For obvious reasons, prospective homebuyers who are expecting to have children, or already have them, might want to move to an area with a highly rated school system. What might not be so obvious is that there are benefits to this even if you aren’t directly impacted by what schools are nearby. Schools affect more than just students; they are a major driving factor in home values.

Neighborhoods with good schools are more desirable, and therefore have higher home values. And because schools don’t typically vanish unless they’re heavily underfunded — which the good schools tend not to be — this is a relatively stable factor in prices. That means homes in these neighborhoods are solid investments, even if you can’t take advantage of the good education.

Conversely, if the school system is not very good, you may think you’re getting a bargain deal with low prices. Unfortunately, your home value probably also isn’t going to go up very much. However, if you are following the trends, you may be able to take advantage of rapidly improving school systems. Maybe prices aren’t high yet, but will be as the schools continue to grow.

Living at the end of a cul-de-sac is frequently met with positive connotations. And indeed, cul-de-sac homes tend to have higher property values. But what is it that makes them more expensive and more desirable? Well, certainly not everyone wants a home on a cul-de-sac. As with any kind of location, there are both distinct advantages and drawbacks.

One of the biggest reasons that cul-de-sac homes tend to have higher property values is actually just that they’re usually on large lots. Much of the value in any property is in the land itself. This in itself can be a benefit, though. Larger lots typically means you’ll have more privacy. Cul-de-sacs also see less traffic, making them safe for children to play outside and for residents to enjoy outdoor activities, as well as quieter. Cul-de-sacs can also be the best of both worlds, in a sense. Despite the larger distance between homes due to larger lots, many people consider cul-de-sacs to foster a sense of community. This is attributed to the circular layout of the street as well as more opportunities for outdoor activities.

Not everyone considers a tight-knit community a good thing, though. If you live on a cul-de-sac, there’s a good chance everyone knows everyone else. Or if you don’t, the rest of them know you as the person who doesn’t interact with them. There’s not a great deal of anonymity. Even if the seclusion is what you’re aiming for, this can also be a negative. Residents may need to navigate through winding streets to reach main roads, potentially leading to longer commute times and increased travel distances. The roads may also be less accessible.

Increasing house prices and relatively stagnant wages have led to the need to rethink our strategies regarding housing. Of course, solving the root issue would be preferable — but if that’s not an option, easing the burden is a useful venture. There have been several recent innovations in methods to approach affordable housing.

A couple of them have been around for a while, but not necessarily targeted at affordable housing. These are government subsidies and grants and developer incentives. If you give people money or tax breaks to build or buy affordable housing, it’s going to become easier. Another that you may have heard of is micro-housing. You may dream of a large home, but the truth of the matter is that smaller houses are not only cheaper, but also more cost effective to build. The only reason they weren’t being built before is lack of demand.

There are also some options you may not be aware of, though. These are community land trusts (CLTs) and shared equity models. CLTs attempt to reduce the cost of homeownership by separating land cost from building cost — normally, a house and the land it’s built on are purchased simultaneously, but with CLTs, the land is owned by a trust and only the structure is sold, so it costs less to buy. A shared equity model allows a buyer to purchase only a portion of the ownership of a home, with the share owned increasing as the buyer accrues equity and uses it to purchase a greater share. This is somewhat similar to a loan, but carries less risk, with the downside being that the buyer doesn’t have exclusive legal ownership of the property.

Tue, Mar 19 @ 7:00PM — 9:00PM PROJECT BARLEY BREWERY 2308 Pacific Coast Hwy Lomita, CA 90717

This is a once a month (every third Tuesday) show that is designed as a listening room for world class songwriters, many with hit songs, long touring/recording associations with music legends etc. to play their original music in an intimate setting.

NO COVER BUT DONATIONS ARE STRONGLY ENCOURAGED AND GO TO THE SONGWRITERS.

Project Barley serves excellent Food (Gourmet Pizza, wings, sandwiches, salads), wine, and award winning beer. Food served till 8:30pm. No reservations so arrive early to get a table. This month we are proud to present: JOEY DELGADO, DEB RYDER, RICHARD STEKOL AND JODI SIEGEL

JODI SIEGEL

Jodi Siegel, originally from Chicago, IL, is a singer, songwriter and guitarist. Over the years Jodi has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and countless others. Her songs have been recorded by Maria Muldaur, Marcia Ball, Tommy Ridgley and Teresa James.

JOEY DELGADO

Singer, guitarist, producer, songwriter, Joey Delgado has been a member of one of the best and most popular East Los Angeles based blues/rock, Americana, Latin soul bands for 50 years, The Delgado Brothers! Out of the 5 Delgado Brothers studio albums, Joey Delgado has produced all but one; and all the over 50 original songs were composed by Joey D and his band of brothers.

