California is proposing a plan to start the “California Dream Fund,” which is intended to allow the state to subsidize purchases by first-time homebuyers without any tax increases. They hope to achieve this by allowing investors to use their money to subsidize the purchase, in exchange for an equivalent share of ownership. This will be limited to 45% to prevent the investors from owning a majority share.

The plan is still in the works, but there are already a few criticisms. Currently, there is no indication of who is liable if the property goes into default. Is it only the buyer? Do the investors have a stake, since they have an ownership share? Is the state liable since they’re the ones providing the subsidy program? Perhaps these questions will be answered later, but if the answer is simply as existing law, the program is no different from a state matchmaking program between investors and prospective homebuyers. Furthermore, subsidizing home purchases does nothing to address the real problem — the fact that home prices are so exorbitantly high in the first place that the plan is being discussed to begin with. Subsidies will increase demand, but demand is already high; it’s the low supply that needs to be addressed.

A 2016 state law requiring organic waste to be processed separately from inorganic waste goes into effect at the start of 2022. However, even with the six year forewarning, cities still aren’t necessarily equipped to handle the change. Some cities, such as Carson, have processing plants allowing them to convert food waste into methane for use as renewable fuel, with fertilizer as a byproduct. But food waste isn’t the only type of organic waste, and the Carson facility can’t process other kinds.

Processing infrastructure isn’t the only issue, either. The cities’ sanitation departments will also need to change the way they collect. That’s easier said than done. The new law didn’t provide any additional funding, and Long Beach can really only afford to provide one additional bin to each household, so they’ll need to put all of their organic waste in the same bin. That means it’s going to need to be either resorted later, or processed at a facility that can process all types of organic waste. Some of the costs are probably going to come in the form of increases to collection bills for residents.

Rent control exists in many cities in California, and was designed to keep rent prices low so that more tenants can afford to rent there. And it does keep prices low — as long as no one is looking to rent there. The problem is that rent control is only in effect during the tenant’s residency; as soon as the tenant leaves, the landlord can increase the price to reflect current market values. This means that even if a new prospective renter is looking in a rent controlled neighborhood, they’re still looking at current market rates.

There’s also another reason it doesn’t help renters much, and may actually harm them. And it’s merely the fact that landlords are aware of the above aspect of rent control and readily use it to their advantage. While rent control laws often do also include some form of eviction protection, they don’t outright prevent evictions, and in many cases renters aren’t able to afford to sue their landlords if they were wrongly evicted. This means that in many cases landlords can simply choose to evict their current tenant if they want to increase the rent price, or if they can’t find believable cause to evict, just stop maintaining the property until the tenant doesn’t find the situation livable anymore. Without rent control, prices steadily go up, but landlords don’t resort as frequently to devious methods to raise the price.

California was once a dream destination in the US, and probably still is for some people unable to afford it. But as for the people already living here, they’re leaving at a higher rate than people are coming in. What’s happening? Is California simply not living up to its expectations? What about the state do people not like?

There’s a theory that it’s California’s high tax rates that are pushing people out to nearby states such as Texas, Washington, and Arizona. But this is a misconception — it’s not that people don’t want to live in California, it’s that they can’t. The median home price in California has increased by 300% since the 1970s, even adjusting for inflation. Meanwhile, incomes have increased only 33% in the same time period. People who have been living here happily for years or even decades can no longer afford to do so, and are moving to less expensive states. California desperately needs more affordable housing or a wage overhaul if it wants to reverse its negative domestic migration numbers.

The eviction moratorium for federally backed mortgages was set to expire at the end of last month, but on June 24th, it was extended through July 31st. California has even gone above and beyond the CDC recommendations, extending the state residential moratorium through September 30th. With a third of renters in California feeling they were likely be evicted in July or August, and an additional 6% being quite sure of it, something needed to be done. 10% of California renters are still behind on their payments, and over a fifth of them had little to no confidence in their ability to make their July payment.

When people retire, there’s a temptation for them to want to pay off their mortgage as soon as possible. After all, it’s a repeating cost that people simply don’t want to have to deal with. However, that’s not necessarily the best financial choice. Depending where the money is coming from, it may actually be less expensive to keep making payments. That said, there’s definitely something to be said for reducing the stress that comes with overhead payments, even if you sacrifice some income.

