, and recently evicted people certainly won’t be looking to originate new home loans any time soon. The MBA expects 2021 to bring the number up to $390 billion for commercial loans. The catch is that commercial landlords aren’t protected by the recently extended foreclosure moratorium. If multi-family homeowners are hit with a foreclosure, all their tenants will be affected as well. Commercial property owners as well as lenders are looking for new methods of loan accommodations.

There are two types of mortgage loan insurance, and it’s also possible to avoid needing insurance. Mortgage insurance premiums (MIP) are the type of insurance required by the Federal Housing Authority (FHA). The other type is private mortgage insurance, or PMI. It’s easier to qualify for FHA loans, but private loans come with some additional benefits if you do qualify. Most notably, it’s only PMI that you can avoid; if you only qualify for an FHA loan and not a private loan, MIP can’t be ignored.

Private lenders generally have stricter credit score requirements than the FHA. In return, the higher your down payment, the lower your premium amount. Furthermore, if your down payment is at least 20%, you aren’t required to get loan insurance, so you avoid paying PMI. If you’re getting an FHA loan, you’re stuck with MIP for at least 11 years. On the bright side, the down payment amount to qualify for a reduction to 11 year MIP is 10%, not 20%.

Generally, the greater you can make your down payment, the better. Of course, paying all cash to avoid a loan at all is ideal, but not everyone can afford to do that, so keep in mind the important breakpoints. If you qualify for a private loan, putting at least 20% down is probably your best bet. Even if you only qualify for an FHA loan, be sure to put at least 10% down so that you aren’t stuck with MIP for the entire duration of the loan.

The Federal Housing Finance Agency (FHFA) announced in August that it would be charging an additional refinancing fee to offset losses due to COVID-19. The new fee was expected to come into effect yesterday, September 1st, but at the last minute, the FHFA rescheduled it to December 1st. We’re still in the midst of a recession, so the FHFA doesn’t want to make too many changes too early.

The new fee exempts refinance loans with balances below $125,000, affordable refinance products, Home Ready, and Home Possible. Applicable loans, which are cash-out and limited cash-out refinance loans, will have 0.5% added to each transaction. While this fee applies directly to lenders, it also indirectly affects borrowers in the form of higher interest rates. While the FHFA certainly wants to recoup their projected $6 billion in losses, they’ve agreed that now is not the time; the economy still needs to recover first.