DEB RYDER

Born in Chicago Illinois, she began singing at the age of five joining her Dad, crooner Al Swanson on stage at several popular venues and churches in the area. Debs musical career began in her early teens when her mother moved the family to California and along with her stepfather opened the renowned Rock and Blues club the Topanga Corral. There, she opened for and performed with such legends as Etta James, Big Joe Turner, Taj Mahal and Canned Heat, all regulars at the club. These artists mentored Ryder, and it was then that her vision of herself as a singer, songwriter and performer began to take shape.

RICHARD STEKOL

Richard is a triple threat. He plays guitar like nobody else, any style, he sings soulfully and with purpose and he writes incredibly original songs that either break your heart or knock you over the head with their truth. He’s a songwriter like no other and those that know of his work are forever changed. While some know Richard as one of the founding members of Southern California’s Honk Band (they had three records released on a major label and toured extensively opening for people like The Beach Boys, Kenny Loggins and Michael McDonald), he was also a member of the super group The Funky Kings (featuring Jack Tempchin, Jules Shear, Richard Stekol, Greg Leisz). He released many solo records over the years and has had songs covered by Michael McDonald, the late great Mike Finnigan, Ian Mathews, Michael Nesmith, Kenny Loggins, Julie Christensen, Rick Nelson, Amy Holland and more. He is also a producer of many independent recordings and has played guitar as a session player. He is a true original in a sea of copycats.

A Staged Reading of The People with The Trees in Their Chest by Shawn Christopher Lovell Nabors. Produced by Grand Vision Foundation.

Nabor’s new and original play follows an African American family from Brooklyn, NY as they struggle to break the curse of poor health that has marked their family for generations.

The audience will be invited to give constructive feedback after the performance.

Kimberly Ford

Kimberly Ford

DREAMLAND with Kimberly Ford The Music of Joni Mitchell Saturday, March 23 / 8 PM (?Wine Tasting 7 PM)

An homage to one of the most iconic Woodstock musicians. Hear Help Me, Both Sides Now, River, and more.

Jack of Hearts w/ Scarlet Rivera The Music of Bob Dylan

Fri, Apr 05, 2024 8:00 PM Doors 7:00 PM

For over five decades, Bob Dylan has remained one of the most important figures in American music. The Jack of Hearts Band seeks to authentically replicate the sound of Dylan – from the early ‘60s folk scene to the Blonde on Blonde album, the Woodstock retreat to masterpieces such as Blood on the Tracks and beyond.

Returning to the Annex with violinist, Scarlet Rivera, best known for working with Bob Dylan on his 1976 album Desire and as part of the Rolling Thunder Revue.

In a normal year, the interest rate for a conventional mortgage loan would be lower than the rate quoted for a “high balance” loan, which would be slightly lower than a “jumbo” mortgage. (Here in Los Angeles jumbo is more common than not.) The theory behind the differing rates is one of risk management. Lenders generally consider larger loans to be more risky, thus jumbo costs more.

Guess what! It’s not a normal year. It’s a Presidential Election Year. In addition to the political strife, our nation is closely involved in a couple of economy-disrupting wars in other parts of the globe.

The end result is jumbo loans with fixed interest rates that are as low or lower than conventional loans. Despite headlines touting strength in the economy, interest rates have increased by approximately .5% since the first of the year. The most recent announcements from the Federal Reserve System are hinting that anticipated rate reductions aren’t happening at all in the first half of 2024, and the number of potential reductions is expected to be less than previously expected.

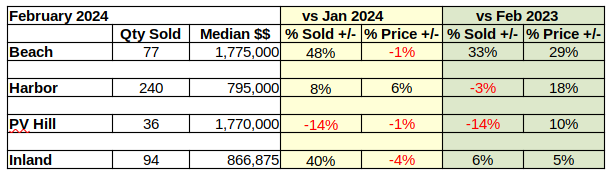

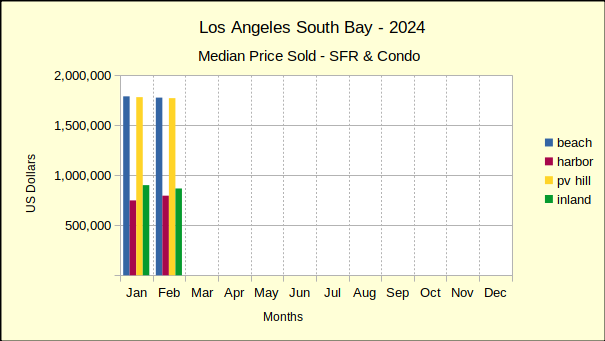

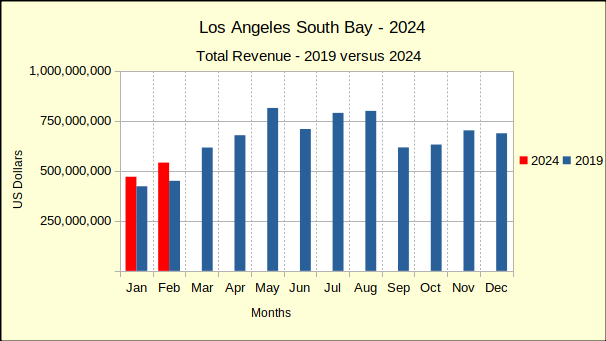

Last year saw median prices in the South Bay falling below 2022 prices through July. In August of last year price declines began to abate. By December of 2023 prices had started to stabilize. The new year continued that trend with only one negative median price result in January. Improving on that, February showed solid growth in prices across the South Bay. The real estate market seems to be reacting to what is touted as an improving economy.