Sometimes the decision is relatively simple. If you have excess money lying around not being invested, such as in a checking account, you probably want to pay off your mortgage. This is because checking accounts typically don’t earn much interest if any at all, so the interest rate on a mortgage is guaranteed to be higher — the longer you wait, the more you lose. This also applies to any other funds that are being invested at a lower interest rate than the mortgage. Of course, this assumes you don’t need large sums of cash in the near future for some other reason.

Checking account withdrawals also aren’t taxable, unlike funds from certain retirement accounts. The interest rate comparison may not work out for retirement accounts. Even if it does work out, the withdrawal tax may make it less economically viable, especially if it pushes you into a higher tax bracket.

If you’re looking to take advantage of interest rates while they are still low, you have two options. You can either buy a new house, or refinance to get a lower rate. Both options can have pros and cons, and which will benefit you more will depend on a few factors.

Refinancing can be a good option under either of two conditions. The first is high equity. If you have a lot of equity in your home, refinancing allows you to access it for a temporary boost in available funds. The second is shortening the length of a loan. If you can get a shorter term loan at a lower interest rate than you currently have, that’s usually an incredible deal. Of course, whether you’re actually saving money or not in the long term depends how much you’ve already put into your current loan.

Moving is a good option if you have something in mind for the type of home you want. Low interest rates enable you to purchase a more expensive home without necessarily increasing your mortgage payment by much, if at all, and it could even be lower. This is especially the case if you are actually looking to downsize — your mortgage payment would almost certainly drop. If you were already planning to buy, it’s still a good time, even with mortgage rates starting to climb back up.

Recent economic hardships are causing some people to downsize, especially if they’re also moving into urban areas, where living space is at a premium. Most of the time, people who are moving out simply put all their furniture and belongings in a moving van, and figure out where to put it later. People living in a house that’s appropriately sized for them generally don’t use the entirety of their home’s space, but that doesn’t necessarily mean they’ll have enough space to bring everything when downsizing.

Some of your furniture may have to go. If your new condo or apartment doesn’t have a dedicated living room, you probably don’t need both your couches. Going down one bedroom because your kid has moved out? Get rid of the extra bed. You don’t need to just leave them there, though — you can donate them, give them to a friend, sell them, or even just hold them in a storage unit.

Speaking of storage, a smaller home absolutely is not going to have as much storage space. You need room for items such as towels, bedsheets, clothing, and dishes. In your old home, these may have all gone in your closet and dresser. But maybe your new closet is smaller, and perhaps your old dresser doesn’t actually fit in the new space. Think about investing in compact storage containers and utilizing space efficiently, such as by storing containers under your bed.

One of the ways lenders try to make sure mortgage applicants are good on their loans is by looking for a down payment. A down payment tells lenders that the applicant does currently have money, and is therefore probably capable of saving some portion of their income. But that starts to fall apart when the money isn’t theirs — if the down payment was gifted to the buyer, generally by their parents, the buyer doesn’t necessarily have any skin in the game. They may be more likely to default on their loan.

Homeownership is a struggle, especially in California where home prices are exorbitantly high. In many cases, first time homebuyers actually do need a little bit of help to get started. The Consumer Protection Finance Bureau (CPFB) has data available for the years 2009 to 2016, which states that 31% of homebuyers aged 25-44 received a down payment gift. Unfortunately, not all homebuyers are able to get one. Black households in particular are often lower income, and the parents don’t have excess savings to give to their children. Given how frequent gifting is, this is a considerable blow to Black homeownership. While down payment gifts may seem like a necessary evil to overcome low homeownership rates, in the end they primarily boost white homeownership, exacerbating racial inequality, and are also only temporary boosts, since they result in more foreclosures.

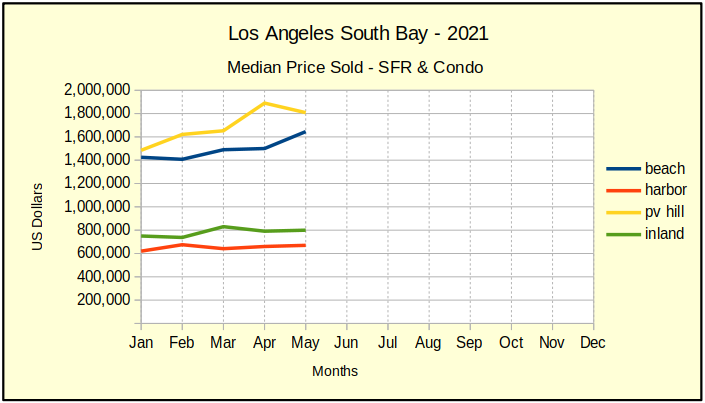

It’s official. We’re now in the post-pandemic phase. So what’s the real scoop on local real estate? Follow along as we review the May statistics and tease you with a little early June data.

