The high mortgage interest rates we’ve been experiencing have been the result of benchmark rate increases by the Federal Reserve. The benchmark rate isn’t directly tied to mortgage interest rates, but the benchmark rate does have a strong effect on interest rates. Now, though, no more rate hikes are expected, which should cause interest rates to level off, and then start to decline.

This levelling off followed by a decline is exactly what the Fed was aiming for with the rate hikes. It’s impossible for mortgage rates to drop without the real estate market, and in turn the economy as a whole, taking a hit. By raising rates above what they should be during a period of high prices, what the Fed has done is soften the blow by allowing the decline to be more gradual. Of course, this comes at the cost of significantly decreased affordability for the period of the rate hikes. Once interest rates fall below 6%, which should happen before the end of the year, the market should pick back up again. However, the effect may not be noticed until next year, as the end of the year is not generally a time of heavy market activity.

Builders have had it rough the past few years. The pandemic resulted in skyrocketing lumber prices as well as many job losses for construction workers. In order to get the most bang for their buck, builders started building luxury homes, which generally have a higher profit to cost ratio. But this couldn’t last long, as both market demand and legislation pressured them towards construction of affordable living homes, while at the same time, zoning restrictions made even this rather difficult.

Pressures on construction companies have started to ease up in most of the country, but not everywhere. Particularly in the West and Northwest, available land is an issue. Fortunately, builders may have figured it out and now have a new plan: Make smaller homes. It’s predicted that more affordable starter homes will become available within the next year or two, as 42% of builders are reducing the square footage of their homes. It doesn’t even require a big change — the nation’s largest homebuilder, D.R. Horton, is only reducing home sizes by an average of 2%. Builders are also planning to build more townhomes and duplexes, which take up significantly less space per unit than single-family residences.

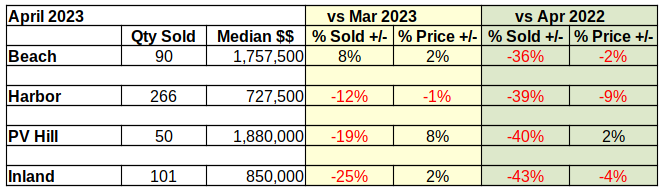

April of 2023 ended with a 40% drop in the number of homes sold across the South Bay compared to 2022. The median price was down 20% from last year in Palos Verdes and is up by a mere 1% at the Beach. Year to year median prices across the South Bay are down approximately 5%. Cumulative sales revenue for the first four months across the South Bay has dropped 39% from 2022 numbers.

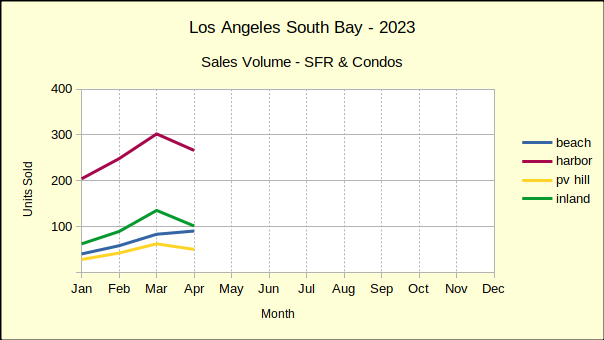

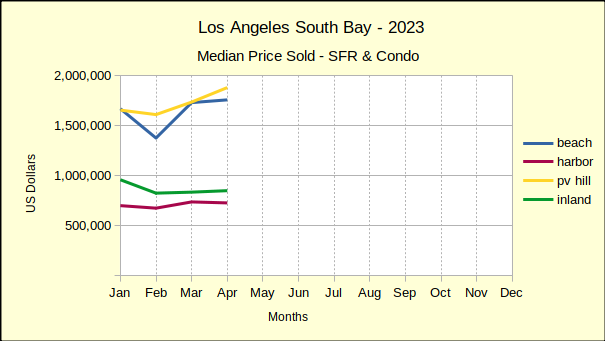

Year to date, 2023 has been one of the slowest markets we’ve seen in recent years. Sales are off by 43% in the Beach Cities and are down by 22% across the South Bay compared to last year. Median prices escalated dramatically in 2021-2022, and are still above those of 2019 by 30-35%. However, the median has fallen in all four areas since late last year. We anticipate the median price continuing to drop until interest rates seriously decline again.