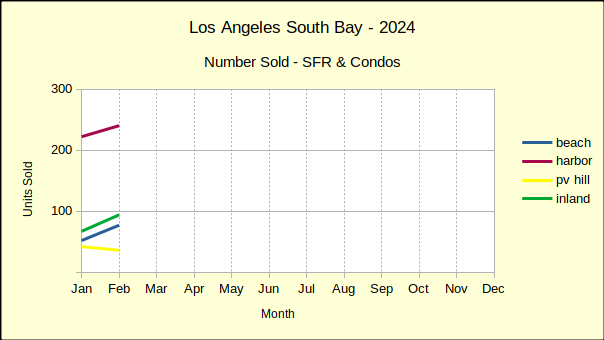

However, compared to last February, sales volume this February was a mixed bag with overall positive growth of 2% despite declines of 3% in the Harbor area and 14% on the Hill. These weaker sales figures follow a strong growth in the number of homes sold in January versus the same month in 2023.

Recent month to month history has shown that a decline in sales volume is typically followed by a decline in median price. This “tit for tat” resonance indicates a market where buyers are at the edge of their ability to buy and sellers are feeling the resistance. Indeed, following the upward movement of mortgage interest rate activity for the first two months of the year leads to the conclusion sales volume will drop, followed by more substantial price decreases in coming months.

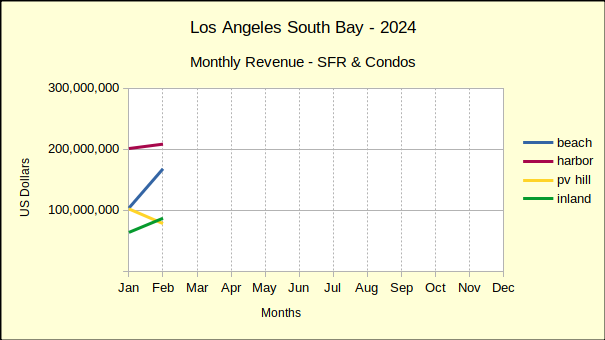

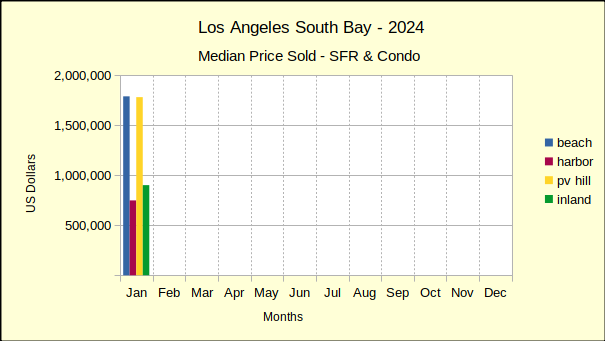

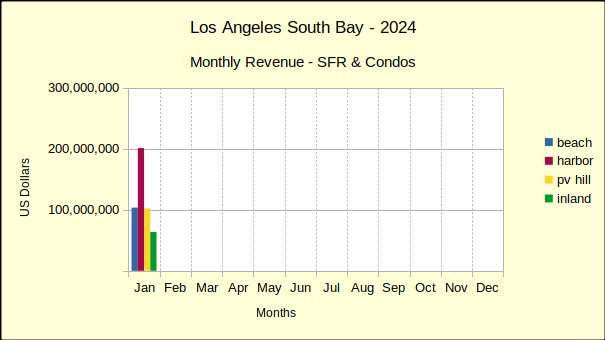

Beach: Sales and Prices SeeSaw

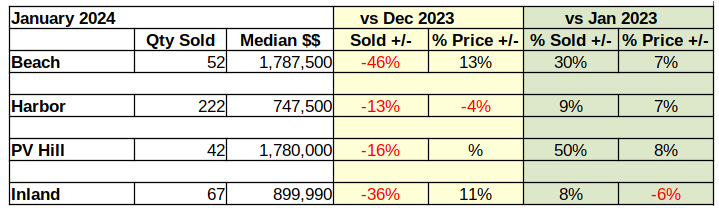

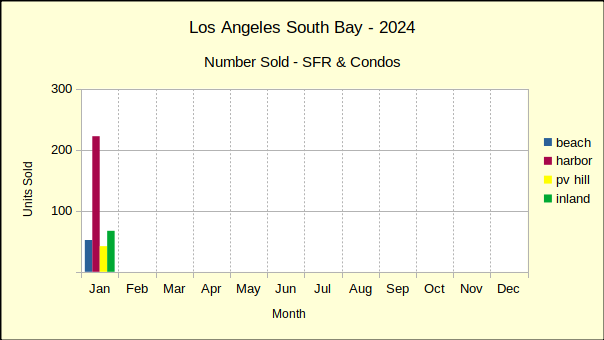

On a month to month basis, the Beach area has seen serious ups and downs in the number of homes sold and in the median sales price. January started with a massive 46% drop in sales from December, then February showed up with a 48% increase in sales volume. By way of contrast, Palos Verdes sales were down 16% and down 14% for the same months. The median price for Beach homes slipped 1% in February versus a 13% increase in January.