Putting Statistics in Perspective

The first thing we want to do is remind everyone that in the first three months of the pandemic, the number of sales in the Los Angeles South Bay had dropped to approximately 50% of 2019 activity. So, when we say sales are up 100% from last year, what we’re really saying is that sales volume is pretty much back to normal. That is, “normal” in 2019.

Similarly, the fact all areas show higher sales prices than 2020 is relatively meaningless. We can only look to recent months or pre-pandemic statistics for market indications. We’ll get into more detail below, but remember that comparisons of 2020 to the Great Recession can be misleading.

Median Price Climbs: Everywhere

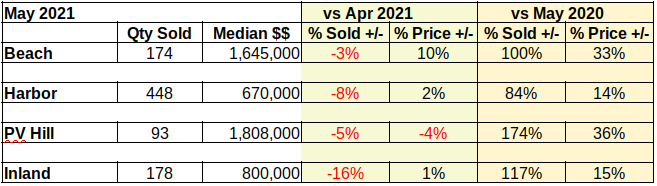

The median price in May of this year is shown in the chart below. Because 2020 wasn’t very meaningful in terms of normal real estate activity, we pulled up 2019 statistics. Respectively, the median price is up from 2019 by 25% at the Beach, 20% in the Harbor, 18% in PV and 16% Inland. That’s more than a healthy increase in prices for two years of appreciation. We can see from the charts there was some rapid inflation the first quarter of the year. More so at the Beach and in PV than elsewhere. Probably we’ll see some of that taken back as the market cools.

What we’re not talking about is what part of the market is selling? High? Low? Let’s look at the sales volume to find the hot spot in the market.

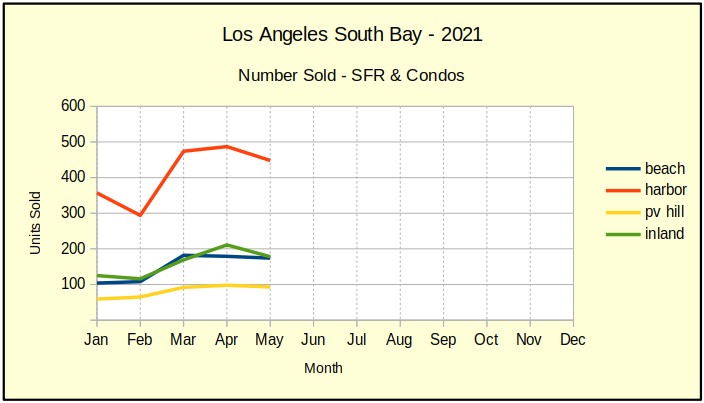

Sales Volume Starting to Smooth

The number of home sales per month across the South Bay has just about returned to normal. Sales in May 2020 were off by 45%-55% across the board from 2019. Now, comparing May of 2021 to 2019 we find that the Harbor cities have had virtually zero change in the number of sales. By contrast, the Beach shows 2% more sales, the Inland cities 5% growth in sales, and Palos Verdes 19% growth.

Two things stand out for me. The two year lack of growth in sales volume for the Harbor cities tells me the pandemic hit those cities the hardest. The recovery there will lag behind the rest of the South Bay offering some opportunity for those ready to buy now.

The second hot spot is 19% growth in sales volume on the Palos Verdes peninsula. Looking over the actual sales, I’ve concluded it’s simply that there are far fewer homes on the Hill, so minor change in sales statistics can look like a major fluctuation.

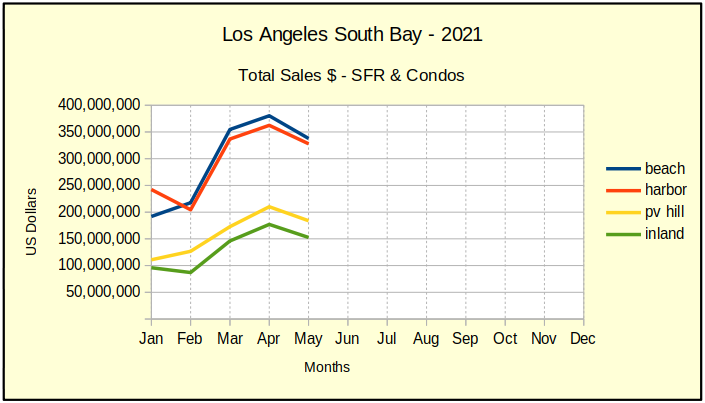

Total Sales Down Across the South Bay

Our chart below shows the total sales dollars climbing out of a winter slowdown that was accentuated by the pandemic. All areas rose uniformly in March and April of this year ending in May just about where they were the prior fall. June results will give us a better picture, but we expect a gradual leveling as inventories grow.