Business in the years between 2019 and 2023 was seriously impacted by the pandemic, and the massive government funds released to counter the effect of the pandemic. Looking back at 2019 and comparing it to 2023 offers a perspective on where the market is and where we can expect it to go during the balance of the year. Today we see a huge decline in the number of homes being sold. That has yet to translate into a significant decline in median prices, although 75% of year over year sales show prices falling.

At the same time the Average Days On Market (ADOM) has increased from about 7 days during the sales boom of 2021-2022 to about 30 days now. That’s a four-fold increase in the amount of time it takes to sell a home. For a seller who needs to move, that will feel like an eternity. It’s that sense of urgency that drives prices down and ultimately results in a shift of the market.

At the Beach “Sticky Prices”

Sellers in the Beach Cities had a good month in April—at least compared to March of this year. Compared to April of last year, the picture is far worse.

The number of homes sold in April was up 8% compared to March. That sounds positive, until the realization that sales volume was down 36% compared to April of 2022. At the same time, the median price was up 2% versus last month, and down 2% compared to the same month last year.

There’s a lot of talk among brokers these days about “sticky prices.” Recent sales at the Beach offer a good example of what that means. The statistics show that sales are down 36% from last year, however prices have only dropped 2%. Sales are falling because the number of viable buyers is down.

Interest rate increases have pushed the most tenuous group of prospective buyers out of the market. At the same time, sellers are still revelling in the boost to median prices that came with record low interest rates during the pandemic. Beach area sellers have yet to adjust to the reality of a re-trenching economy. That adjustment is “sticky prices.”

Harbor Sales and Prices Off

The neighborhood can affect how long it takes the median price to respond to changes in the economic environment. While sales volume and pricing has remained strong at the Beach, sellers and buyers in entry level communities are impacted more immediately by shifts in the economy.

Thus we see the give and take of the market bring median prices into a stable range early in the year in the Harbor area. The red line in the median price chart below shows four months of reasonably steady prices. While month over month prices have shown only a 1% drop, the monthly sales volume has taken a 12% dive from March, as shown in the Sales Volume chart, above.

The monthly decline in sales was multiplied in the year over year statistics. April sales volume was down 39% from April of 2022. For the same period, the declining sales volume was coupled with a 9% drop in median price. So the entry level communities demonstrate a much quicker and deeper response to changes in the financial picture.

Part of that response is the time on market, which has risen from 15 ADOM in mid-2021 to 26 ADOM in April of this year. The increasing time required to sell homes contributes to the number of homes available on the market. Both factors contribute to falling purchase prices.

Palos Verdes In Extremes

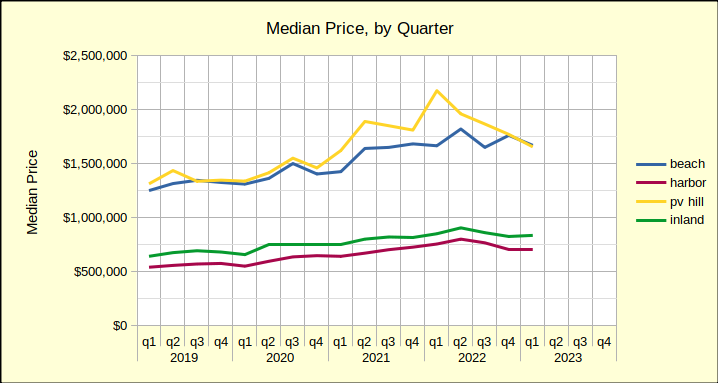

Through 2021 and 2022 home prices on the Palos Verdes peninsula benefitted from the Covid pandemic more than any area in the South Bay. In the median price by quarter chart, shown below, the yellow line is seen jumping up and away from the blue line of the Beach Cities. Unfortunately for home owners on the Hill, that price boost has already pulled back into line with prices of Beach area homes.