February sales volume versus February of 2023 was also steeply higher at 33%, the largest increase of the South Bay areas. At $1.175M the median price was up 29% over the same month last year. This is a somewhat surprising median price increase in light of other annual increases around the South Bay falling in the range of 5-18%.

Looking at year to date for the first two months of 2024, the Beach area had positive sales volume of 32% with a median price increase of 17%.

Harbor: More Up and Down

Responding to the volatility of the economy, the Harbor area flipped from negative numbers in January to positive in February. The number of homes sold was up by 8% over the prior month, while the median price of those homes increased 6%. The largest of the South Bay areas, the Harbor area typically has less variability in both sales and prices than the other areas.

Annual figures, looking at change from one year to the next in the same month, is usually a predictor of long term direction. February home sales in the Harbor area seem to be close to the bottom of market. Volume dropped by 3% from 2023, the smallest annual decline since the end of the pandemic.

At the same time, the median price rose 18% above that of February 2023. It should be noted that the median price in the Harbor last February was exceptionally low at $675K. In contrast, the $795K for this year appears to be on the high side and should be expected to moderate as the year goes on.

Year to date, the number of homes sold has increased by 2% over 2023. The median price has gone up 12%.

Hill: Numbers Continue to Fall

Real estate on the Palos Verdes Peninsula was off more this month than last. Month to month sales volume dropped by 14%. Median price, which was flat last month, has fallen by 1% this month. This kind of back and forth jockeying in price and volume looks jerky in the month to month statistics.

When viewed against the backdrop of annual data one can more readily see the direction. Annually, residential sales dropped by 14%, roughly the average of the past few months. While sales volume was dropping, the annual median price rose a surprising 10%.

Combining January and February for year over year numbers shows the number of homes sold increasing by 11% and the median price increasing by 9%

Inland: A Mixed Bag for Sales and Prices

Like the Beach cities, the Inland area enjoyed a huge surge in the number of homes sold for February, after suffering a large drop in sales January. Volume was up by 40% for the month. Median price dropped 4% after an 11% jump last month. So far this year the market has been very unpredictable.

As mentioned early, the “same month, last year” perspective is starting to level out. Residential sales volume for February of 2024 increased by 6% compared to 2023. The median price was up 5% over for the same period. The annual percentage of change seems almost stable by comparison the the monthly.

Year to date, Inland sales have increased 7% while the median price has declined by 1%. So far in 2024, only the Inland median price has declined from the first two months of last year.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

Before purchasing a new home, there are some important details that will help you make your decision. You’ll want to know what you’re paying for, as well as how to get the best deal. Asking the right questions will make the process much smoother for you.

First, make sure you know exactly what it is you’re buying. Is any personal property included in the sale? Is any fixture excluded? A purchase offer should address personal property and any exclusions. Also, if there are any disclosed concerns with the property, you’ll want to know what they are. It may not be worth your while if there are any major concerns. You’ll also want to know what you can expect to be paying in utility costs. After all, utilities are a component of homeownership costs.

If you want the best deal you can get, you should definitely ask your agent for a comparative sales report. This is a report which details recent sales histories of similar properties. Depending on the area, it may be unlikely to find an exact match, but this will give you a rough estimate of the expected price range for a property that you’re considering. This is particularly important if you’re concerned that the property may be overpriced or have some sort of defect. To aid in this, you can also ask how long the property has been on the market. If it has been sitting around longer than average, there could be an issue. Another question you may want to ask is if the sellers have already bought another home. This could give you some insight into the motivations of the sellers, which may help you negotiate.

You may have received a loan payment notice from a company you don’t recognize or you know you haven’t taken a loan from. That doesn’t necessarily mean it’s a scam, but it could be. Loan servicing is a real thing, whereby lenders outsource their payment collection to a loan servicing company. In addition, lenders can and do sell their loans to other companies, or companies could merge or get bought out. These are all legitimate reasons you could get a notice from an unfamiliar company.

Unfortunately, scammers are aware of all these methods, and attempt to convince you that what’s happening is legitimate. So, if you notice any deviation, you should always check to make sure it’s real. If the lender’s policy changes or the company is sold, you should receive a letter notifying you of this before any new collections occur. Beware that this process could be disrupted by improper transfer of records or collection dates coinciding closely with the change. Make sure to communicate directly with your lender, not the company that is collecting, until you are sure that it’s legitimate.