As of now, activity indicates that the peak of recovery from the pandemic is passing by us right now. Things should level out over the summer leaving us with a statistically somewhat normal sales year.

South Bay Summary

Across the South Bay we’re seeing a moderation of the wide swings and extreme numbers generated throughout the pandemic. For example, monthly March sales volume for all areas was up 57% over the prior month. By the end of April volume was only up by 6%. For May it was down -8%. Taking a peek at sales to date in June, it should be at -2% next month.

What we’re watching is the panic leaving the marketplace and stability returning. Pent-up demand earlier this year pushed property prices up as much as 14% on a month-to-month basis. While still steep, the high for May was 10%. Our forecast for June price increases in SoBay is a high of 9%, with a low of 0%.

At the moment there is little indication prices will move into negative territory beyond losing some of the rapid inflation of recent months. That may change as moratoriums on eviction and foreclosure dissipate. Currently slated to end September 30, 2021, some fear that the end of local moratoriums will release a flood of foreclosures and cause prices to plummet.

Locally, Los Angeles county and city have offered several alternative plans to minimize the impact. In some cases the entire debt may be covered by combined State, Federal and local government funds, completely rescuing both the tenant and the landlord from housing loss. As a result, many in the industry expect prices and activity levels to return to approximately where they were prior to the pandemic.

We believe the level of inventory will be nearly normal by this fall. Already we see offer prices declining and Average Days On Market (ADOM) stretching past 30 days for 15-20% of available homes. Following the usual slowdown for the holiday season, we predict a robust January in 2022 as the pandemic becomes a fading memory.

Judging from the downturn in May, we’re now returning to a more normal market. So, logically speaking, homes listed in June and later should come on the market at slightly lower prices. Our expectation is for area median sales to fall back by approximately $175K in the Beach and Harbor areas, with a decline of about $100K for PV and Inland area sales.

When the pandemic hit, event venue The Grand in Long Beach was no longer able to host events, most of which are weddings. Rather than panic about the loss of income, The Grand decided to get involved in the community. They contacted the City of Long Beach numerous times and eventually were able to find a deal where they could cater to Roomkey and Homekey sites, which are former hotels converted into homeless housing.

Though The Grand did charge for their meals, since they were already at a loss from the pandemic closure, that wasn’t the main purpose. Each meal was only between $5 and $6, so the primary benefit to The Grand was feeling like a part of the community. And the homeless community benefitted immensely. Not only were they provided with meals without needing to leave the safety of their homes, but this was professionally catered food from a business that does events for a living. It’s good food, and helps give the homeless community hope and feelings of self-worth.

The City of Long Beach approved the Commercial Rental Assistance Grant (CRAG) back in January, and their application period is now open. It allows small businesses to get up to $4000 in funding to help them pay rent. The funding, which is approximately $1.7 million, comes from the federal COVID relief funds. Eligible businesses must be in a designated CRAG zone within Long Beach, conform to the Health Code, and have no more than 50 full-time employees. The application period began June 11th and goes until July 22nd, and applications can be done online.

We’re all aware of racial disparities when it comes to homeownership, even if we don’t all know the extent of the disparity. What may come as a surprise is that the issue even extends to refinancing for those Black and Latinx households that do already own a home. Surely Black and Latinx households can benefit from refis just as much as white households — so why don’t they? The increasing volume of refis this year, due to lower interest rates, could shed some light on the issue.

Two of the major reasons are actually readily observable. Because Black and Latinx households are usually lower income, they also tend to have lower credit scores and higher loan-to-value ratios. Both of these pose risks to lenders, which causes lenders to quote higher interest rates. These combined probably account for about 80% of the disparity. Possible reasons for the remaining 20% include lower education, lower financial literacy, less employment stability, and weaker social networks. All of these are, in fact, underpinned by systemic inequality. While changes in the mortgage and lending industry can help to address the disparity, the long-standing effects of systemic inequality will dampen any such efforts.