Comparing the first four months of the 2023 to 2022 median prices on the Hill have dropped 16%. It’s a steep decline in view of decreases at 3% and 6% in the Inland and Harbor areas, respectively. Even more so when looking at the 1% increase at the Beach.

The statistics look much better when comparing Palos Verdes sales from 2023 to statistics from 2019, the last “normal” year of real estate business. Sales volume on the Hill is down a modest 13%–modest by comparison to the Beach, which is down 43%. In contrast, median prices in 2023, compared to 2019, are still showing positive growth of 30%.

So, if one were to take the Federal Reserve System position that 2% annual growth is a desirable target, where would prices be today? The median price in Palos Verdes in May of 2019 was $1.5M. Jump forward to 2023 and that becomes about $1.6M. The median on the Hill last month was $1.9M, which suggests further price reductions.

Inland – The Steepest Fall

From an investment perspective, homes in the Inland area of the Los Angeles South Bay are “bread and butter.” These are the homes, much like those in the Harbor area, which reliably increase in value over long periods of time at a slow and steady rate. Most importantly, they house the bulk of our community.

In the short term, Inland home sales volume is down 25% from March to April of this year. Median prices are up 2% for the same period. This is the steepest fall in number of homes sold in the four areas charted.

Year over year, sales volume is off even more at 43% below April of 2022, and prices similarly down by 4%. We expect a seasonal boost to sales for the second quarter, when families most frequently schedule moves. Beyond that, most predictions are for continued softening in the real estate market as the Fed struggles with inflation. (The April Consumer Price Index, [CPI-U] for Los Angeles metro was 5.2% for Housing.)

At the start of May, the Federal Housing Finance Agency (FHFA) modified the fee structure for loans guaranteed by Fannie Mae or Freddie Mac. The goal of the change was to increase the accessibility of homeownership to disadvantaged groups. In order to achieve this, fees were reduced for low-income borrowers, first-time homebuyers, and those with credit scores below 680.

However, reducing some fees meant needing to increase fees elsewhere. Fees increased significantly for middle income earners, those making larger down payments, cash-out refinance applicants, and second-home buyers. Critics argue this is a bad idea, since middle-income earners are more ready to buy and less risky to lend to. But despite the fee increases for middle-income earners, fees are still lower the higher your credit score — that hasn’t changed. If the changes push middle-income earners away, the effect is probably psychological, not necessarily financial.

This year has not been a good year for banks. City National Bank settled for millions early this year. In March, two major banks — Silicon Valley Bank (SVB) and Signature Bank — went bankrupt. These weren’t the only banks to fail, but they were the most well known. Now, First Republic, the largest bank to fail since Washington Mutual in 2008, has been added to list of failed banks. After First Republic failed, it was briefly taken under government control before being auctioned off. JPMorgan Chase, who had also purchased Washington Mutual when it failed, is the new owner of First Republic. The entire situation with First Republic has cost the Federal Deposit Insurance Corporation (FDIC) about $13 billion.

However, analysts and federal regulators emphasize that the banking crisis has calmed down, now. When SVB and Signature Bank failed, fears were warranted. But those failures sparked an inquiry into which banks were likely to fail, and First Republic was identified as a likely candidate early on. So, this wasn’t entirely unexpected, and regulators were able to act quickly. Additionally, the FDIC admits that SVB’s failure was partially their fault, as they had not been meticulous in their supervision. Analysts aren’t expecting any additional major bank failures in the near future.

There was a time that smaller homes and multi-family living were common in Long Beach. Over the decades, that has transitioned to condos and then to single-family residences. But in 2020, Long Beach municipal codes were revised, reducing the minimum square footage requirement to just 220 square feet. The original aim was probably not co-living, which wasn’t on the radar given that it occurred around the start of the pandemic. Nevertheless, builders now are seeing the opportunity to build apartment buildings consisting of small units with shared common area.