The heat of California, particularly in the summer, means many Californians turn up the air conditioner to stay cool. But there are some areas of the world that can get just as hot, if not hotter, and do without cooling systems. How do they manage it? In Burkina Faso, which frequently reaches temperatures over 100 F, it’s the type of stone used for construction.

Burkina Faso is rather low on the Human Development Index (HDI), ranking 184th out of 191 countries as of 2020. This means much of the country doesn’t have access to electricity, and importing concrete is expensive. What they do have easy access to is a stone called laterite, which forms naturally in the region. Laterite is quite strong once formed into blocks, and its thermal properties help keep the interior cool. Constructing buildings using laterite is not a new concept, but in much of the world it has been replaced by concrete.

Unfortunately, laterite is not a solution for California. With its advantages come some pretty severe disadvantages. Laterite has extremely low earthquake resistance. In California, which has over a hundred earthquakes per day and building laws requiring high earthquake resistance, laterite buildings simply won’t work.

Whether your home has a lot of outdoor space or just a little, it’s possible to make good use of it. But in order to optimize your space, first you need to know how you want to use it. Not everyone wants to use their outdoor space for the same functions, and you want to have some idea of what function or functions it should serve for you.

If the space is large enough, divide it into zones. For example, you might have one area for relaxing with a book, one for a garden, and one for socializing with guests. Various types of lighting can help to transform each zone individually or your entire space. Perhaps you want soft ambient lighting, or maybe you want more functional lighting for reading or dining. Regardless of what you use your space for, a couple things are to be expected in any outdoor space, and those are seating areas and greenery. Choose weather-resistant materials such as wicker, teak, or metal and add cushions for improved comfort. Opt for plants that require minimal upkeep and grow well in your area.

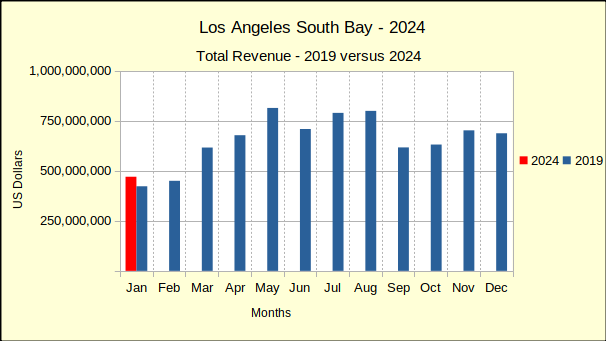

Across the Los Angeles South Bay the number of homes sold in January was down compared to December—way down. For the same time period median prices are mixed with most sales either flat or down.

Looking at sales volume in January versus January of last year, shows big increases in activity. However, that serves more to show how slow the real estate market was at the beginning of 2023, than how good it is today. Median prices were likewise up for most areas when compared to the same month last year.

From a historical perspective, looking back at 2019, still the most recent “normal” business year for real estate, we see sales volume overall remains 21% below that benchmark. Median prices, which shot up during the pandemic have stubbornly stayed up. As of January, median prices range from 25-30% above the 2% inflation factor the Federal Reserve targets.

The combination of inflated prices and mortgage interest rates testing the 7% level has created a stagnant market place. Typically a presidential election year would bring rosy news about a growing economy and low interest rates. At this point there’s only one month of data, not enough to make any forecasts, but 2024 is off to a slow start.

Beach: Sales Off 46%

Month to month sales volume in the Beach cities collapsed by 46% in January. After back to back increases in the number of homes sold for November and December, the huge drop was unexpected. Juxtaposed against the 13% increase in median price, it demonstrates the current market dynamic.

The only actual buyers are people who have no choice but to move, despite the low inventory and high interest rates. At the same time, most sellers are stalling because they don’t want to be sitting on the market for weeks. And, because most sellers are also buyers, they’re waiting for a better market with more homes available and lower interest rates for their replacement purchase. As a result, the number of available homes listed on the MLS is further depressed.

This has brought about a rare phenomenon, the “off-market” sale. Both buyers and sellers are actively looking for deals that can be consummated without the competitive environment of the Multiple Listing Service (MLS). Buyers love the fact there are no bidding wars. Sellers are glad to sell at asking price without endless open houses and dozens of showings. The properties usually end up on the MLS as history, but not as competition. How long this trend will last depends on the economy over the next few months.

The market at the Beach has clearly improved since last year. Sales from January of 2024 have climbed 30% compared to January of 2023. At the same time, median price has moved up 7%. Of course, as mentioned earlier, last January was far from a good market in real estate.

Given the turmoil of recent years, one is compelled to look back at 2019, before the pandemic with it’s rock-bottom interest rates and sky-rocketing prices. Using that metric, January sales this year fell 34% below January of 2019. Median price this January was 43% higher than it was in January of 2019. Clearly “normal” is still a long way off.