With demand being so high in the housing market, house sales are happening quickly. But that’s not the only thing selling quick. Those new homeowners are also looking to purchase new appliances and electronics for their new house. Best Buy in particular has exceeded their sales expectations. They’ve particularly noted sales of big screen TVs and home consultations and installations. Home Depot and Lowes are also faring well, and Walmart has increased their investment in home goods.

Representatives from Best Buy say that it’s the consultations and installations that put them over the top. There are many companies that sell appliances or TVs or office supplies. But most don’t also offer home services along with the sales. Services such as internet tech support are in high demand for buyers just moving in, who don’t want to waste any time getting connected. However, they’re less certain about their future in the second half of the year, as pandemic restrictions are ending and people are spending less time at home.

Relativity Space, an aerospace company headquartered in Long Beach, has announced its new rocket the Terran R. The Terran R is fully 3D printed and is reusable. The 3D printing process allows for manufacture in under 60 days, with 100 times fewer parts than traditionally built rockets. Relativity was also working on a smaller rocket, the Terran 1, but decided to raise $650 million from investors to accelerate development of the Terran R.

The Terran R is intended to be a space freighter, capable of carrying cargo between Earth, the moon, and Mars. Relativity believes software-based 3D printing is the future of aerospace manufacturing and can enable efficient space travel. Their eventual goal is human colonization of Mars.

Union labor is strong in Long Beach, where the International Longshore and Warehouse Union (ILWU) has a large workforce. Despite unionization, some things are out of their control. Terminal operators currently are frequently union workers working for a public entity, since ports are usually owned by the city. But the terminals themselves are often owned by private companies, and leased to the city.

In Long Beach, the Pier T terminals are owned by Total Terminals International (TTI), which is itself jointly owned by companies based in Switzerland and South Korea. TTI is in the process of considering terminal automation to improve efficiency. While they may achieve their efficiency goal, it will also cause many of the ILWU workers to lose their jobs as terminal operators. With the terminals being internationally owned, TTI doesn’t have much incentive to care about US workers, unless their decision causes the City to want to break ties with them.

Last year, the California Public Utilities Commission (CPUC) imposed a moratorium on utility disconnects for nonpayment. The CPUC moratorium applies to both residential and commercial buildings, and they regulate the majority of electric and gas companies. However, this moratorium is slated to end July 1st, and the total amount owed is fast approaching $2 billion.

Utility companies aren’t about to simply forgive all of these charges. Fortunately, they’re thinking of plans that can help people balance their debts without owing large lump sums. Possibilities include partial forgiveness and/or rate categories, or even full forgiveness for qualifying households. California is also working on including utility aid in their state budget plan.

As a concession to restaurants during COVID-19 restrictions, they were given access to expanded outdoor dining space and the option to provide alcohol as part of takeout orders. Indoor capacity restrictions have recently been removed, but in California, these options are staying throughout the rest of the year.

City officials agree that outdoor dining has brought something to the cities that they were lacking. Even though many of these new spaces are not zoned for eating areas, San Francisco mayor London Breed says they brought new life to the city even during a pandemic. In fact, she wants them to stay permanently, not just through 2021. There’s also a bill to extend to-go alcohol indefinitely.

Data from 2021’s Quarter 1 Housing Affordability Index is now available, and while the numbers haven’t changed much from last quarter, the continuing downward trend is apparent. Affordability is equal to or slightly lower than the Q4 2020 numbers in all major categories, including overall US affordability.

Only seven counties experienced an increase in affordability: Kings, Merced, Butte, Plumas, Siskiyou, Tehama, and Humboldt. The already lowest affordability rating of Mono County took an enormous nosedive, dropping from 11 to 3. Lassen County remains the most affordable county at 62, despite being down from 67, but the top spot may be up for grabs as Kings County went up one point to 58.

Buying sight unseen has increased in popularity recently, as walkthrough technology has improved and the pandemic has forced fewer in-person interactions. But take care — improved technology means online walkthroughs don’t necessarily reflect reality. If you must buy sight unseen, it’s best to make sure you trust whoever is creating the images or videos for you.

Most everyone is aware of image editing software, even if it’s only Photoshop. A bad Photoshop job can be obvious, but professional photographers know how to use their camera’s inherent features to even better effect. These can include lighting modes, image enhancement, recoloring, and even splicing multiple images. Savvy buyers may instead look for video walkthroughs, which provide a better view how the various spaces interrelate. Don’t be fooled, though. Videos are almost as easy to edit as images.