Derek Burnham is a former Long Beach city planner and now works at a development firm, and is excited about the idea. Burnham has already planned about 48 units, which are going to be roughly the same size as hotel rooms, around 350 to 500 square feet. The target audience for this project is people who want to be near jobs and transportation, but can’t afford the typical apartment or condo unit. But builders don’t yet know how receptive people will be to it — after all, the transition away from shared living towards single-family residences was cultural and not pragmatic. Because of this, the plans are flexible, allowing anything from private units to shared units to miniature family units.

Two measures went into effect this spring, Measure GS in Santa Monica on March 1st and Measure ULA in Los Angeles on April 1st, both of which enact an additional transfer tax on the sale of very expensive homes, dubbed the Mansion Tax. Measure GS affects properties sold at over $8 million and Measure ULA has two tiers, one affecting properties sold at over $5 million and another affecting properties sold at over $10 million.

Prior to these measures, the transfer tax in both cities was a small dollar value per $1000 of purchase price regardless of property value. Including county taxes, this value is $5.60 in Los Angeles, and Santa Monica has two tiers, one at $4.10 per $1000 and another at $7.10 per $1000. Measure GS added a third tier to the Santa Monica system, which is a significantly higher $56 per $1000 value for homes over $8 million. Los Angeles still only has one base value of $5.60 per $1000, but with an additional tax of 4% for homes between $5 million and $10 million, and 5.5% for homes over $10 million.

The business lobby in California, and in particular the California Chamber of Commerce, has had quite a lot of success taking down bills that they deem “job killers.” Many of these bills are not at all designed to kill jobs, but rather to improve conditions for employees. To the business lobby, these are the same thing, but these are often the types of bills that the majority of the populace in California would tend to support.

One of the bills the California Chamber of Commerce is targeting is a bill to tax total wealth on individuals with a net worth of $50 million or more. Introduced by Milpitas Democratic Assemblymember Alex Lee, the bill would be the first of its kind if it passes. Obviously, there have been taxes on income, but so far, none on net worth. Lee’s argument is that the stocks and properties owned by the ultra-wealthy allow them to legally borrow and transfer funds in a way that avoids a significant percentage of income taxes. According to the chamber, this would simply convince the ultra-wealthy to leave California, rather than increase tax revenues.

The second bill was proposed by Los Angeles Democratic Senator María Elena Durazo. The bill would increase the minimum wage for health care workers to $25 per hour. According to Durazo, health care workers — especially whose who are women or people of color — frequently take home poverty wages, despite working multiple shifts due to being understaffed. The chamber argues that increased payroll costs for health care facilities would simply be passed onto patients, reducing health care affordability.

The chamber has a similar argument against the proposal to increase the required minimum paid sick days offered per year from three to seven, claiming that either the costs will be passed to consumers or the employers will cut benefits or lay off workers. Long Beach Democratic Senator Lena Gonzalez, who introduced the bill, says that the current sick leave is not adequate and forces employees to either forego pay to stay home or risk infecting coworkers.

For the past couple of years, house prices had been rising dramatically across the country. Here in California, we’re now starting to see prices drop since the start of this year. Prices are now falling in all 12 major housing regions west of Texas, as well as in Austin, TX. The same can’t be said everywhere, though. In the 37 largest metros east of Colorado, excluding Austin, TX, prices are still rising. Of course, markets can differ drastically by state, but such a clear divide between eastern and western US may be unprecedented.

Falling home prices was the expected result of the federal benchmark rate hikes. It seems to be working in the western US, as prices become too unsustainable to continue to increase. The regions with the most significant price drops are the ones that were rather expensive. But there are still other factors at play in the eastern US, driving prices still upward. Some areas, such as Hartford, CT and Buffalo, NY, never reached unsustainable home prices and remain rather affordable. They also have rather low inventory. These factors combined are keeping prices from dropping, leading to an 8% increase in prices in January. Florida is attracting many new employees with multiple financial companies relocating to Miami in 2021 and 2022. Prices are expected to eventually start falling even in the east, but don’t expect anything drastic. Low inventory across the country is preventing any sudden market collapse.