Harbor: Sales Off 13%

Month to month statistics from the Harbor area demonstrate a truism. Pointing the way toward stability in the market, many of January’s home sales came with a reduced price. The median price dropped 4%, rather than increasing as it did in the Beach cities. Those price reductions appealed to buyers and the number of transactions increased considerably. Correspondingly, the sales volume only dropped 13% as opposed to a 46% drop at the Beach.

Harbor area sales for January 2024 ended with 9% more transactions than the same month lin 2023 in an unsurprising response to the market collapse of last winter. Also on the positive side, median prices for Harbor area homes increased by 7%.

Pre-pandemic residential sales for January 2024 was mixed in comparison to January of 2019. Sales volume was off, with 16% fewer homes sold in 2024. At the same time, median prices were up 44%.

Hill: Sales Off 16%

November and December of last year looked like a bad thing was turning good, and then January 2024 came along. Home sales on the Hill suffered less than at the Beach or Inland, but a 16% drop in sales volume in an already moribund market hurt. Median prices on the Hill hit that “sweet spot” with no change up or down.

Compared to January of 2023 the number of home sales on the Hill went stratospheric climbing 50% for the month. Of course, having read this far you know last winter was a low spot in the market. Combine that with the comparatively small number of sales on the Palos Verdes Peninsula and it’s easy to have outsize percentages. While sales volume was up 50%, median prices climbed a more modest 8%.

January 2024 versus January 2019 in home sales on the Hill showed an solid improvement. The number of homes sold increased by 27%, in contrast to falling sales in the Harbor and Beach areas. With the number of home sales up, a 37% increase in the median price is a welcome addition.

Inland: Sales Off 36%

Home sales in the Inland area closely followed those at the Beach in January. Similarly, the month ended with a calamitous 36% drop in the number of homes sold—down to 67 homes from over 100 in both November and December. Likewise, the median price came in with an 11% increase, slightly less than at the Beach. This shows the effect of “sticky prices” where a lot of sales don’t happen because the sellers are resistant to lower offers and buyers are balking at higher prices.

On a year over year basis, January 2024 showed 8% growth in the number of sales compared to last January. Median prices continued following the long downward slide of 2023 and dropped another 6%.

Comparing the Inland sales to 2019, the most recent stable year, the number of homes sold has dropped by 39% leaving a lot of room for recovery. The median price has climbed 40% over that five years, roughly 27% greater than the “ideal inflation” sought by the Federal Reserve.

Beach=Manhattan Beach, Hermosa Beach, Redondo Beach, El Segundo

Harbor=Carson, Long Beach, San Pedro, Wilmington, Harbor City

PV Hill=Palos Verdes Estates, Rancho Palos Verdes, Rolling Hills, Rolling Hills Estates

Ocean view corner end unit flooded with natural light in highly sought-after Palos Verdes Bay Club. Enjoy sunrise and sunset views from two private, tiled decks and floor to ceiling windows in living area as well as bedrooms. Although this unit is on the first level, the building itself is significantly elevated and the corner location affords open and expansive views. This unit has the Delaware B Floor Plan (See Listing Supplement). The Delaware plans are the only units in the complex with 2 view balconies as they are always end corner units facing the ocean. Double front doors lead to a foyer and great room with living and dining areas. Remodeled kitchen and baths with high quality features. Floors are waterproof wood-look vinyl, travertine, and tile. Washer/dryer hookups inside unit (washer/dryer not included) and community laundry just down the hall. Other upgrades include electronic custom-made blinds for floor to ceiling windows in living room and custom walk-in closet (instead of wardrobe closet in original floor plan) in primary bedroom. The unit comes with two subterranean parking spaces and two storage units. Recent improvements for this building include new roof and updated hallways with new carpet, wallpaper, and paint. Palos Verdes Bay Club offers two oceanside pools and spas, two tennis courts, other sport courts, a social hall, a fitness/game room, beautiful grounds, and walking trails to the ocean and nearby Terranea.

For additional photos see https://moeryphotography.com/clients/AClark/32735SeagateDr107

Friday, March 15, 2024 8:00 PM $25-$40 a person, wine tasting $16 or free for members

From the moment Grammy-nominated Caro Pierotto strikes her first note, her captivating warm voice energizes the room. Accompanied by her all-star band, you’ll hear covers and originals in Portuguese, Spanish, and English featuring elements of samba, reggae and soulful pop.

“The expressiveness and technical mastery in Caro Pierotto’s voice underscores Brazil’s tradition of great female singers – from Sylvia Telles to Gal Costa.”- Ernesto Lechner/Latin Alternative for NPR

Pierotto’s music has found audiences all over the globe. Her 2023 album, ‘Sambalismo’, has been cited as one of the Brazilian Music Albums of the year.

Captain John and the band deliver vintage sea shanties and nautical tunes with Celtic-punk and pirate-rock swagger.