SB 9, also called the HOME Act of 2021, is a California law requiring cities to allow homeowners to subdivide lots into potentially up to 4 units. This law makes it significantly easier to built accessory dwelling units (ADUs). Huntington Beach has decided it doesn’t like this, and is willfully ignoring the law, stating that they won’t process ADU applications. The City Council has even gone as far as to enact an ordinance declaring that they are exempt from some of the requirements of the Housing Accountability Act (HAA). The HAA streamlines the approval process for low- and moderate-income housing. Huntington Beach is not compliant with HAA requirements, and so the city is attempting to declare that the regulations simply don’t apply to them.

This is entirely illegal on the part of Huntington Beach, and so naturally, it hasn’t gone over well. The city has received letters from the Department of Housing and Community Development (HCD) and has been sued by the California Office of the Attorney General (OAG). Knowing that the state does have authority in this regard, the Huntington Beach City Council is starting to backpedal. But this probably isn’t the end, nor was it the beginning. Huntington Beach has already been sued previously by the state for housing law violations, settling in 2020 and losing millions of dollars in state funding.

The California Housing Finance Agency (CalHFA) recently launched the Dream For All Shared Appreciation Loan, a secondary loan to be used in conjunction with CalHFA’s Dream For All Conventional first mortgage. This secondary loan carries its own set of requirements, which may or may not differ from the initial Dream For All Conventional first mortgage. The requirements of the secondary loan are provided here, but you should consult with CalHFA to be sure that you meet all requirements. The requirements are provided for two categories, both for the borrower and for the property.

The borrower must be a first-time homebuyer, which CalHFA defines as not having owned and occupied a home in the past three years. The borrower must also occupy the property as their primary residence and meet income limits for the program. In addition, the borrower, or at least one of the co-borrowers if there is more than one, for any CalHFA first-time homebuyer loan must take a CalHFA approved Homebuyer Education and Counseling course. This course does have a fee, which varies by method and agency, and can be done online or in-person. The Dream For All program also has its own additional course. Fortunately, this course is free, but it is only accessible online.

The property requirements are simple for single-family residences and manufactured homes, which are both allowed, but may be more complex for other types of properties. Condominiums must also meet the guidelines for whichever initial mortgage you choose. Guest houses, granny units, and in-law quarters may be eligible, but would not be eligible in addition to the main residence, since the property must be only one unit.

You’re probably aware that the Federal Reserve has been repeatedly hiking up interest rates. The idea behind this anti-inflationary measure is that increasing interest rates will result in lower consumer spending, which will force prices down to recover demand. The Fed’s eighth and most recent benchmark rate increase was on February 1st, just a couple days ago. However, this increase was the lowest of the series — only 0.25 percentage points, compared to prior increases of 0.75 or 0.5 percentage points. This is because we’re starting to see the desired result, decreases in inflation. It’s not enough to stop cold turkey, but it’s enough to reduce the pressure on interest rates.

But what else has the increasing benchmark rate done, besides reduce inflation? Well, obviously it has increased interest rates. This includes credit card rates, auto loan rates, and some student loan rates. Up until recently, it has also included mortgage rates. But mortgage rates are only indirectly affected by the benchmark rate, and they’re actually starting to decrease now. Another rate indirectly affected by benchmark rates is the savings rate. You’ll start to earn more money from savings accounts and certificates of deposit. It’s important to note, though, that with inflation being as high as it is right now, it has already entirely negated the effect of this savings over time, so you’ll have to save for quite some time for it to matter.

City National Bank, based in Los Angeles, was accused of refusing to underwrite mortgages in predominantly Black and Latino communities. The Justice Department alleged that this occurred between the years of 2017 and 2020. They used two major pieces of evidence: First, other banks operating in the same areas with predominantly people of color received six times as many mortgage applications during this time period. Second, of the 11 branches City National opened in the past 20 years, only one was in a neighborhood with predominantly people of color, and this branch did not have a designated underwriter. While it’s theoretically possible that City National Bank simply doesn’t have many customers that are people of color, discrimination is a likely reason for that.

While City National Bank denied the Justice Department’s allegations, they seemed cooperative with the investigation. They claimed that they supported efforts to ensure equal access and readily agreed to a settlement. The terms were a $29.5 million loan subsidy fund for Black and Latino borrowers as well as an outreach campaign costing $1.75 million. The 31.25 million dollar value makes this the largest settlement ever for the Justice Department.

Wells Fargo is one of the biggest banks in the nation as well as one of the top mortgage lenders. In fact, it was the number 1 mortgage lender in 2019. However, that’s about to change. 2019 was also the year that Wells Fargo acquired a new CEO, Charlie Scharf, who inherited a company under strict scrutiny as a result of a 2016 fake account scandal. Among the changes Scharf is making is a massive shift away from mortgage lending to focus mainly on investment banking and credit cards.

According to Wells Fargo exec Kleber Santos, investigations into the 2016 scandal also revealed that their mortgage lending business was simply too large in scope. The implication is that it was too difficult to manage oversight of all the facets of the company, and that mortgage lending was the one that needed to be trimmed down. Wells Fargo will not be completely eliminating its mortgage lending business, but it will be cut down dramatically to prioritize existing customers and borrowers in minority groups.

The California Department of Insurance (CDI) has provided the latest update to their resources on the effect of wildfires on insurance. Statewide data on policy counts is now available for 2021, and county-level and zip code-level multi-year data has been updated to 2021, going back to 2015. You can also view archives of older statewide data up to 2015. In addition to policy counts, the CDI has compiled updated info on coverage limits, premiums, losses, and claims.

Also available are additional resources for those wanting to know their wildfire risk or looking for insurance. A report with a large amount of data, including but not limited to coverage amounts and losses for each zip code, is available for download under the “SB 824 Wildfire Risk Information” header of the CDI’s Rate Filings page. This data is from 2018-2019. There is also a list of insurance companies offering incentives for wildfire safety, last updated in November, as well as a searchable list of insurance companies and real estate agents that work with high-risk areas.

When the lockdowns hit, homeowners very quickly realized what their homes were lacking in terms of comfortably getting through the lockdown period. The result was a shift in which home features were most in demand. People began to favor more outdoor space so they weren’t stuck inside, home amenities, and variable living space, among other things. While the virus certainly hasn’t disappeared, lockdowns are no longer in effect, masks are no longer mandatory in most cases, and people are gathering together more. But the lockdown-era trend shifts continue to be apparent.

Backyards are a popular feature, with 22% of listings highlighting them. Patios and pools are also the focus of an increasing amount of marketing, with 13% of listings mentioning patios and 11% calling attention to the pool. Home gyms are also increasing in popularity. Of course, this doesn’t prove that buyers want more outdoor space and home amenities, but it does say that’s what agents think buyers are looking for. The same is true of multipurpose spaces. The ideal kitchen now includes a kitchen island, which has the flexibility to be used as a dining area, workspace, or entertainment table. It’s even extending to the way the home is organized — open-concept living had been popular for a while, but it’s now fallen out of favor as people realized they had no private or quiet spaces with everyone at home at the same time. The motivation for this shift is no longer present, but the experience seems to have changed peoples’ minds about open-concept living.

In the last 80 years, a particular species of salmon, the Chinook salmon, has not been found in the wild in one of its previously most important areas, the McCloud River in northern California. The Chinook salmon has been endangered since 1994, possibly as a result of dam construction, but it’s gotten worse in recent years. They’re also dying off in the Sacramento River, which is becoming too warm for many young salmon to survive. Now, a joint conservation effort between the State of California, the federal government, and the Winnemem Wintu Tribe of Native Americans is looking to reintroduce Chinook salmon to the McCloud River.