Kraus leads this merry crew of powerhouse musicians after years spent as a sea captain and growing up in a musical household. His pioneering band perfectly combines his love for music, the sea, and the legacy of seafaring storytelling. And, just so we’re all clear, John Kraus really is a captain – on LA Maritime Institute’s stunning Tall Ships! The Goers are: Tim Weed on violin, David Dutton on the drums and jazz legend Bob Aul on fiddle and tuba. Paul Givant of Rose’s Pawn Shop shows up frequently to play guitar and banjo.

Roots & Rambles is a concert workshop series featuring musicians dedicated to the preservation, artistry, and evolution of folk and traditional music in the United States. One hour before the concert. Please RSVP if you plan on participating. Concert tickets are required to participate.

Roots & Rambles is made possible by a grant from the National Endowment for the Arts.

TUESDAYS @ 5:30PM — 7:30PM The Lighthouse Cafe, 30 Pier Avenue Hermosa Beach, CA 90254 310 376-983

Andy & Renee-Banana Leaf

THU, FEB 22 & 29 @ 6:30PM — 9:00PM Banana Leaf & Beach Cities Social, 1408 S Pacific Coast Hwy, Redondo Beach, CA 90277

DYLANFEST 34

Saturday, May 25th! Tickets on sale soon! Torrance Cultural Arts Center

One of the largest Bob Dylan festivals in the world is being held for the 34 year. Organized by Andy Hill and Renee Safier, this all day event exclusively presents music created by Dylan and performed by 50-60 artists, some international and all well known here in LA.

Andy & Renee & Hard Rain at Wilson Park

SAT, JUN 29 @ TIME TBA Wilson Park, 2200 Crenshaw Blvd., Torrance, CA 90501

Andy & Renee & Hard Rain-Songs From Laurel Canyon

SUN, JUN 30 @ 8:00PM The Grand Annex, 434 W. 6th St., San Pedro, CA 90731

SoCal favorites play originals and Songs from Laurel Canyon. Hear classic rock hits of the late ’60s and ’70s from Buffalo Springfield, Carole King, James Taylor, Linda Ronstadt, CSNY, plus a set of the band’s award-winning original songs culled from their 17 CDs. Get tickets at https://grandvision.org/event/andy-renee-hard-rain-songs-from-laurel-canyon/

This is a once a month (every third Tuesday) show that is designed as a listening room for world class songwriters, many with hit songs, long touring/recording associations with music legends ETC… to play their original music in an intimate setting. NO COVER BUT DONATIONS ARE STRONGLY ENCOURED AND GO TO THE SONGWRITERS. Project Barley serves excellent Food (Gourmet Pizza, wings, sandwiches, salads), wine, and award winning beer. Food served till 8:30pm. No reservations so arrive early to get a table. This month we are proud to present: TED RUSSELL KAMP, BLISS BOWEN, JASON FEDDY AND JODI SIEGEL

TED RUSSELL KAMP is an LA-based singer/songwriter, producer and Grammy winning bass player. He just released a new record called California Son that is already riding up the charts and receiving excellent reviews!

Ted writes, records and travels the world performing his own country / roots / Americana music from his eleven critically-acclaimed albums. Ted also plays live, records sessions, and collaborates on songs with A-list songwriters and musicians in L.A., Nashville, Austin and around the world. Ted often works out of his home studio — The Den — and has produced several well-received albums for fellow artists there. Ted has also had the honor of being a friend, collaborator and member of Shooter Jennings’ band for most of the last 15 years. Ted also played on the 2020 Grammy winning Country Album of the Year, Tanya Tucker’s While I’m Living.

BLISS BOWEN

Bliss Bowen is a singer-songwriter and writer who spent most of her childhood inhaling the salt air of the Atlantic Ocean and the folklore of the Pine Barrens of South Jersey (aka Springsteen country). She then rooted herself in the foothills of Sierra Madre in Southern California, where she finds abundant inspiration for her soulful Americana songs and stories. Bliss is currently preparing for the late spring release of her album Ghost Trees, which she has been recording with a crew of exceptional musician pals from L.A.’s Americana-roots community. Whether performing as Bliss Bowen & Friends with her rocking band or in duo and trio configurations for more intimate performances, she connects with audiences honestly via her powerful, heartfelt singing and storytelling and evocative roots music. reverbnation.com/blissbowen, blissbowen.bandcamp.com, open.spotify.com/artist/3q3x9BbcTh50q4v6tb6Ozh

JASON FEDDY

Jason is Laguna Beach CA Arts Alliance “Artist of The Year” 2019/20. He has worked as a singer/songwriter and guitarist ever since his school days, pausing only for 5 years as a morning jock on KX93.5, Laguna Beach, Ca’s local radio station. He is a central figure in the music scene of Laguna Beach, curating and producing the city’s numerous outdoor music series. His album of songs from the plays of Shakespeare and the show, “Shakespeare’s Fool” are critically acclaimed.

JODI SIEGEL

Jodi Siegel, originally from Chicago, IL, is a singer, songwriter and guitarist. Over the years Jodi has opened for and or shared the stage with many respected musicians including: Albert King, Robben Ford, Robert Cray, J.D. Souther, David Lindley, Fred Tacket and Paul Barrere (Little Feat) and countless others. Her songs have been recorded by Maria Muldaur, Marcia Ball, Tommy Ridgley and Teresa James.