There isn’t anything wrong with the McCloud River itself. It’s still a good spawning point for Chinook salmon, even with climate change threatening young salmon in the Sacramento River. The problem is that they can’t actually get out because of the dams. This new conservation effort seeks to aid them with human intervention. They transported 40,000 Chinook salmon eggs to the McCloud River and measured how many spawned. About 90% of the eggs hatched. The next step was to help them along their migratory route when it came time. In order to do this, they’ve recaptured the salmon along their migration, bypassed the upper Sacramento River, and redeposited them in the lower Sacramento River. This has been successful, but the next step is still a work in progress. The group hasn’t quite decided the optimal way to get the adult salmon to return. Options include an additional recapture and redeposit, the construction of a fish ladder, or the demolition of some dams. The first two options would use a route across the Shasta Dam, while the last would involve smaller dams and a new route.

In recent years, a few states have created laws regarding pay transparency in an effort to reduce discriminatory wage gaps. Colorado was the first to introduce a statewide law in 2019, though it didn’t take effect until 2021. New York City’s law will soon expand to all of New York. A new law just took effect in Washington as well as our own state, California, on January 1st. California’s law requires that companies with at least 15 employees post pay ranges in their job listings, as well as requiring that current employees have access to the pay range for their current position. The penalty for violating this requirement is between $100 and $10,000 per violation. The first violation only gets a warning as long as the information is added. Some companies also don’t currently have pay bands — the new law requires them. Companies with at least 100 employees will need to provide more detailed information.

Unfortunately, the new law may have to contend with some resistance. In New York City, employers chose to display incredibly wide price ranges. This doesn’t help prospective employees at all to figure out how much they would actually be getting. In one extreme example, Citigroup claimed a range of $0-$2 million, though they later said this was a computer glitch and changed it to something more reasonable. In Colorado, employers created remote job openings — with the stipulation that they could not be in Colorado, so the state requirement didn’t apply to that listing. Colorado’s method probably wouldn’t work in California, since California has such a large population that employers would miss out on a huge segment of potential employees. But New York City’s method is actually already in use in California, even without a requirement to list pay ranges at all. This is because prospective employees tend to disregard a listing entirely if there’s no pay range provided.

The country’s longest-lasting eviction protections are due to end February 1, 2023, at least in Los Angeles, as confirmed by the City Council. The protections have been in place since March 2020, as a response to COVID-19. Despite federal and many local protections ending much earlier, the city’s tenant protections have remained in place the entire time.

The eviction moratorium was certainly financially beneficial for many people who were unable to work during lockdowns, but might otherwise have been expected to continue to pay rent. However, the actual reason for that particular moratorium was fear of the spread of the virus. The economically-motivated tenant protection is currently slated to remain in place until February 2024. This is the prohibition on raising rent for rent-controlled units, of which there are over 650,000 in Los Angeles. Some things are still in a bit of a limbo, though. There are still eviction proceedings going on as tenants are, in fact, still expected to pay at least a portion of their rent, despite the eviction moratorium. Some landlords don’t even want tenants anymore, but can’t find a legal reason to evict them, as their tenants haven’t done anything wrong. The end of the moratorium will erase some confusion. Some City Councilmembers are looking to re-implement some specific protections, but haven’t come to a consensus.

Six new laws affecting real estate are coming next year, and two more in 2024. The six coming next year go into effect January 1, 2023. SB 1495, going into effect January 1, 2024, modifies real estate licensing requirements. AB 2503, with a compliance date of December 31, 2024, requires a revision of the terminology used in real estate contract law to ensure consistency. In addition, SB 1005 and SB 1017 both clarify existing law, SB 1005 regarding probate code and SB 1017 regarding tenant protections against domestic violence.

AB 1410 requires homeowner’s associations (HOAs) to allow members and residents to discuss their common interest development (CID) on social media, as well as allow them to rent out a portion of owner-occupied space. HOAs also may not pursue enforcement for violations during an emergency if it is unsafe to fix it. AB 1837 and AB 2170 both modify existing laws regarding eligible bidders for foreclosed properties, making it easier for tenants, owner occupants, nonprofits, and governmental organizations to win a bid. AB 2559 defines a reusable tenant screening report, which landlords may choose to use, and which they must allow tenants free access to if they choose to use it. AB 2745 requires that experience used for a real estate broker exam be within the prior five years. AB 2960 states that disclosure requirements are set at the date of the contract, even if disclosure requirements change.