There’s a strong tendency to want to pay off your mortgage as quickly as possible. There’s also a strong reason for lenders to not want you to do that — they get less money because you aren’t paying as much in interest. Because of this, they frequently use prepayment penalties. This is an extra fee for paying off your mortgage too quickly or before the term of the loan ends. If you’re simply paying the minimum amount anyway, this won’t affect you, but if you think you may want to pay off your loan early, you’ll want to know your options.

Different states have different laws regarding prepayment penalties, and some don’t allow them at all. In states where they are allowed, they come in two types: hard prepayment penalties, which are fixed fees regardless of the reason for prepayment and that are usually a percentage of the loan amount, and soft prepayment penalties, which are only charged if the borrower pays a large amount in a short time period. Even in states that allow prepayment penalties, not all loans will have them, and you may be able to negotiate with your lender for their removal. When shopping for loans, make sure to read all the terms of the agreement, and talk to a legal professional if there’s anything you don’t understand or want to learn how to negotiate.

If you’re planning to sell your home, or just want to be informed about current trends, you may want to know about present day homebuyers’ preferences. The problem is that looking at general trends only tells you about the largest cohorts of homebuyers, which are Millennials and Baby Boomers. Not only do these two groups have vastly different preferences between each other, it also ignores Gen X and the admittedly small group of Gen Z homebuyers.

Knowing the demographic makeup of your region can help you to understand what the people in your area are looking for. Alternatively, knowing what other cohorts desire can help tailor your choices to attract people to your home. There are certain things you cannot change, such as the walkability or access to public transportation in your neighborhood and presence of nearby parks or schools. However, if you know which types of people are looking for the sort of things that exist where you are, you can base your decisions about things you can change based on that group’s preferences.

Currently, Baby Boomers are not in the business of buying large, fancy homes. They’re looking to downsize, or remodel a home to suit their personal needs. They also generally want a healthcare facility nearby, since their age can lead to medical complications. Gen X is looking for a mix of business, family care, and leisure. Many Gen X people are working and also spend time caring for their aging parents, which leads them to want either nearby parks or recreational facilities to improve their work-life balance, or a suburban or rural lifestyle if they work from home. Millennials are the largest cohort of potential homebuyers, but they also can’t currently afford expensive homes. Rising housing costs mean Millennials are currently transitioning from renting to their starter homes, since many of them have had their initial homeownership plans delayed. As for what they’re looking for, they’re big on technology and sustainability, and prefer easy access to employment hubs via either walkability or public transportation. The group of Gen Z homebuyers that are actually able to afford a home have probably not been much affected by delays, so their digital native and eco-friendly identity is even more pronounced than in Millennials. They prioritize energy efficient homes, smart technology, and cultural diversity.

Solar energy has been growing in popularity in recent years, and there are good reasons for that. Solar energy is highly sustainable, and isn’t subject to fluctuations in the market since the amount of available solar energy is not market-dependent. Some people aren’t convinced though, and that may be the result of some misconceptions.

A big reason people don’t even entertain the idea of solar energy is that they think it’s too expensive. While initial installation can be pricy, the savings over time allows the investment to pay off relatively quickly. This is especially true because utility prices are increasing, and solar panels don’t require utility payments, so your electricity bills may be cut out entirely. There are also government incentives in place that will allow you to offset the initial investment cost. Solar panels do have some maintenance costs, but they’re pretty minimal — just some regular cleaning is generally sufficient.

Others believe solar panels are only effective in warm, sunny weather. A more appropriate statement would be that direct sunlight enhances their efficiency. They still work perfectly fine in cloudy or rainy weather. Also, they actually work better in colder temperatures, not worse. This is because their efficiency is determined by a difference in energy between the photon particles in sunlight and electron particles in the panel — which have lower energy at colder temperatures — not the total amount of energy received. This means a hot, sunny day may result in the same efficiency as a cold, overcast day.

You might think lenders would need to do a bunch of fancy calculations to determine how much money you can borrow. There are certainly several factors that go into the final calculation, but if you want a rough estimate, it’s actually relatively simple. Lenders tend to use one of two formulas, either mortgage payment as a percentage of gross monthly income, or debt to income ratio.

Both of these factors involve your gross monthly income — that is, the amount you were paid before deductions from social security and taxes and before making any payments or contributing to savings. Where they differ is what your gross monthly income is compared against. The first method calculates what your monthly mortgage payment would be based on actual interest rate and ensures that it doesn’t exceed 28% of your gross monthly income. The debt to income ratio method compares your gross monthly income against your debts, such as credit card debt and other loans. These existing debts plus your new loan payments should not exceed 36% of your gross monthly income. Both these methods do require knowing the interest rate, which is determined by several factors, but if you know about where interest rates are, you can make an educated guess.